Direct Indexing and the IKEA Effect

Key takeaways

- The “IKEA effect” describes a cognitive bias that happens when people put in some form of labor to complete a project or finish a creation.

- Offering personalized experiences that create an emotional attachment is not something the financial services industry has historically done well.

- Direct indexing won’t solve the behavior gap, but it has the potential to create better investor behaviors by allowing investors to play a larger role in the portfolio-building process.

- Given what we know about investor habits, direct indexing has the potential to be the next disruptive force in wealth management.

For General Educational Use Only

The “IKEA effect” describes a cognitive bias that happens when people put in some form of labor to complete a project or finish a creation. It refers to the fact that people tend to place higher values on things they create themselves.

Harvard Business School’s Michael Norton and others coined the term in a 2012 paper and define it as the “increase in valuation of self-made products.” The name itself comes from Swedish furniture retailer IKEA, which sells furniture that often requires physical assembly done by the customer.

Build-A-Bear Workshop is a unique example of this phenomenon. Build-A-Bear is a retail experience where customers walk into a store, buy a standard teddy bear off the shelf, and then have the option to add features (clothing, voice box, etc.) for an additional price. The standard teddy bear retails between $15 and $40, but after add-ons, customers often pay double the retail price, and in some cases, much more.

To the cynic, Build-A-Bear sells expensive teddy bears. But analyzing the business objectively, Build-A-Bear sells a unique experience, offering a personalized teddy bear that has the follow-on effect of creating an emotional bonding experience between the buyer and a loved one.

Business is going well: Build-A-Bear celebrated their 25th anniversary last year with the most profitable year in company history.

The financial industry would be wise to learn from a simple business concept like Build-A-Bear.

Personalization Not a Dominant Feature of Wealth Management

Offering personalized experiences that create an emotional attachment is not something the financial services industry has historically done well.

Direct indexing, one of the latest innovations in wealth management, hopes to bridge that gap.

As background, direct indexing refers to a separately managed account (SMA) that tracks an index, or a blend of indexes while holding the individual stocks that comprise the index. Said differently, mutual funds and exchange-traded funds (ETFs) are wrappers that sit between investors and the stocks they own. Direct indexing removes that wrapper and allows investors to hold the individual stocks that sit inside the index.

Standard indexes (think ETFs or mutual funds) have a single methodology—one set of rules dictating what they own and how they rebalance. In effect, they are “one size fits all.”

Like owning a standard index mutual fund or ETF, direct indexing also invests and rebalances according to a pre-determined methodology. But with direct indexing, the methodology can be personalized based on an investor’s circumstances and preferences and can be easily adjusted as circumstances change.

If an investor:

- Works for a healthcare company and wants to own a broad equity index minus healthcare stocks (to avoid the career risk associated with working in that industry), that can be implemented through direct indexing.

- Owns a large, concentrated stock position (or multiple), you can actively attempt to capture losses from individual stocks within the index, sell a portion of the concentrated stock at different intervals, and use the tax losses to offset gains from the stock sale.

- Wants a portfolio that aligns with their values, whether it's less exposure to fossil fuels or focuses on companies with more women in leadership positions, direct indexing can help facilitate that.

These are only a few examples of practical direct indexing use cases.

Direct Indexing Value Beyond Numbers

Some benefits of direct indexing can be precisely quantified, like capturing tax losses, while others cannot.

The psychological satisfaction investors can achieve from playing an active role in building their own portfolio cannot easily be measured. Nonetheless, it could be a major force in driving better investor outcomes.

Ryan Murphy, Morningstar's Global Head of Behavioral Insights, mentioned the following on the topic:

“Helping investors stay the course is a valuable service from advice providers. Building personalized direct indexing strategies may be a useful way to add to this by driving engagement and at the same time discouraging people from meddling with their allocations, especially during volatile times.”

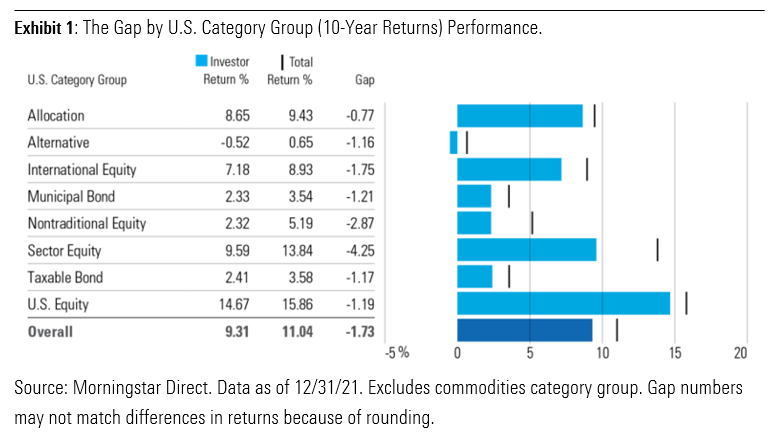

Among individual investors, the most common pitfall is buying and selling at inopportune times, which in aggregate, causes investors to underperform the indexes they invest in. Morningstar conducts an annual study “Mind the Gap,” which shows across eight asset classes that investor returns have fallen short of the category’s total returns, on average, over the past 10 years.

Peter Lynch is one of the greatest mutual fund managers of all time. His fund, Fidelity Magellan, achieved annual returns of roughly 30% from 1977–1990, but the average investor in his fund only earned roughly 8%. Reason being, investors put most of their dollars into the fund at peaks and took the most money out at troughs.

Direct indexing won’t solve the behavior gap, but it has the potential to create better investor behaviors by allowing investors to play a larger role in the portfolio-building process.

A byproduct of being involved in portfolio building should be a deeper understanding of how the portfolio is invested—an emotional connection of sorts—which could create less uncertainty during periods of market turbulence.

Given what we know about investor habits around buying and selling, this feature alone could go a long way in helping to produce better investor outcomes.

The Bottom Line

Direct indexing has the potential to be the next disruptive force in wealth management.

It’s clear that investors are interested in building portfolios that are unique to them. Whether it’s a focus on tax management, company or sector preferences, factor tilts, or other considerations, direct indexing can play a helpful role.

A customized portfolio experience also creates an additional benefit by increasing an investor’s corresponding attachment to it, which could ultimately translate to less buying and selling at the wrong time.

In effect, it ties the portfolio to the person, and we know people tend to place higher values on things they’re more connected to. And unlike Build-A-Bear, direct indexing doesn't require additional costs for additional customization.

Direct indexing takes the one-size-fits-all approach of ETF and mutual fund investing and turns it on its head, helping financial advisors add compelling value to a passive portfolio and tailor it to a client’s unique needs.

The trends in customization have permeated other industries and created stickier customer relationships—it’s about time deeper customization came to investing.

Opinions expressed are as of the current date; such opinions are subject to change without notice. Morningstar Investment Management shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions or their use. This commentary is for informational purposes only. The information, data, analyses, and opinions presented herein do not constitute investment advice, are provided solely for informational purposes and therefore are not an offer to buy or sell a security. Please note that references to specific securities or other investment options within this piece should not be considered an offer (as defined by the Securities and Exchange Act) to purchase or sell that specific investment. Performance data shown represents past performance. Past performance does not guarantee future results. All investments involve risk, including the loss of principal. There can be no assurance that any financial strategy will be successful. Morningstar Investment Management does not guarantee that the results of their advice, recommendations or objectives of a strategy will be achieved. This commentary contains certain forward-looking statements. We use words such as “expects”, “anticipates”, “believes”, “estimates”, “forecasts”, and similar expressions to identify forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason. Past performance does not guarantee future results. Morningstar® Managed PortfoliosSM are offered by the entities within Morningstar’s Investment Management group, which includes subsidiaries of Morningstar, Inc. that are authorized in the appropriate jurisdiction to provide consulting or advisory services in North America, Europe, Asia, Australia, and Africa. In the United States, Morningstar Managed Portfolios are offered by Morningstar Investment Services LLC or Morningstar Investment Management LLC, both registered investment advisers, as part of various advisory services offered on a discretionary or non-discretionary basis. Portfolio construction and on-going monitoring and maintenance of the portfolios within the program is provided on Morningstar Investment Services behalf by Morningstar Investment Management LLC. Morningstar Managed Portfolios offered by Morningstar Investment Services LLC or Morningstar Investment Management LLC are intended for citizens or legal residents of the United States or its territories and can only be offered by a registered investment adviser or investment adviser representative. Investing in international securities involve additional risks. These risks include, but are not limited to, currency risk, political risk, and risk associated with varying accounting standards. Investing in emerging markets may increase these risks. Emerging markets are countries with relatively young stock and bond markets. Typically, emerging-markets investments have the potential for losses and gains larger than those of developed-market investments. A debt security refers to money borrowed that must be repaid that has a fixed amount, a maturity date(s), and usually a specific rate of interest. Some debt securities are discounted in the original purchase price. Examples of debt securities are treasury bills, bonds and commercial paper. The borrower pays interest for the use of the money and pays the principal amount on a specified date. The indexes noted are unmanaged and cannot be directly invested in. Individual index performance is provided as a reference only. Since indexes and/or composition levels may change over time, actual return and risk characteristics may be higher or lower than those presented. Although index performance data is gathered from reliable sources, Morningstar Investment Management cannot guarantee its accuracy, completeness or reliability.

Market Perspective: There are No Rewards Without Risk

2022 reminded investors of the risk from investing, but none of this makes losses palatable. As the old axiom goes, “there are no rewards without risk.” Here's perspective from Marta Norton, CIO, Americas, Morningstar Investment Management LLC.

The Unconscious Nudge: Behavioral science and its financial implications

Over the course of this presentation, we will talk about how the brain systems work and how it impacts decisions that people make.

Understanding the Motivations for Personalized Sustainable Investing

Approaches that promote a more sustainable society and economy align to a given client’s personal view—and it’s important for an advisor to understand each client’s objectives and preferences.