Helping Clients Act on 2023’s Opportunities – At Any Age

Key takeaways

- Welcome to our 2023 outlook, where we take a positive yet realistic view of the investment landscape.

- This year, we cover our “2 x 2 Investing Grid” again, but also add our ideas for people in their 20s, 30s, 40, 50s, 60s and 70s.

Navigating the Big Four—Inflation, Valuations, Recession, and Retirement

Welcome to our 2023 Outlook!

The outlook has been created to highlight the most important issues facing investors, share insights from our current research, and help you make better investment decisions as we enter 2023. It has been compiled by our investment leaders, draws on the work of our global team, and is informed by our investment principles.

As we look back over the year that has passed, it is striking how much the economic, geopolitical and investing environment has changed over the last 12 months. A war in Europe, a cost-of-living crisis and the collapse in the price of (formally admired) technology companies have all grabbed the headlines and reinforce a comment we made this time last year: “The future holds a wide range of possible outcomes and is characterized by unyielding complexity that continually defeats those who seek to make confident forecasts. Fortunately, our role as investors is not to forecast the future, but rather to construct portfolios that empower people to reach their goals whatever the economic and market conditions.”

We Welcome 2023 with Open Arms

As we look forward this year, we hold to this mantra but would highlight that the fall in the price of equities and bonds this year has improved the outlook for investors. Underlying this view is the understanding that returns to investors will be determined by both the cashflows generated by the assets in which we invest and the price we pay to acquire those assets. Last year, we noted fundamentally attractive assets that were unattractive investments due to their high price. This year, we see some fundamental weakness in certain assets, but they can be bought at sufficiently lower prices to create a more fruitful ground for investors.

The importance of this dual focus when undertaking investment analysis tends to be lost in markets characterized by excessive optimism or pessimism. As investors become increasingly focused on the near-term path of prices—confident of either a continuation of the past or a sharp reversal—many forget that most paths lie between these two outcomes. It is for this reason that we adopt a granular, fundamental and valuation-driven approach to investing, acknowledging that expensive markets can provide opportunities, and cheap markets may be a source of threats. In every situation, the right approach is to view the future probabilistically and think long term.

Working with the Conditions We’re Presented

At the start of 2023, it is even more important than usual to look beyond the headlines that confront us and focus on the objectives of investors and the risks to meeting those objectives. We have sought to address these in the following pages, offering practical insights drawn from our own research that are aligned to the key objectives of investors and expressed in the portfolios we manage.

Investing Ideas at Every Stage of Your Journey

We are aware that in such a volatile environment, each generation has particular concerns. Therefore, we have included a series of key ideas to support investors at each stage of the investing journey.

The Biggest Questions for People in their 20s (Click Here to See Our Ideas)

- Is now a good time to get started with investing, given all the noise and uncertainty?

- Should I be building my assets in stocks, property, high-risk assets like crypto, or my own education?

- How much should I invest for it to be worth it?

The Biggest Questions for People in their 30s (Click Here)

- Should I repay debt, save cash, or invest? What will help me most if interest rate rise?

- Is investing for retirement worth it? Should I avoid locking my savings away in case I need it?

- Should I align my savings with my values, or keep separate?

The Biggest Questions for People in their 40s (Click Here)

- How much do I need to invest from here through to retirement?

- What is the right asset mix for my phase of life?

- What should I do to protect against loss, such as losing my job in a recession?

The Biggest Questions for People in their 50s (Click Here)

- Given the market moves, will I have enough capital to reach my goals? Are my goals realistic?

- How do I make the most of my savings? What are my smartest investment options?

- What impact would a market crash have before retirement?

The Biggest Questions for People in their 60s (Click Here)

- How do I know if I have enough money to retire?

- What’s the smartest approach to generate an income from my portfolio?

- How do I deal with inflation, given rising expenses and falling asset prices?

The Biggest Questions for People in their 70s (Click Here)

- Should I adjust my spending in this environment? Is my capital going to last?

- Can I do anything to safely generate more income from my portfolio?

- How do I avoid the big mistakes that will cause me to run out of money?

As you can likely see, the above captures the “big four” of 1) inflation, 2) interest rates, 3) recession, and 4) retirement needs. These topics are covered herein, but if you’d like to see a more detailed list of ideas for each age bracket as we enter 2023, we have one-pagers available at the above links too.

We wish you a prosperous 2023 and happy investing.

Getting Ahead of Inflation Changes in 2023

Marta Norton, Chief Investment Officer, Americas

2022 caught investors off guard with persistently high inflation and aggressive responses from central banks worldwide. Could 2023 be more of the same? Potentially. Though there are also reasonable arguments to be made for a disinflationary environment, or worse, a stagflationary environment. With the full spectrum of possibilities in mind, we ought to position portfolios to weather a range of inflationary environments in 2023. 2023s Inflationary Environment Isn’t Preordained

The relentless worldwide persistence of inflation surprised investors—and economists—in 2022. Heading into 2023, inflation remains a challenge for much of the developed world, from the U.K., to Europe, to the United States. This is no small concern. Beyond the pressure inflation applies to consumers wallets, it’s also a destructive force on investments. That is, inflation demands a higher return hurdle to meet investor goals while simultaneously making returns harder to come by, reducing the value of bond income payments and eating away at company earnings. The Bank of England, the European Central Bank, and the Federal Reserve have each taken varying levels of aggression against inflation, aiming to cool demand and reinforce price stability in their respective economies. The central bank response to inflation has had an equally, or perhaps even more costly, impact on asset prices as inflation itself. With interest rates moving higher, bonds have been particularly hard hit—U.S. Treasuries have suffered double digit declines this year, which is among the largest in history. The respective paths ahead for inflation and interest rates are arguably two of the most critical variables for 2023 market outcomes. Should inflation surprise to the upside, central banks may very well continue to push rates higher, economies could teeter further into recessions, and asset prices could continue to decline. But higher inflation isn’t the only risk in 2023. If inflation is not as quick to dissipate as consensus thinks, central banks may maintain a tightening posture for longer. Stubborn inflation and higher interest rates could mean the easy above average equity and bond returns of the past decade are a thing of the past, at least for now.

Understanding the Range of Outcomes is Paramount

Of course, no outcome is preordained. In the U.S., inflation hawks can point to any number of persuasive arguments for a bleak inflation outlook, but the market itself is pricing in moderate levels of U.S. inflation over the next five years, with falling rates from the Federal Reserve by the end of 2023. Under those conditions, it’s not a stretch to imagine U.S. markets bouncing back in short order, rewarding investors who have stayed invested.

Easing inflation and rates in the U.S. bodes well for emerging markets too, particularly those with debt denominated in U.S. dollars. However, inflation rates in the U.K. and Europe are less contingent on U.S. outcomes. Nuanced issues exist in these markets, with the debt challenges in the U.K., the continuing European energy crisis, and uncertain geopolitical outcomes. Given this dynamic, it’s hard to imagine a quick resolution to inflationary concerns in those markets.

Yet even in the U.K. and Europe, five-year inflation expectations are only slightly above long-term inflation targets—and well below current levels—underscoring that over the long run, the momentum for inflation is generally to the downside.

Our View of Inflation Pathways

Our own inflation outlook leans benign. As long-term investors with valuation models focused on the coming 10 years, not the coming 10 months, our inflation and interest-rate expectations are not Herculean.

But building portfolios for a range of time horizons and investment goals requires outlooks that don’t just focus on the next 10 years, but also the journey markets take to get there. With that in mind, we recognize that in today’s uncertain climate, the range of outcomes in the near term is particularly wide. Moreover, the market, while typically quite good at pricing in possibilities, has been consistently off the mark on inflation—and interest rates—over the past year.

It’s important that we size asset classes for portfolios not just based on their valuation, but also their behavior in a range of inflation and economic growth environments. For example, due to markedly higher valuations, we’ve reduced our energy exposure over the course of 2022. However, we have retained exposure to master limited partnerships (MLPs) and European energy, both of which are relatively cheaper in our eyes than broad US energy and may prove resilient should inflation remain persistent. We’ve also maintained exposure to U.S. Treasury Inflation-Protected Securities (TIPS), which have sold off over the course of the past year as real rates have risen. These now appeal to us, not just due to their better valuations but also because they offer portfolios a measure or protection against negative inflation surprises. In fact, our analysis suggests both energy and U.S. TIPS could prove effective even in a stagflationary environment, when growth disappoints but high levels of inflation persist.

While we’ve considered portfolio outcomes in the event inflation and interest rates remain high, we’re also cognizant of how portfolios could behave if we enter a disinflationary environment, which is characterized by positive but slowing rates of inflation. Under those conditions, our analysis of history suggests higher-duration fixed income could outperform. An increased level of fixed income exposure may therefore do well in that environment. Within equities, our analysis suggests that defensive sectors are also attractive in the event of disinflation.

In sum, it’s not an inflation forecast or rate expectation that dictates positioning. In fact, we think forecasts of that variety are largely a fruitless exercise, especially when they matter most. Investors and economists have learned that the hard way over the past year. Far more critical to our mind is acknowledging the full spectrum of possibilities and positioning portfolios to weather the range of them. From deflation to inflation to stagflation and beyond, we enter 2023 considering portfolios in light of each outcome, weighing market expectations against the price. It’s this emphasis on planning over prediction that we believe will allow for good client outcomes over the long run.

Are We in a Low Return World? We Doubt It

Philip Straehl, Global Head of Research, Investment Management

Much of the post global financial crisis period was marked by loose monetary policy and low inflation, which provided fertile ground for financial markets. This trend was only turbo-charged by the global pandemic, which took the shackles off any policy restraint and saw developed nations, spearheaded by the United States, launch unprecedented fiscal stimulus programs to support economic activity during the COVID lockdowns. These policy measures reinvigorated animal spirits, fueling a post-pandemic speculative frenzy in everything from meme stocks to cryptocurrencies, pushing asset prices to new highs.

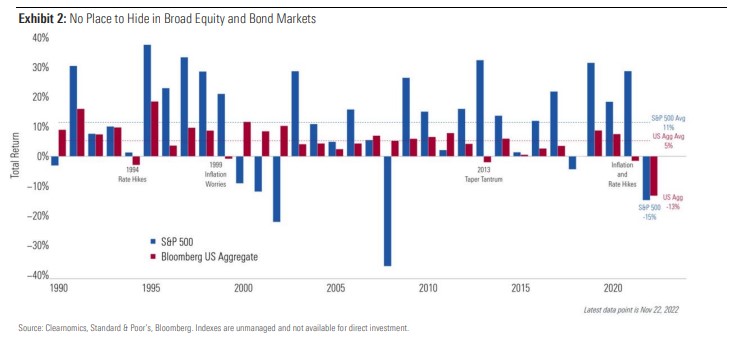

Inflation reaching four-decade highs in 2022 was the proverbial wet blanket that caused these trends to go into reverse. With price stability on the line, central banks could no longer provide a backstop to asset prices which markets had gotten accustomed to since the dotcom era “Greenspan Put.” Instead, central banks were “taking forceful and rapid steps” to bring inflation down, push bond prices up and deflate risk assets. The most rapid increase in interest rates on record, propelled in a double-digit selloff in both stocks and bonds, leaving investors with only a few places to hide as markets adjusted to the new environment.

The double-digit sell-off in investors’ 60/40 portfolio which provided diversification during many previous downturns, left investors wondering whether low returns are in store for the foreseeable future. We doubt it. Taking a longer-term perspective, the 2022 downturn has set the stage for a much-improved long-term investing environment.

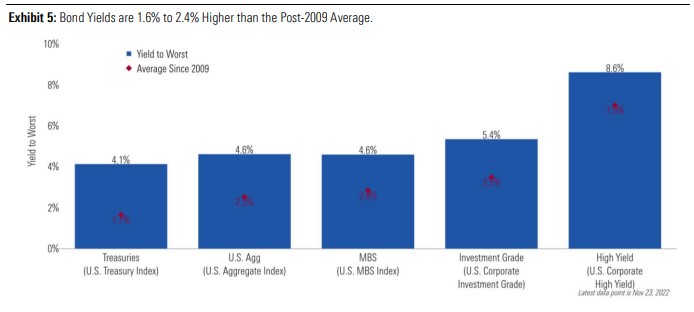

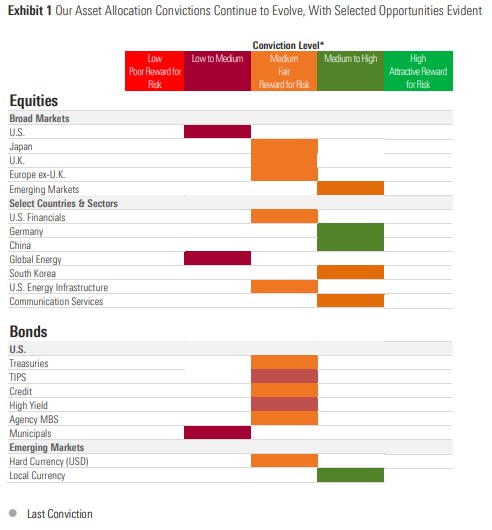

One reason for optimism comes from fixed income. The 10-year U.S. real yields are at their highest level since 20092, offering meaningfully positive return prospects after inflation—following an extended period of not keeping up with consumer prices. As a result, we assign a medium conviction to core U.S. fixed-income markets (including Treasuries, corporates, and TIPS), indicating a more balanced reward-for-risk picture within bonds today. And major investment-grade bond markets priced to deliver a return after inflation between 1.5% to 2% over the next decade.

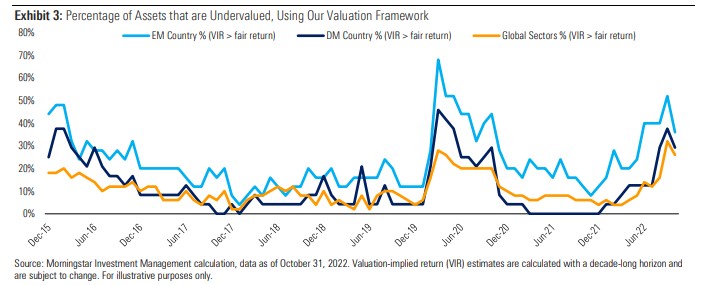

Equity market valuations are significantly better now than late-2021, too. This improvement has been reflected in the percentage of assets trading at a positive spread-to-fair value. For example, 12 months ago, there were no developed country equity markets that were undervalued using our valuation models. In contrast, at the end of October 2022, almost 30% of countries were cheap compared to their longterm fair-value expectations (i.e., undervalued). Notably, this proportion was even higher at the end of September 2022, with 37.5% of countries in coverage presenting as being undervalued.

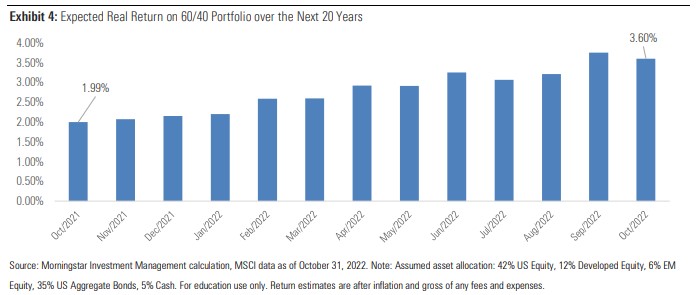

Considering the improvements in equity and fixed income valuations over the course of 2022, our valuation models suggest that the 60/40 portfolio stands to deliver a return after inflation of 3.6% over the next two decades. This is a 1.6% improvement from a year ago.

Rotation within equity markets was another key theme over the course of 2022. In others words, those assets displaying the best prospects a year ago are not displaying the best prospects today. This rotation has seen some assets fall away in their appeal and others rise over the past 12 months. For example, energy companies stood out through 2020 and much of 2021 as one of the most attractive assets. While energy has declined in the rankings since this time, the prospective ranking for communication services companies has gone the other way. Twelve months ago, the communication services sector was ranked sixth out of the 10 world sectors. Today, it sits at the top.

Communication services is a truly diverse sector, encompassing internet media companies (such as Alphabet and Meta), media and entertainment companies, and telecom services providers. In part a function of weak recent share price returns—experienced by a number of its most significant constituents—global communication services now possess one of the highest valuation-implied return estimates among the sectors we cover. While we do see heightened fundamental risk present in the sector as opposed to other asset classes, valuations (both absolute and relative) as well as contrarian elements tip the scales on our conviction in favor of a “Medium to High” overall score.

We also see significant opportunity within emerging-markets equity. This asset class, which encompasses a wide swath of countries in the “developing” world, has experienced broadly negative share returns in 2022—especially in U.S. dollar terms. Given our assessment of valuation, the fundamental risk picture, and contrarian elements, we conclude that absolute and relative valuations have improved to the degree that it merits an upgrade in our overall conviction to “Medium to High”.

These are just two ideas, among a better opportunity set. Yet, our valuation model suggests that both communication services and emerging markets stocks are expected to deliver a real return (above inflation) of around 7% over the next decade.

Better Valuations Create Opportunity, But the Principles of Good Investing Still Apply

The above analysis is encouraging, especially after a challenging year. That said, we acknowledge periods of market volatility can be unnerving for clients. These are the times when special attention should be given to managing our behavioral biases as investors. Our approach is to follow a disciplined valuation-driven investment process guided by a set of investment principles that keep us focused on the long term and what matters fundamentally. Periods of uncertainty often lead to the biggest opportunities in the market, as market participants overreact to news.

Yet, the principles of good investing must still apply. As such, we put forward five key lessons that will hold us (by us, we mean collectively) in good stead through 2023 and beyond: 1) to be long-term minded, 2) to use a consistent framework for assessing value, 3) to deeply assess fundamentals, 4) to think contrarian, and 5) to understand where you are in the capital cycle. As we navigate markets today, we remind ourselves of these lessons and remain optimistic that the best days for investors lie ahead.

Helping Clients Navigate a Recession

Mike Coop, Chief Investment Officer, Europe, Middle-East & Africa

As investors, the reality is that a recession appears the most likely scenario for many countries. The “R” word tends to incite fear, but every investor will endure multiple recessions in their lifetime. The key is how we deal with them, as they have a habit of bringing out the worst in investors—every single time.

Given the long-term nature of investing, enduring the odd recession is a pre-requisite to attaining your full list of financial goals. It is not just about financial discipline, but also having strong foundations that allow you to withstand inevitable setbacks and even thrive when they occur. More often than not, this carries three requirements, 1) goal-setting as a true north, 2) staying the course with a well-diversified portfolio, and 3) using valuation to get the odds in your favor.

This framework helps give the necessary perspective to address today’s concerns, with common examples including:

- Whether bonds will work as a diversifier this time.

- If history is irrelevant because the world is changing.

- Staying invested if a recession is coming.

This Economy is Different, But It Always Is

Yes, high inflation and changing geopolitical conflict does mean today’s economy is different from the past. However, we should not forget the long history of business cycles across all kinds of economic and geopolitical environments. Where does that leave us today? Will a global recession happen in the next 12–14 months? According to Preston Caldwell, Morningstar’s head of U.S. economic research, it’s a virtual coin toss—at least in the U.S., which accounts for around a quarter of the global GDP and over 60% of the global stock market.

"Either way, we expect growth to accelerate again in 2024 as the Federal Reserve lifts off the brakes" Caldwell said. Underpinning this view, resolving supply chain issues has begun to lower the price of goods and should continue to tamp down inflation. Caldwell forecasts that inflation has a reasonable probability of receding to normal levels in 2023 and could even undershoot the Fed’s 2% inflation target by 2024. Of course, this is just one possible pathway, but the analysis is encouraging and plays true to our philosophy—to position portfolios for multiple outcomes, not one deterministic prediction.

What’s the Real Issue Here?

It might not feel like it to clients who feel crunched by interest rates and inflation, but asking if there will be a recession—and how to avoid it—misses the point.

The true questions people are asking are “Am I okay?” and potentially “Can I do something smart at this time?”

These questions are always well intended, but they can be dangerous behaviorally. During such times, it is always healthy to center back on the truths of investing during a recession.

Truths of Investing in a Recession

- To get investment returns you need you to take risk—cash is unlikely to help you beat inflation and grow wealth over time.

- Recessions are common (occurring every 7—10 years on average), temporary (lasting several years), and eventually followed by economic recovery.

- Stocks tend to front-run the economy, not the other way around. They will also front-run the economy before the recovery happens. This makes market speculation incredibly difficult as you need to get two decisions right (exit point and re-entry point) amid heightened uncertainty. Very few, if any, have this skill.

- Stocks do have a track record of falling before and during recessions because company profits fall and bankruptcies rise. However, they have always recovered lost ground in the years that follow.

- Bonds have a track record of doing well because inflation and interest rates tend to drop. Today, interest rates and bond yields are high enough for bonds to provide this offset.

- The main way you fall short of your financial goals is a permanent loss of capital where you never recoup the losses. These can occur in recessions (such as a low-quality investment that goes bankrupt), so care needs to be taken.

- Three killers that trigger permanent losses are: 1) speculative investments with no basis for their valuation, 2) assets with too much debt, and 3) selling out at the bottom because of behavioral biases.

- Buying shares when they are cheap tends to lead to higher-than-usual returns because markets price in bad scenarios and there is upside if conditions improve.

Reaffirm Goals of Investing

Coming into 2023, it is important to make sure your goals and objectives remain relevant. Given the changes we’ve experienced in recent years, it is not unusual for these goals to have shifted. This includes confirming the timeframe for reaching them. Whatever the outcome of this review, there are big advantages of measuring success in terms of progress to reaching your goals, rather than “beating the market.”

This nudges behavior toward topping up our savings after big market falls as a way to get us back on track to reaching our goals after a market sell off rather than selling out at the bottom. By doing this, we also have the prospect of buying undervalued assets that can offer potential upside.

Staying the Course with Robust Portfolios and Using Valuation to Your Advantage

A recession is only one scenario. This vividness bias can lure you into a certain mindset, where you become fixated on recession impacts and forget the full range of potential outcomes. Proper preparation must include positive scenarios, too.

Instead of erring on the side of caution every time there is a period of uncertainty, check that you are taking the right amount of risk to reach your goals—one that you can live with in bad times and one that will be enough to at least keep pace with inflation. To do this, it often makes sense to invest in a diversified portfolio with assets including those that behave differently to others when there is recession—such as equities and high-quality bonds.

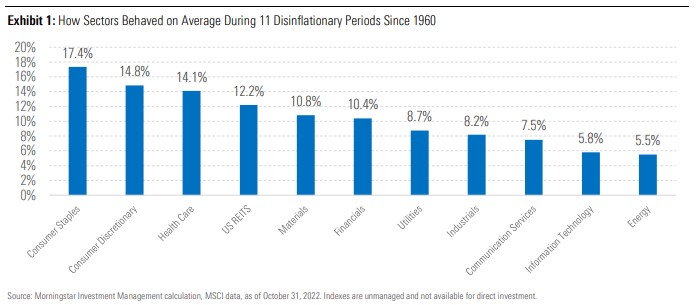

A portfolio doesn’t need to be complex—it just needs the right exposures to deliver against your goals. As part of this, it is desirable to favor assets that already reflect pessimism about the future. These assets are less prone to falling than assets that are highly popular, have gone up a lot, and are priced for the best possible scenario—and therefore, not very likely to occur. Within equities, we find it imperative to balance exposure between the most attractively valued assets along with stabilizers such as dominant companies with little debt and goods and services that are perennially in demand. Examples can often be found in areas like healthcare, utilities, and consumer staples.

Finally, unless you need to realign against your goals, you should stick to your strategy. Even in recessionary conditions, you should avoid market timing and macro forecasting—trust the experts who tell you this is a fool’s errand. Ensuring you’re not blown off course should be among your highest priorities, resisting the devil’s temptation to sell in the depths of a recession and miss out on the recovery.

Investing Positively in Retirement in 2023

Matt Wacher, Chief Investment Officer, Asia Pacific

Retirement remains a complex word, meaning different things to different people. But almost unanimously, it means “the act of stopping work.” By extension, this usually means “relying on your own savings,” potentially supplemented with government support.

For those relying on your own money, 2022 was an incredibly tough one. It contained the double-hitter of 1) inflation driving your cost-of living higher, and 2) higher interest rates causing asset prices to fall. The good news is that this shift has created a far more positive footing moving into 2023—all else being equal.

We Can All Embrace Higher Yields

As with the very best sporting teams, every asset in a portfolio plays a role – some assets are more proficient at defence and others press forward to attack—but they need to work together. It is also this cohesion that makes great portfolios. Throughout 2020 and 2021, the defensive portion of a portfolio was not well placed to do its role. Historically, low yields meant that bonds could provide little resistance to broader economic stress. That has clearly changed—and it has big implications for retirees. Not only have the long-term prospects improved for equity markets, now the defensive portion of portfolios has a genuine prospect of providing some ballast.

Investors of all types can appreciate higher yields, but this is especially relevant to retirees. It reduces the “capital gains hurdle” you need to jump, allowing you to lean more heavily on the income component of your total return. This is most pronounced in bonds, which retirees tend to have a higher allocation toward, where we can now deliver income in excess of the so-called 4% safe withdrawal rate (which remains a good rule of thumb, despite its weaknesses).

Keeping a Close Eye on Sequencing Risk

Despite the good news on yields, one must think carefully about further downside risks, too—especially with sequencing risk staring at every retiree. Conceptually, this is the danger of a near-term decline in your assets causing you to over-withdraw (the risk of a big decline early in your retirement wiping out a big part of your nest egg). This risk is ever-present, but it may feel prominent in an environment that could be recessionary. By the same token, there is a key conundrum between sequencing risk and longevity risk. That is, we don’t really know how long we need our capital to last for, so retirees do need to maintain some level of growth assets to ensure their savings can last.

Fortunately for investors, higher yields impact both the equity and fixed income assets in the portfolio—and how they work together. Notably, improved defensive characteristics from bonds can provide more scope to actively pursue those assets with the best prospects in the growth portion of portfolios. And those assets look very different today than they did a year ago.

Said simply, the opportunity set has shifted, so there could be value in portfolio adjustments. By the same token, volatility can be used within a retirement portfolio to position for future outcomes. The key is timeframe—and this is even more relevant for those in retirement. Recalling the words of the legendary Sir John Templeton, “Bull markets are born on pessimism, grow on skepticism, mature on optimism, and die on euphoria. The time of maximum pessimism is the best time to buy, and the time of maximum optimism is the best time to sell.”

Be Smart About Your Withdrawal Strategy, Thinking Long Term

The obvious temptation in recessionary conditions is to tighten the wallet. This makes sense as an act of safety, but the true task of investing positively in retirement is to maximize utility. Specifically, we want to preserve capital, but not to the extent that you can’t live life (achieve goals). Short-term thinking is often the enemy here, believing that you need to act more cautiously than is required over the long run.

A positive way to handle this is to use bucketing. There are different approaches that have merit, but the central idea is to ease the mental accounting by splitting your nest egg up into short-term, medium-term, and long-term buckets. The longer-term bucket would naturally carry more risk (typically via stocks), which will move higher and lower but will top-up your shorter-term buckets over time. The beauty of doing this is that is works really well with a valuation-driven asset allocation. This means favoring cheaper assets that are fundamentally attractive, which can often take a while to harvest but tend to have higher yields. If you get this approach right consistently, it has the potential to really add to your retirement cash flow over time.

Cash Flow Matters

The ongoing debate about an income-approach versus a total-return approach continues, but in our mind it misses the point. After-tax cashflow is most important—not necessarily how you achieve it. Specifically, a retiree wants to make sure they can generate enough cashflow to meet their short term needs and any emergencies, while preserving their capital base. It shouldn’t matter whether this is generated from an asset that delivers high levels of income or by reducing the capital of an asset. In both instances, the capital base remains broadly the same (a dividend reduces the price of the share by the amount of the dividend). This dynamic only changes when the tax treatment is different for income and capital.

It is therefore not our job to predict which approach will steer investors to a better outcome in 2023—the key here is to maximize utility and always think about the total cash flow. To our way of thinking, a valuation-driven approach shines here, too. It means you focus on buying assets at a low price, boosting the cashflow generating prospects in a manner that can also keep overall risks lower (buying a low-priced asset carries less “valuation risk”). If done correctly and consistently, this can offer the best prospect for achieving your goals in retirement.

The conversation around income versus capital therefore carries nuance, which we highlight below.

- For those who prefer an income approach, we note a far wider range of assets delivering yields of above 4%. This avoids the problems of this time last year, where it required elevated levels of risk to achieve the same levels of income, such as risky high-dividend stocks and bonds with low credit quality. Some of the same challenges apply, though, with some higher-income assets exhibiting no growth in income (a risk in the face of inflation) and potentially elevated credit risk. We think yield-chasing is a cardinal sin when it is taken to the extreme, moving up the risk curve without a thorough understanding of what you own and why you own it.

- With a total-return approach in 2023, there is likely to be a greater tailwind from yield generation anyway, potentially avoiding the need to sell part of the portfolio periodically to meet your withdrawal needs. With a total cashflow mindset, one of the upsides to this approach is that you can potentially access lower-yielding assets at lower prices, which could add to your cash flows over time. For example, healthcare companies, which can offer different risk and return drivers to a portfolio.

A Wildly Better Environment for Retirees

Last year, we said in our outlook, “2022 is likely to be a difficult environment for passive-income generation, with low rates and expensive assets a common challenge… with higher inflation eroding the purchasing power of your income.” Coming into this year, we have higher yields and lower valuations, helping you with the three measures of retirement success: 1) cash-flow stability, 2) source of withdrawals, and 3) likely ending account value.

Summary of Our Asset-Allocation Views

2023 looks set to be a fascinating year. We have some new dynamics to deal with, including higher interest rates, coupled with inflation and a potential recession. We don’t expect it to be a smooth ride, but valuations look to be on much better footing, and we continue to emphasize portfolio robustness to find pockets of relative opportunity. We note our convictions are long term in nature, perhaps better considered over the course of a decade or two, which we believe will continue to empower investor success.

At Morningstar, our mission is to empower investor success, and we're pleased to offer these resources to help you provide investors with a range of options they need to save for retirement, protect their savings, and generate the income they need to fund specific goals.

Drawing on core capabilities in asset allocation, investment selection, and portfolio construction, Morningstar’s Investment Management group provides professional guidance and access to strategies that can help investors reach their financial goals. Our investment approach is designed to be risk aware, intentional, contrarian, and aligned to goals.

Advisors who use managed portfolios often find more time to grow their practice, focus on what matters to prospects, and build stronger, lasting relationships with clients. To learn more about using managed portfolios in your practice, call +1 877 626-3224 or email mp@morningstar.com to reach your regional sales representative.

Opinions expressed are as of the current date; such opinions are subject to change without notice. Morningstar Investment Management shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions or their use. This commentary is for informational purposes only. The information, data, analyses, and opinions presented herein do not constitute investment advice, are provided solely for informational purposes and therefore are not an offer to buy or sell a security. Please note that references to specific securities or other investment options within this piece should not be considered an offer (as defined by the Securities and Exchange Act) to purchase or sell that specific investment. Performance data shown represents past performance. Past performance does not guarantee future results. All investments involve risk, including the loss of principal. There can be no assurance that any financial strategy will be successful. Morningstar Investment Management does not guarantee that the results of their advice, recommendations or objectives of a strategy will be achieved. This commentary contains certain forward-looking statements. We use words such as “expects”, “anticipates”, “believes”, “estimates”, “forecasts”, and similar expressions to identify forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason. Past performance does not guarantee future results. Morningstar® Managed PortfoliosSM are offered by the entities within Morningstar’s Investment Management group, which includes subsidiaries of Morningstar, Inc. that are authorized in the appropriate jurisdiction to provide consulting or advisory services in North America, Europe, Asia, Australia, and Africa. In the United States, Morningstar Managed Portfolios are offered by Morningstar Investment Services LLC or Morningstar Investment Management LLC, both registered investment advisers, as part of various advisory services offered on a discretionary or non-discretionary basis. Portfolio construction and on-going monitoring and maintenance of the portfolios within the program is provided on Morningstar Investment Services behalf by Morningstar Investment Management LLC. Morningstar Managed Portfolios offered by Morningstar Investment Services LLC or Morningstar Investment Management LLC are intended for citizens or legal residents of the United States or its territories and can only be offered by a registered investment adviser or investment adviser representative. Investing in international securities involve additional risks. These risks include, but are not limited to, currency risk, political risk, and risk associated with varying accounting standards. Investing in emerging markets may increase these risks. Emerging markets are countries with relatively young stock and bond markets. Typically, emerging-markets investments have the potential for losses and gains larger than those of developed-market investments. A debt security refers to money borrowed that must be repaid that has a fixed amount, a maturity date(s), and usually a specific rate of interest. Some debt securities are discounted in the original purchase price. Examples of debt securities are treasury bills, bonds and commercial paper. The borrower pays interest for the use of the money and pays the principal amount on a specified date. The indexes noted are unmanaged and cannot be directly invested in. Individual index performance is provided as a reference only. Since indexes and/or composition levels may change over time, actual return and risk characteristics may be higher or lower than those presented. Although index performance data is gathered from reliable sources, Morningstar Investment Management cannot guarantee its accuracy, completeness or reliability.

Successful charitable giving plans start with “why”

Wealth Strategist Ben Rizzuto discusses the importance of understanding the motivations behind investors’ charitable giving aims and how advisors can help clients clarify and achieve their goals.

Regrets, I’ve had a few: 7 common financial regrets (and how to avoid them)

Retirement Director Ben Rizzuto explains how we can learn from the regrets of others to better prepare for the future and shares seven steps to help ensure we don’t lament our past financial decisions.

Women and savings: Your future in focus

We’re talking about women’s finances, including how to identify your goals and decide what you may need to save for the future.