A New Way to Calculate Retirement Health Care Costs

Health care costs are top of mind for every retiree or anyone who is nearing retirement. According to T. Rowe Price’s Retirement Savings and Spending study (2019), the top three spending concerns of retirees are (in order of importance): paying for long-term care services, health insurance premiums, and out-of-pocket health care expenses.1

The projected health care costs in retirement provided by some of the leading experts sound alarming. In its latest (2018) projection, the Employee Benefit Research Institute (EBRI) estimates that to have a 90% chance of covering all their health insurance premiums and out-of-pocket costs, a 65-year-old couple will need $296,000.2 And according to the most recent (2010) estimates from the Boston College Center for Retirement Research (CRR), a typical 65-year-old couple can expect to spend $197,000 over their remaining lifetime with a 5% chance that the number exceeds $311,000.3

These numbers don’t include long-term care costs, which could be catastrophic in some cases. While these numbers offer a good idea of how expensive retirement health care could be over several decades, they are not very helpful for individual financial planning. Here’s why:

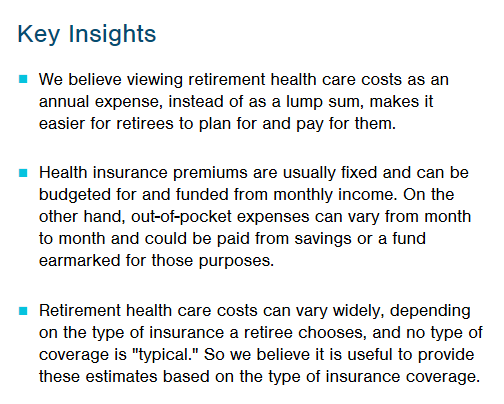

- Lump-sum estimates of health care costs covering the entire duration of retirement are not useful for budgeting and planning purposes because health care expenses are not incurred as lump sums. Individuals have to make their health care decisions based on their financial resources at any given point in time.

- There are embedded health insurance coverage assumptions in most of these calculations. Health insurance coverage varies significantly for retired Americans, even under the broad umbrella of Medicare. It is not clear if any particular type of health insurance coverage can be termed as "typical."

- Combining premiums and out-ofpocket costs tends to distort the perception of the risk of health care costs in retirement and complicates the associated financial planning. Premiums are relatively stable at the individual level, but out-of-pocket costs are more uncertain and, as a result, accounts for most of the variation in health care costs. Premiums also constitute the bulk of their health care expenses for the majority of retirees. As a result, for most retirees, a large chunk of their annual health care costs is predictable and can be easily planned for, a fact masked by the combined lifetime health care cost estimates.

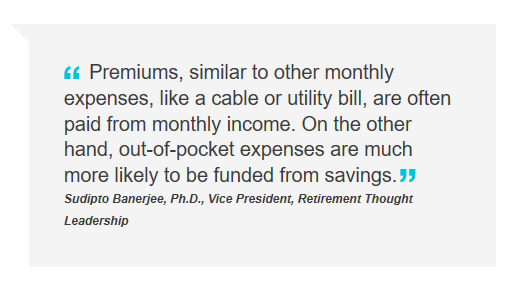

By separating the premiums and out-ofpocket costs, retirees will be able to plan better for these expenses. Premiums, similar to other monthly expenses, like a cable or utility bill, are often paid from monthly income. On the other hand, out-of-pocket expenses are much more likely to be funded from savings.

As a result, we believe that framing health care costs in retirement should be based on (at least) three factors:

1The Retirement Savings and Spending (RSS) study is a nationally representative annual survey of workers ages 21 and above who are either currently participating in a 401(k) plan or eligible to participate and have a plan balance of at least $1,000. Along with 3,000 workers, the 2019 RSS study also includes a sample of 1,000 retirees who had a rollover IRA or a left-in-plan 401(k) balance.

2Fronstin, Paul and Jack VanDerhei. “Savings Medicare Beneficiaries Need for Health Expenses: Some Couples Could Need as Much as $400,000, Up From $370,000 in 2017.” EBRI Issue Brief, no. 460 (Employee Benefit Research Institute, October 8, 2018).

3Webb, Anthony and Natalia Zhivan, March 2010. “What Is the Distribution of Lifetime Health Care Costs from Age 65?” Center for Retirement Research at Boston College, No 10-4.

This material is provided for general and educational purposes only, and not intended to provide legal, tax or investment advice. This material does not provide recommendations concerning investments, investment strategies or account types; and not intended to suggest any particular investment action is appropriate for you. Please consider your own circumstances before making an investment decision.

The views contained herein are those of the authors as of February 2020 and are subject to change without notice; these views may differ from those of other T. Rowe Price associates.

All investments involve risk. All charts and tables are shown for illustrative purposes only.

© 2020 T. Rowe Price. All rights reserved. T. Rowe Price, INVEST WITH CONFIDENCE, and the Bighorn Sheep design are, collectively and/or apart, trademarks of T. Rowe Price Group, Inc.

T. Rowe Price Investment Services, Inc., Distributor.

Plan advisors: 5 topics to discuss at your year-end investment committee meeting

Retirement Director Ben Rizzuto outlines five topics – including recent defined contribution developments and ideas for engaging plan participants – that advisors can discuss at upcoming year-end investment committee meetings.

Plan Talk: Analyzing risks and opportunities in today’s plan menu lineups

In this episode of Plan Talk, Retirement Director Ben Rizzuto speaks with Damien Comeaux, Senior Portfolio Strategist, about how the Portfolio Construction and Strategy (PCS) team analyzes plan menu lineups to help ensure they provide adequate diversification.

The Rollover Reset

Financial professionals looking to capture rollovers from DC plans need expertise in rollover-related issues like non-Roth after-tax account opportunities, special rules for Net Unrealized Appreciation, in-service plan rollovers, the Warn Act, and more. Are you ready?