The U.S. Dollar in 2020: Does the Buck Stop Here?

KEY INSIGHTS

- Following prolonged strength and a boost from the coronavirus‑induced liquidity crisis, the U.S. dollar could be heading for a long‑term downtrend soon.

- Headwinds to the dollar could include a stronger recovery in the rest of the world versus the U.S., falling interest rate premia, and easier liquidity conditions.

- There could be an opportunity for investors to add international bonds and currencies in order to diversify their portfolios and potentially boost performance.

During a volatile few years that included seismic events such as Brexit and the coronavirus pandemic, the U.S. dollar has been a pillar of strength. It has shown greater resilience than most other major currencies, providing a degree of stability for investors during an unstable period. However, there are signs that the dollar may have reached its ceiling in the first quarter as it has recently started to weaken. If this happens, investors may want to turn to other currencies as they seek to diversify their portfolios and improve performance in the second half of the year.

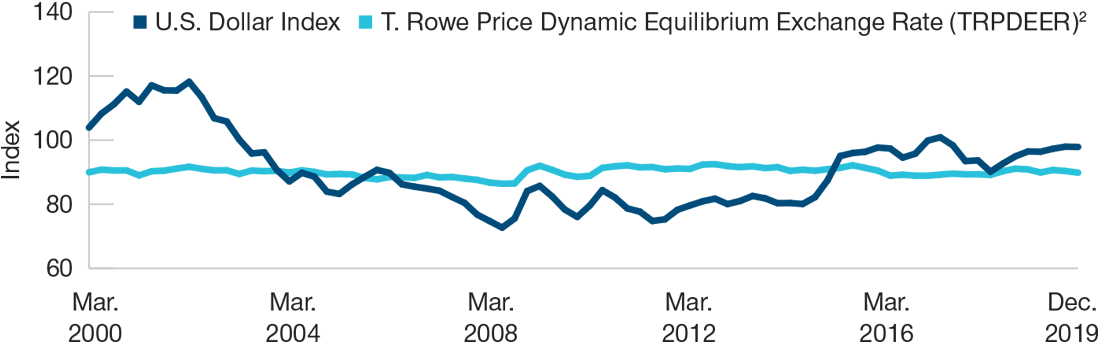

THE U.S. DOLLAR WAS OVERVALUED BY 8% AT THE START OF THE YEAR

(Fig. 1) U.S. Dollar Index1 potential misevaluation.

1 U.S. Dollar Index = Bloomberg DXY Index.

Sources: Bloomberg Finance LP and T. Rowe Price.

An Elongated Bull Run That Weighed on Foreign Currency Assets

While March’s dash for liquidity reminded the world of the dollar’s strength, the currency’s current cycle of appreciation actually began back in 2011. That year, the Fed’s quantitative easing (QE) program stopped in the second quarter, stifling the dollar supply. Elsewhere, slowing global growth, falling commodity prices, and the escalation of the eurozone debt crisis also put upward pressure on the dollar. In 2014, the dollar strengthened further when the Fed began tapering its QE program, reducing the supply of new money and boosting dollar demand. A subsequent influx of new euros, courtesy of the European Central Bank’s QE program in 2015, also bolstered the dollar’s relative value.

However, while the dollar’s run was driven by these technical factors early on, it has since been buoyed mainly by external factors. These include lower growth in Europe and China and the shift in the American crude oil balance on the back of lower global prices and increased U.S. oil production. March 2020’s dollar spike served as a reminder of how useful the currency is in a crisis: Since the beginning of 2015, the U.S. Dollar Index (DXY)—a measure of the dollar’s value against a basket of foreign currencies—has typically ranged between 90 and 100, but it exceeded 100 (indicating the dollar is strengthening against other currencies) during the market sell‑offs in the fourth quarter of 2015, the first quarter of 2016, and in March this year.

"The coronavirus may mark the dollar’s final peak in this uptrend before it reverses course."

Overall, this current cycle has suppressed the value of investments in foreign currency assets in U.S. dollar terms. The downward pressure on foreign currencies has also reduced the luster of foreign currency bonds given that many investors instinctively view their wealth in dollar terms.

The Beginning of the End—Signs of Overvaluation

The coronavirus crisis may, however, mark the dollar’s final peak in this uptrend before it reverses course. Indications prior to the pandemic suggested that the dollar may have reached the end of its upward trajectory. Indeed, at the end of 2019, T. Rowe Price found the dollar to be overvalued against 26 other currencies, nine from developed markets and 17 from emerging markets. Overall, according to our modelling, the dollar was implied to be 8% overvalued.

The events of this year have only served to increase the market value of the dollar given its perceived safe‑haven status. However, following March’s spike, the currency has declined, and four key factors suggest that the dollar could be facing a sustained period of depreciation ahead:

1. The Start of a New Cycle Could Drive a Reversal of Fortune

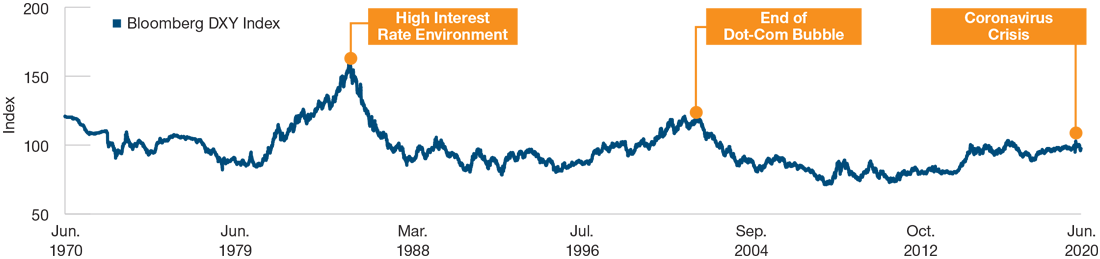

Although short‑term peaks and troughs can happen during broader uptrends and downtrends, there is reason to believe the current cooling of the dollar could be the start of a fresh downward cycle. Previous dollar bull runs have tended to last several years before falling back. The most significant of these occurred in the early 1980s when the Federal Reserve increased interest rates to 20% in a bid to ward off “stagflation” (an environment of persistent economic sluggishness and high inflation). From its trough in October 1978, the DXY rose by more than 52% by March 1985.

After recalibrating in the late 1980s and early 1990s, the dollar once again surged toward the end of the millennium. This was prompted by the flurry of interest in U.S.‑based tech companies in the late 1990s, which boosted the DXY by more than a third from July 1995 to February 2002. However, as the tech frenzy died down, equity markets fell, and the U.S. Federal Reserve cut rates to a (then unprecedented) 1%, the dollar pulled back. With this in mind, it is worth noting that prior to the pandemic, the U.S. dollar’s strong run was concurrent with near‑record highs in U.S. equity indices such as the Nasdaq.

2. The U.S. Path to Economic Recovery Looks Uncertain

The possibility of a global growth rebound in the second half of the year could also weaken the dollar. Given its status as the world’s biggest currency, the U.S. dollar’s ups and downs are influenced by wider global sentiment: Strong U.S. economic performance relative to the rest of the world, a hawkish Fed, and a low risk appetite are generally indicative of a stronger dollar; relatively slower U.S. growth, a more dovish Fed, and a brighter outlook for international markets often coincide with a weakening U.S. dollar. As we look ahead to a post‑coronavirus global economy, there are indications that we may be moving from the former environment to the latter.

"...the evaporation of this interest rate differential makes the U.S. dollar much less attractive to hold..."

At face value, economic and sentiment data across the board appear eye‑wateringly bad. However, despite some record lows in April, it is likely that some countries are over the worst of the crisis. The first countries to impose lockdowns in Asia and Europe have reopened, led by China, which restarted its manufacturing industry as early as March. Eurozone purchasing managers’ indexes (PMI) indicated a hefty rebound in May, although they remain in contraction territory; and, encouragingly, services sectors are reopening in some of the hardest‑hit areas, such as Spain and Italy. Additionally, the European Union’s massive stimulus plan has provided a strong signal of the bloc’s commitment to rebuilding, which should be positive for the euro.

While the U.S. is also reopening, its path to normalized growth remains a concern: Infection numbers in the country remain high and far outstrip the rest of the world, the risk of a second outbreak remains quite real, and the reopening of the economy is likely to be extremely gradual. Sentiment data also hint at a relative lack of optimism for a fast recovery, with May’s PMI scores lagging on weak production and new orders. This is not to say the U.S. is destined to lag the rest of the world in recovery returns, but it does make it likely that—at the very least—the era of “U.S. exceptionalism” of the past few years is coming to an end, threatening the dollar’s place on the pedestal.

3. No More Rate Differential

The removal of one of the more enticing reasons for holding the dollar, namely its higher interest rate compared with other peers, could also see the dollar slide. In 2017 and 2018, the Fed hiked interest rates seven times, while other major central banks remained on an easing trajectory. This helped the dollar to rally as higher interest rates tend to increase the relative value of a currency.

However, in 2019, the Fed reversed course, trimming rates three times during the year and committing to buying USD 60 billion in Treasury bills per month. This year, as the coronavirus crisis spread, the central bank eased further by cutting rates to near zero, bringing its rate much closer to ones seen in other developed markets such as the eurozone and Japan. Additionally, the Fed has expanded its QE buying programs, supplying trillions of dollars to the market.

From a currency perspective, the evaporation of this interest rate differential makes the U.S. dollar much less attractive to hold from an investor’s point of view as the “carry” now earned (the return received from holding it versus other currencies) is much less and, in some cases, negligible. Indeed, since the Fed has cut rates to near zero, outside of a major liquidity squeeze in late March, the U.S. dollar has fallen back to January levels.

"The political landscape, while muddled, also poses questions for the currency."

Furthermore, the Fed’s efforts to increase the supply of dollars internationally via foreign exchange swap lines have also played a part in the currency’s fall. Following its coordinated move with the Bank of Japan, European Central Bank, Swiss National Bank, Bank of Canada, and Bank of England to tap lines and boost dollar liquidity in mid‑March, the Fed opened swap lines with a further nine countries later in the month to improve access to the world’s reserve currency. While this was done, as the Fed put it, “to help lessen strains in global U.S. dollar funding markets,” a byproduct of this was to put downward pressure on dollar value by increasing supply.

The shifting composition of central banks’ foreign exchange reserves may also indicate that the U.S. dollar is on a downward path. A number of institutions, such as the Bank of Russia, have been actively trying to reduce transactions made in the currency, while central bankers such as Mark Carney, who up until March was the governor of the Bank of England, have said the dollar’s role in the global financial system should be reduced.

4. Waning Status—USD Declines as Percentage of Global Reserves

Indeed, there are signs that this is already happening. According to figures from the International Monetary Fund, the currency accounted for around 57% of central bank reserves at the end of 2019; however, during that year, the amount of U.S. dollars held fell as a percentage of global reserves, while currencies such as the euro, the Chinese yuan, the British pound, and the Japanese yen all gained share over the same period, despite the fact that the U.S. dollar was a much higher‑yielding currency at the time. Last year, China also reduced the weight of the dollar in the renminbi basket by 0.8% (1.5% including the Hong Kong dollar), boosting weights of the euro, Australian dollar, and Russian ruble.

The political landscape, while muddled, also poses questions for the currency. Given criticisms of governments worldwide during the coronavirus crisis, the outcome of the upcoming U.S. presidential election is more uncertain than it appeared just a few months ago. Should Democratic nominee Joe Biden win, or even if that outcome appears more likely as we near polling day, the dollar could see a period of weakness on the expectation that the protectionist policies of the current Donald Trump‑led administration will be rolled back.

IS IT TIME FOR THE DOLLAR TO TURN?

(Fig. 2) It could be reaching the point when previous rallies reversed.

Sources: Bloomberg Finance LP, data analysis by T. Rowe Price.

Why Now Might Be the Time to Diversify Currency Exposures

Despite these factors, there is no guarantee that the dollar will decline. The currency still retains safe‑haven properties and liquidity value, something highly valued in uncertain times. Should the coronavirus pandemic extend beyond the summer through secondary outbreaks or a meager rebound, expect investors to look favorably upon the dollar once more. Even if U.S. data become bad enough to warrant lower interest rates for longer by the Fed, it is possible that any fall in demand for the dollar due to the fall in rate differential would initially be offset by the rise in demand for U.S. Treasuries and other U.S. dollar‑denominated low‑risk financial assets. Additionally, a reigniting of U.S.‑China trade tensions could lead to more protectionism in the near future, and thus buoy the dollar, while history tells us that rebounds in Europe and Japan are not guaranteed.

However, as we approach 10 years into the dollar bull run, and global growth shows signs of returning after the coronavirus crisis, investors should consider whether a diversifying shift from U.S. dollar‑denominated assets to international bonds could be a smart move as we approach the second half of the year.

WHAT WE’RE WATCHING NEXT

How U.S.‑China tensions unfold in the runup to the U.S. presidential election later this year is one of three key factors we are looking at in the future in terms of where the dollar will head. Elsewhere, our attention is also focused on the possible increase in corporate and household bankruptcies following the conclusion of fiscal support this summer. Finally, we will be keeping an eye on news on the public health front—in particular, we will monitor the likelihood of a second wave of virus infections or a more rapid discovery of a vaccine/therapeutics.

Important Information

This material is provided for informational purposes only and is not intended to be investment advice or a recommendation to take any particular investment action.

The views contained herein are those of the authors as of July 2020 and are subject to change without notice; these views may differ from those of other T. Rowe Price associates.

This information is not intended to reflect a current or past recommendation concerning investments, investment strategies, or account types, advice of any kind, or a solicitation of an offer to buy or sell any securities or investment services. The opinions and commentary provided do not take into account the investment objectives or financial situation of any particular investor or class of investor. Please consider your own circumstances before making an investment decision.

Information contained herein is based upon sources we consider to be reliable; we do not, however, guarantee its accuracy.

Past performance is not a reliable indicator of future performance. All investments are subject to market risk, including the possible loss of principal. International investments can be riskier than U.S. investments due to the adverse effects of currency exchange rates, differences in market structure and liquidity, as well as specific country, regional, and economic developments. Fixed-income securities are subject to credit risk, liquidity risk, call risk, and interest-rate risk. As interest rates rise, bond prices generally fall. Diversification cannot assure a profit or protect against loss in a declining market. All charts and tables are shown for illustrative purposes only.

T. Rowe Price Investment Services, Inc.

© 2020 T. Rowe Price. All rights reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the bighorn sheep design are, collectively and/or apart, trademarks or registered trademarks of T. Rowe Price Group, Inc.

Peeling back the onion: A concentric approach to investment decision making

Portfolio Managers Greg Wilensky and Jeremiah Buckley offer a framework for interpreting economic news for investment decision making.

What is ESG and why do we care?

Michelle Dunstan, Janus Henderson’s Chief Responsibility Officer, explores ESG considerations and highlights how ESG integration helps Janus Henderson deliver on client goals and aspirations.

Hiding in plain sight: The investment case for healthcare

Though healthcare may have flown under the market’s radar this year, the sector’s attractive valuations and new growth opportunities are not to be overlooked, say Portfolio Managers Andy Acker and Dan Lyons.