Successful charitable giving plans start with “why”

December 30, 2022, fell on a Friday. Many of you may have been relaxing at home during the holiday break, but I was scurrying around my house gathering up items to donate. Not only was I doing this to clear out some space in my closet, but also to make sure I would be able to get a receipt for a charitable donation for the 2022 tax year.

As I drove up to the donation center, I found a long line of cars. It seemed a lot of other people had left their charitable donations until the final days of the year. As I waited my turn, I told myself, “Next year, I’m going to plan this better and not leave it until the last minute.”

If you’d like to stay up to date on these ideas and timely solutions, sign up for our Wealth Management email subscription.

There’s a good chance many of your clients are considering making a charitable donation sometime during the next few months. Research shows that most Americans donate to nonprofit organizations and feel that others should be doing so as well:

- 69% of the U.S. population engages in charitable giving

- Each person supports an average of 4.5 charities

- 77% believe everyone can make a difference by supporting charitable causes1

While Americans are committed to giving, many of those who make donations (me included) wait until the last possible second of the tax year to do it: 30% of annual giving occurs in December, and 10% of annual giving is done in the last three days of the year.

Successful giving depends entirely on the goal(s) an investor is trying to achieve, and financial professionals can be instrumental in helping clients clarify and achieve those goals. Being able to provide the appropriate guidance can help clients achieve their financial, charitable, and value-based goals, as well as further integrate you into a family’s wealth transfer plans.

Why do people give?

To offer useful guidance, it’s important to first understand why people give. There are actually several proven reasons, but for our purposes I think the two most important are 1) tax purposes and 2) the good feelings giving helps create.

Regarding reason number one – taxes – there a few things to keep in mind:

First, remember that charitable contributions to an IRS-qualified 501(c)(3) public charity can only reduce your tax bill if you choose to itemize your taxes.

Second, if your deductions are over $13,850 (single) or $27,700 (married filing jointly), it’s important to understand how different assets are viewed by the IRS. If you donate cash, you can generally deduct up to 60% of your adjusted gross income. However, if appreciated assets (held for one year or longer) are donated, they are deducted at fair market value, up to 30% of your adjusted gross income.

Lastly, it’s always a good idea to make sure you are donating to an IRS-qualified organization and to keep a record of all contributions.

Understanding the “why”

While these tax-related details are relatively black and white, the motivations behind the contributions and the feelings they might elicit for a client are far more complex. Investors have myriad choices when making charitable gifts. Social, wealth transfer, and personal goals, as well as the aforementioned tax deductibility, all factor into an investor’s final selection. Family patriarchs or matriarchs may also want the next generation to understand how important charity is to them and make sure this value lives on into the future. That’s why clarifying a client’s true motivations is an essential step in supporting their charitable giving goals.

Helping clients understand the “why” behind their giving is where an advisor can truly add value. Plus, the reasons will inform many of the tax aspects of these donations, such as what form they should take, when they are made, and how the overall donation should be conducted. For additional guidance, we’ve developed a charitable giving resource to help clients think through these considerations and make informed decisions.

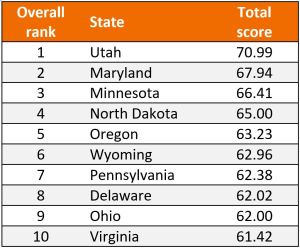

Whatever the reasons behind clients’ giving, it’s a good idea to start the charitable planning process now. Advisors with clients who live in certain areas should have charitable giving on their radar (see below for the top-10 most charitable states based on factors such as share of income donated and volunteer rates).

Top 10 states for charitable giving

Source: “Most Charitable States for 2023.” Wallethub, November 2022. States were compared across 19 key indicators of charitable behavior, with data set ranging from the volunteer rate to share of income donated to the share of sheltered homeless.

Another consideration to keep in mind is that clients of certain faiths may be more inclined to prioritize giving. Mormons donate more than any other Christian group, while Jewish individuals outdo all other religious givers.2

Whether it’s taxes, values, or some combination of the two, charitable giving is something a lot of our clients will be focusing on soon. And while a lot of giving occurs in December, it doesn’t necessarily have to. With a bit of planning and discussion, advisors can help the families they work with meet their timely financial goals along with their timeless charitable aims.

Sources

1 “The Ultimate List of Charitable Giving Statistics For 2023.” Nonprofitsource.com, 2023.

2 “Charitable Giving Statistics for 2023.” Define Financial, February 10, 2023.

IMPORTANT INFORMATION

The information contained herein is for educational purposes only and should not be construed as financial, legal or tax advice. Circumstances may change over time so it may be appropriate to evaluate strategy with the assistance of a financial professional. Federal and state laws and regulations are complex and subject to change. Laws of a particular state or laws that may be applicable to a particular situation may have an impact on the applicability, accuracy, or completeness of the information provided. Janus Henderson does not have information related to and does not review or verify particular financial or tax situations, and is not liable for use of, or any position taken in reliance on, such information.

Tax information contained herein is not intended or written to be used, and it cannot be used by taxpayers for the purposes of avoiding penalties that may be imposed on taxpayers. Such tax information and any estate planning information is general in nature, is provided for informational and educational purposes only, and should not be construed as legal or tax advice.

The opinions and views expressed are as of the date published and are subject to change. They are for information purposes only and should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector. No forecasts can be guaranteed. Opinions and examples are meant as an illustration of broader themes, are not an indication of trading intent and may not reflect the views of others in the organization. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio. Janus Henderson Group plc through its subsidiaries may manage investment products with a financial interest in securities mentioned herein and any comments should not be construed as a reflection on the past or future profitability. There is no guarantee that the information supplied is accurate, complete, or timely, nor are there any warranties with regards to the results obtained from its use. Past performance is no guarantee of future results. Investing involves risk, including the possible loss of principal and fluctuation of value.

Janus Henderson Group plc ©

C-0924-51481 09-30-24 TL

Regrets, I’ve had a few: 7 common financial regrets (and how to avoid them)

Retirement Director Ben Rizzuto explains how we can learn from the regrets of others to better prepare for the future and shares seven steps to help ensure we don’t lament our past financial decisions.

Helping Clients Act on 2023’s Opportunities – At Any Age

While the principles of good investing haven’t changed, clients’ perceptions and their outlook for 2023 likely have. We believe in preparation, not prediction, when helping investors navigate the wide range of possible outcomes ahead. In the 2023 market outlook from Morningstar Investment Management, you’ll gain perspective on the current financial environment and positive steps to help address financial planning opportunities.

Women and savings: Your future in focus

We’re talking about women’s finances, including how to identify your goals and decide what you may need to save for the future.