report by BlackRock

Student of the Market: October 2023

On September 16, 2020, the U.S. Federal Reserve (Fed) left interest rates near zero and signaled that it expects to hold them there through at least 2023, adding outcome based guidance. The statement follows the new long-term policy framework announced by Chair Jay Powell in August at the Federal Reserve Bank of Kansas City’s annual Jackson Hole conference. The Fed notes that rates will remain near zero “until labor market conditions have reached levels consistent with the Committee’s assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time.” We didn’t get a precise definition of what a moderate overshoot would look like, allowing the Fed to retain some flexibility.

In our view, in a landscape of improved risk sentiment and strong demand for yield, U.S. corporates appear attractive even noting the recompression of spreads since the first quarter. While corporates have retraced a significant portion of their year to date widening, other sectors and asset classes have gone further, leaving corporates relatively well positioned.

Colossal policy responses in the second quarter reassured investors that the U.S. economy can weather the COVID-19 downturn, with a relatively quick return to risk assets pushing the S&P 500® up 20.5% for the period, its best quarter since 1998. After bottoming in March, U.S. stocks rose as much as 44% before the rally stalled a bit over the last few weeks of the quarter. We saw a few signs of hesitation for more policy among lawmakers as indicators improved, but overall both Congress and the Federal Reserve (Fed) remain prepared to do more.

An inevitable blame game between the U.S. and China has followed COVID-19, but the crisis has really just extended the “trust deficit” that has been steadily building between the two countries in recent years. Though the “Phase One” agreement between the countries remains intact, it is very fragile and China is turning to a more domestic focus. The U.S.-China relationship, however, remains pivotal for the global economy, and in our mini-forum devoted to the topic, we began with a discussion of the relationship from China’s perspective.

In our view, monetary and fiscal policy have done a tremendous job in papering over fundamental uncertainty. Read more for the news & nuggets

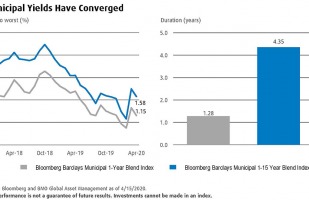

We focus on the strong recovery in the muni market over the second quarter, which proved to be illuminating to municipal investors on a couple fronts.

As the 2020 election season heats up and President Trump’s odds of winning continue to run cold, we believe it is important to understand the investment implications of a potential change in government versus the status quo. We have outlined the policy implications of the three most likely election outcomes: a Democratic sweep, a Biden presidency with a Republican Senate and a Trump presidency with a Republican Senate. This analysis assumes that Democrats hold the House, which we believe is highly likely.

In our view, the markets feel much healthier at the end of April than a month ago, but underappreciated in the improved sentiment is not only the scale of March policy action, but its continuation into April. Actions announced in April would ordinarily have remained in headlines and discussion for weeks, but the nearly half trillion dollar U.S. fiscal stimulus package has been treated almost as a footnote to its much larger cousin in March. Similarly, Fed and other central banks not only continued to implement the massive programs initiated last month, but significantly expanded on them.

Over the past several weeks, yields between short- and intermediate-term Municipal Bonds have converged. This may be an opportunity for investors to significantly reduce interest rate risk while sacrificing minimal income since shorter-term bonds typically have less sensitivity to rates.

|

While bull markets don’t last forever, neither do bear markets. Since 1928, the strength and duration of S&P 500® bull markets has meaningfully outweighed that of bear markets.

|

Pyrford International provide a snapshot of the UK economy as it inches closer to Brexit.

We believe the Fed is taking a risk — one we hope works — in shifting from reactive to preemptive monetary policy. It was not that long ago that the Fed was more forthright about the uncertainty inherent in economic forecasting as Chairman Powell used the analogy of walking into a dark room and slowing down to avoid furniture as an analogy for the Fed’s situation. Today, they seem more certain that they know the future and aim to alter it.