Investment Perspective: All About Rates

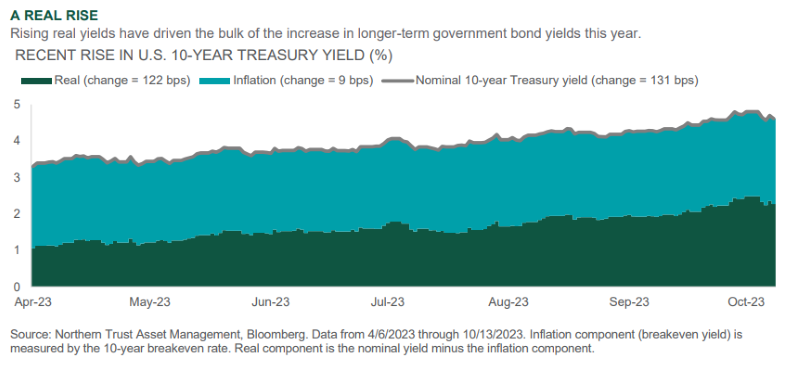

Global markets were weak over the past month, with both stocks and bonds posting negative returns. The catalyst was principally the material rise in interest rates over the course of the month – driving losses in fixed income and pressuring equity valuations. Until recently, the increase in long-term rates off of the regional banking crisis-induced lows in March had been largely driven by increased odds of a “soft landing” and the more hawkish reaction function from the Federal Reserve. The most recent increase, however, shows less fundamental support – meaning it has not been driven by changing expectations for inflation or the Fed. Instead, we believe the required term premium has increased – given economic uncertainty and interest rate volatility – perhaps exacerbated by elevated Treasury supply amid a shift toward more price-sensitive demand as the Fed continues its quantitative tightening. Given the slight divorce from fundamentals, we would anticipate some interest rate rollover in the months ahead.

We believe investors are somewhat complacent about accumulating economic headwinds. Yes, U.S. labor markets were strong and consumer spending has remained durable – but we see headwinds going forward in the capacity to spend from depleted excess savings, as credit card balances move higher and student loan payments resume. Higher rates will also impact the pace of activity in the economy. Several Fed officials have noted the tighter financial conditions from the move higher in interest rates – a clear sign they wish to telegraph to the markets that the out-the-curve rate increase has finished the Fed’s rate hiking campaign for them.

We have a new risk case this month relating to the Middle East conflict. Beyond the human tragedy unfolding, we acknowledge the risk of escalation in the region and what it could mean for oil prices. Oil supplies out of the Persian Gulf could be significantly disrupted should Iran be brought into the fight. We (and we believe central banks) will be less concerned with the inflationary impact of the resulting rise in oil prices – and more worried over the impact on growth. Demand destruction from materially higher oil prices would negatively impact global growth.

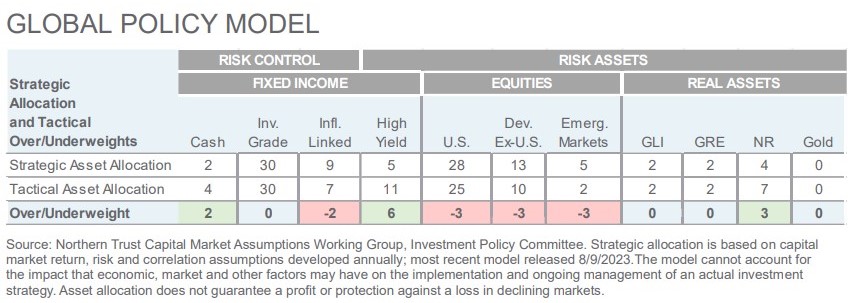

We made no changes to our Global Policy Model this month, maintaining our relatively modest underweight to risk. Equity valuations became more attractive the past month, but we continue to prefer high yield bonds to developed market equities, natural resources to emerging market equities, and maintain an overweight to cash.

- Chris Shipley, Chief Investment Strategist of North America

Interest Rates

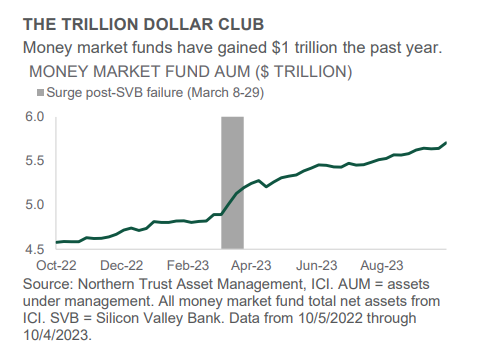

The ascent of yields on the long end of the U.S. Treasury curve has deservedly captured a lot of attention in recent weeks. Meanwhile, yields in the money markets have remained relatively stable. In addition to relative stability, nominal yields on U.S. Treasuries maturing in one year or less remain the highest on the entire yield curve – even after the recent spike in yields on the long end. As we wrote about in April, this dynamic has presented front-end investors with yield opportunities not seen for well over a decade, and Money Market Mutual Funds (MMFs) have continued to rise to the occasion.

In the weeks following the failure of Silicon Valley Bank in March (March 8-29), MMFs surged by over $300 billion to $5.2 trillion as measured by ICI – a record high at the time. Since then, MMFs have gathered even more assets, setting several new all-time highs along the way. They total a whopping $5.7 trillion as of October 4th, 2023 (see chart). The combination of yields over 5% and ability to purchase or redeem shares the same day has continued to attract investors into MMFs. Considering the recent uptick in uncertainty around geopolitical developments, we may continue to see MMF AUM drift higher yet into year end.

- An inverted yield curve and high liquidity have driven a massive increase in money market investments.

- Investor interest may remain elevated given a higher-for-longer Fed and broader financial market risks.

- We remain overweight Cash and neutral Investment Grade Fixed Income given an inverted yield curve and

Credit Markets

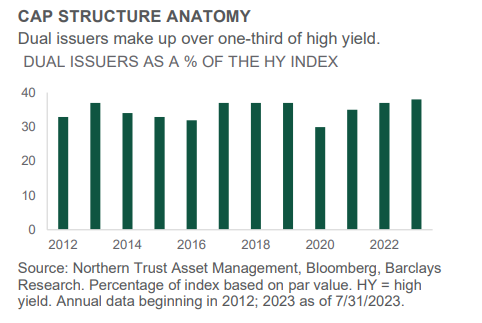

With the recent uptick in rate volatility and renewed concerns around ongoing rate hikes, issuers’ capital structures and the effects on fundamentals from a higher-for-longer rate scenario have come back into focus for investors. With rates and inflation being suppressed for more than a decade following the Global Financial Crisis, companies took advantage of the cheap funding cost by issuing floating rate debt. However, high yield issuers with exposure to rising interest costs via loans are especially exposed with rates on the rise – leaving dual issuers (issuers with both bonds and loans outstanding) worse off from a coverage standpoint.

The interest coverage ratio for dual issuers is 4x compared to 5.2x for bond-only issuers. Dual issuers make up slightly more than a third of the par amount outstanding in the high yield universe, as seen in the nearby chart. High yield issuers with loans in the capital structure tend to be larger companies, which, if worsened fundamentally could put pressure on the broader high yield index. With active management, opportunities may exist in investing in businesses with diversified revenue streams with bond-only capital structures given the current interest rate environment.

- High yield issuers with both bonds and loans outstanding (“dual issuers”) are over 1/3 of the index.

- These issuers – with worse coverage ratios in aggregate – may come under relatively higher pressure from rising interest rates versus bond-only issuers.

- We maintain a bias for default (credit) over market (equity) risk in the Global Policy Model while seeking credit selection opportunities from higher interest rates.

Equities

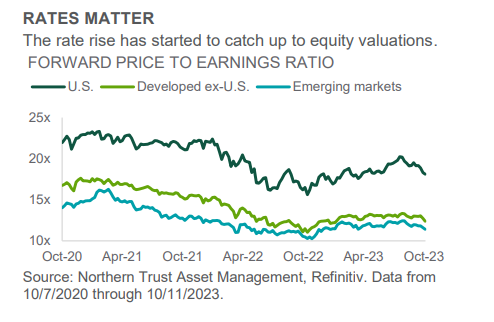

The equity market decline that started two months ago picked up speed this month, with global equities falling by 3%. A rapid rise in long-dated real yields in the U.S. and Europe and the tighter financial conditions they portend added to investor concern that the growth outlook is deteriorating, especially in Europe and China. Some of the complacency we have been writing about was priced out given higher real yields can put downward pressure on economic activity. The differences between regional equity performance were fairly small. The U.S. continued to modestly outperform Europe, Japan and emerging markets, driven by continued outperformance of growth relative to value. An important caveat, however, is that almost all of that outperformance has been driven by just two companies: Amazon (AMZN) and Tesla (TSLA).

Looking forward, the decline in equity markets has not been sufficient to remove our concern regarding market complacency. We continue to worry that the U.S. economy will struggle to pull off a soft landing and see further weakness in Europe and China. As a result, we remain positioned for incremental disappointment on both the economic and earnings front, with underweights to all three major equity regions (3% each).

- Equities declined on the back of a rapid rise in long-dated real yields – with valuations leading the losses.

- The valuation reprieve better aligns with our outlook, but it may not yet have fully run its course.

- We remain underweight developed and emerging market equities given our belief that markets are pricing in too optimistic of an economic outcome.

Real Assets

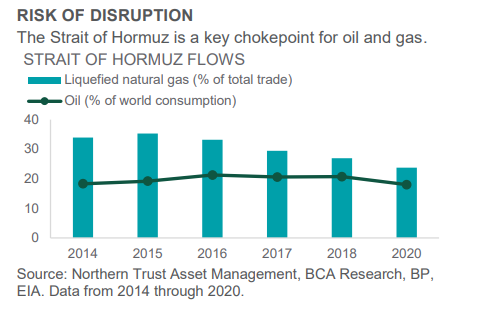

The horrific terrorist attacks on Israel are a violent reminder of the heightened geopolitical tensions that exist today. Oil prices spiked higher in response – not because of any resulting change in supply/demand dynamics, but because of what could happen should the war in Israel broaden. Specifically – should Iran become involved – it is possible that the Iranian regime would block the free flow of oil tankers through the Strait of Hormuz. Such a development could remove nearly 20% of the world’s oil supply from global markets – as well as around 25% of liquified natural gas (see nearby chart).

To be clear, this is very much a risk case – not a base case – at this point. But it’s a risk case that could have big ramifications with oil supplies tight (thanks to reduced investment over the past few years) and reserves low (notably the U.S. Strategic Petroleum Reserve, which currently sits at only 350 million barrels – as compared to the 650 million barrels held prior to recent drawdowns). We came into this already tactically overweight natural resources, given favorable fundamentals (the lack of investment leading to tight supplies mentioned above) and attractive valuations. The increased geopolitical risk only further supports our overweight positioning.

- Oil prices spiked in response to the Israel-Hamas conflict given risk that the war broadens to other areas.

- While not our base case, there is risk of a major supply shock that drives up commodity prices and weighs on the global economic growth outlook.

- The newly-introduced geopolitical conflict adds to support for our tactical natural resources overweight.

Subscribe to Investment Perspective.

Unless noted otherwise, data in this piece is Sourced from Bloomberg as of October 2023.

For Asia-Pacific (APAC) and Europe, Middle East and Africa (EMEA) markets, this information is directed to institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors.

© 2023 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A. The information contained herein is intended for use with current or prospective clients of Northern Trust Investments, Inc (NTI) or its affiliates. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. Northern Trust Asset Management’s (NTAM) and its affiliates may have positions in and may effect transactions in the markets, contracts and related investments different than described in this information. This information is obtained from sources believed to be reliable, its accuracy and completeness are not guaranteed, and is subject to change. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor. Forward-looking statements and assumptions are NTAM’s current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information

This report is provided for informational purposes only and is not intended to be, and should not be construed as, an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Recipients should not rely upon this information as a substitute for obtaining specific legal or tax advice from their own professional legal or tax advisors. References to specific securities and their issuers are for illustrative purposes only and are not intended and should not be interpreted as recommendations to purchase or sell such securities. Indices and trademarks are the property of their respective owners. Information is subject to change based on market or other conditions.

All securities investing and trading activities risk the loss of capital. Each portfolio is subject to substantial risks including market risks, strategy risks, advisor risk, and risks with respect to its investment in other structures. There can be no assurance that any portfolio investment objectives will be achieved, or that any investment will achieve profits or avoid incurring substantial losses. No investment strategy or risk management technique can guarantee returns or eliminate risk in any market environment. Risk controls and models do not promise any level of performance or guarantee against loss of principal. Any discussion of risk management is intended to describe NTAM’s efforts to monitor and manage risk but does not imply low risk.

Past performance is not a guarantee of future results. Performance returns and the principal value of an investment will fluctuate. Performance returns contained herein are subject to revision by NTAM. Comparative indices shown are provided as an indication of the performance of a particular segment of the capital markets and/or alternative strategies in general. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index. Net performance returns are reduced by investment management fees and other expenses relating to the management of the account. Gross performance returns contained herein include reinvestment of dividends and other earnings, transaction costs, and all fees and expenses other than investment management fees, unless indicated otherwise. For additional information on fees, please refer to Part 2a of the Form ADV or consult an NTI representative.

Forward-looking statements and assumptions are NTAM’s current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information.

Northern Trust Asset Management is composed of Northern Trust Investments, Inc. Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K, NT Global Advisors, Inc., 50 South Capital Advisors, LLC, Northern Trust Asset Management Australia Pty Ltd, and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company. P-091923-3121146-091824

Weekly Investment Commentary: Munis offer yield relief from inflation’s heat

U.S. yields began the year at their highest starting level since 2011, and they have since risen further across the Treasury and municipal curves.

Global Weekly Commentary: Higher bar for U.S. earnings to deliver

We saw 2024 as a year of two stories. First, cooling inflation and solid corporate earnings would support upbeat risk appetite.

Global Markets Weekly Update: April 19, 2024

Review the performance of global stock and bond markets over the past week, along with relevant insights from T. Rowe Price economists and investment professionals.