US core fixed income: Better positioned going into 2023?

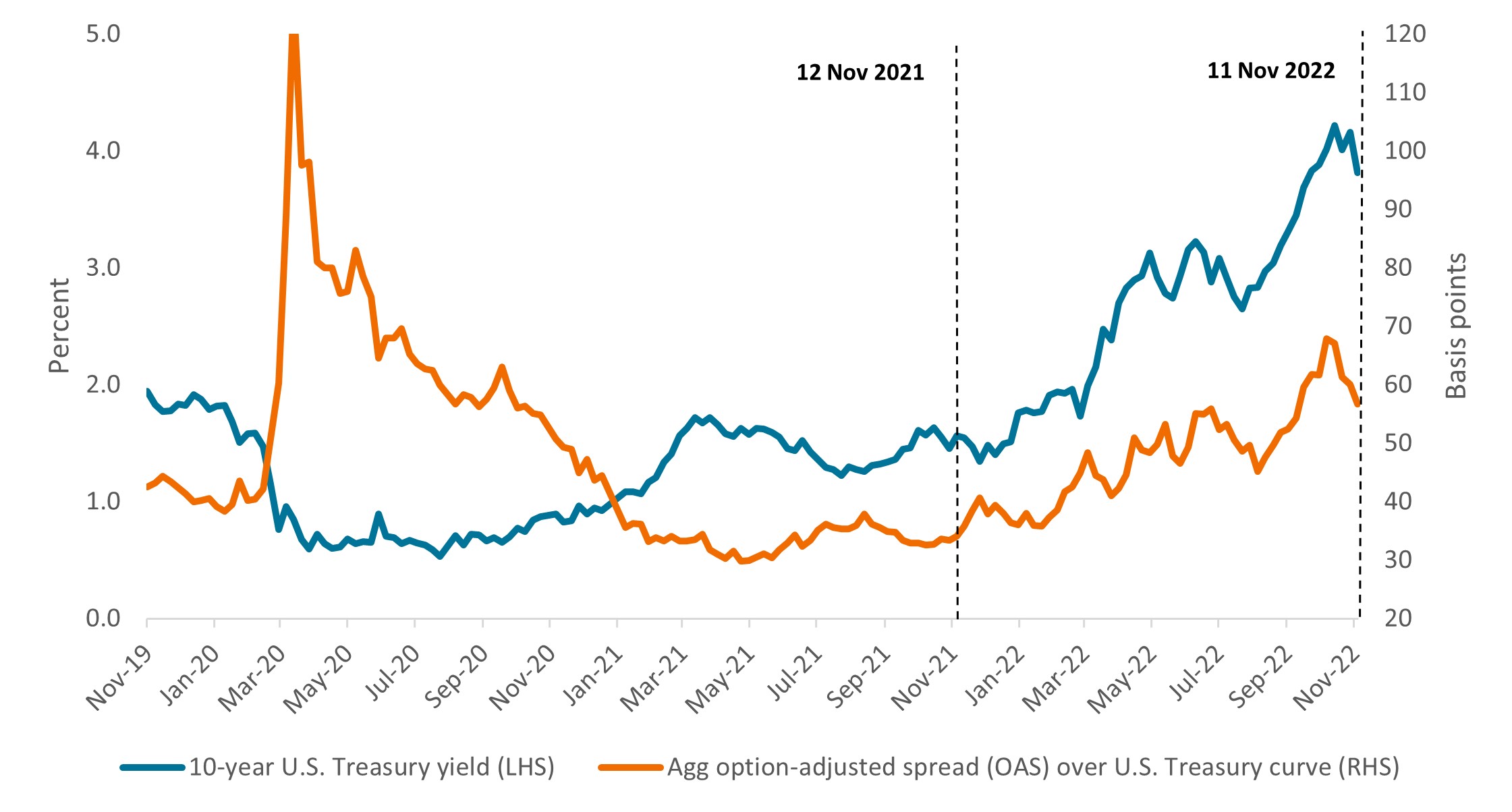

As we look toward 2023 and consider the prospects for U.S. core fixed income in the year ahead, it seems appropriate to first reflect on where we stood just one year ago. The two drivers of fixed income asset prices – interest rates and spreads – were in a very different place heading into 2022, as shown in Exhibit 1. While yields had risen off their COVID-era floor, they were still at historically low levels, supported by the Federal Reserve’s (Fed) prevailing zero interest-rate policy and $120 billion per month in quantitative easing (QE). At the same time, spreads were extremely tight, as record government stimulus had bolstered balance sheets, the economy had recovered from COVID shutdowns, and there was an increased risk appetite among investors.

Today, U.S. core fixed income is in a very different place – perhaps more beaten down after a tough year, but also, in our view, better positioned for positive risk-adjusted returns. While spread widening has taken place, the more significant development has been the sharp rise in yields, driven by the Fed’s aggressive pivot to monetary tightening in its attempt to rein in runaway inflation.

Exhibit 1: What a difference a year makes

Higher yields and spreads imply a better starting point heading into 2023.

Source: Bloomberg, as of 11 November 2022. The Bloomberg U.S. Aggregate Bond Index (Agg) is a broad-based measure of the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. Option-Adjusted Spread (OAS) measures the spread between a fixed-income security rate and the risk-free rate of return, which is adjusted to take into account an embedded option.

Rates: Inflation still holds the key

Notwithstanding the fact that we are starting from a better place, where we go from here will likely hinge on how rapidly (or slowly) inflation comes down. While goods inflation was largely driving higher prices in 2021, services and wage inflation – which tends to be stickier – has recently taken the lead. In response, the Fed has moved aggressively this year, hiking rates to 4.00% so far to cool the economy and the tight labor market.

The looming question is how much weakness we will need to see in the economy, and specifically in the labor market, to bring down wages and service sector inflation. If wages and services inflation display a high correlation to economic and labor market weakness, this could be positive for bond prices, as the Fed will likely not have to raise rates as far, or for as long, and the economic pain can ostensibly be contained. However, if the correlation is lower and inflation remains sticky despite a cooling economy, the Fed may be forced to go higher and remain there for longer. In that scenario, we would probably see a deeper recession and higher default rates, resulting in more economic pain. In our view, this is the most underappreciated risk in markets today – that inflation could be slow to come down even as the economy weakens.

That said, we did see inflation come down slightly recently, with October’s core inflation reading coming in at 6.3% year over year, down from its 6.7% peak in September. While it is promising to see some peaking in the underlying drivers of higher prices, we will need to see inflation continue to fall for several months before concluding that it’s trending down. We are still a long way from 2%, and seldom does a data series move linearly. Therefore, cautious optimism might be the best way for investors to approach their rate expectations in the coming year.

Spreads: Opportunities in securitized

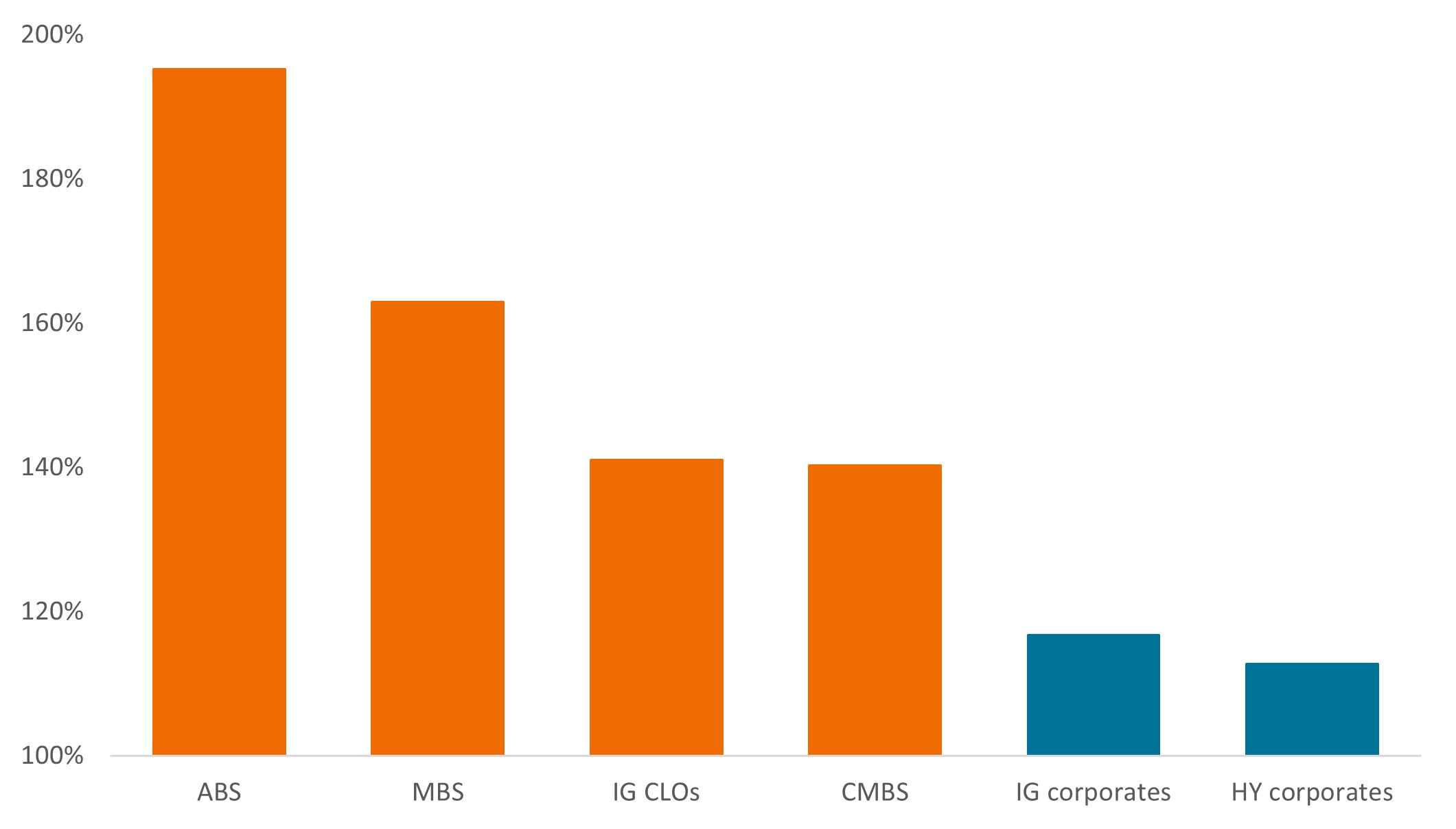

While we’ve witnessed some spread widening across all sectors in 2022, the magnitude thereof has been bifurcated. Notably, spreads on securitized assets have widened substantially more than spreads on corporate bonds, as shown in Exhibit 2. In our view, spreads on securitized sectors imply they are being priced for a recession, whereas corporates are trading only slightly above their 10-year averages. Therefore, we think this is an excellent relative value trade. If we do go into a recession in 2023, corporate spreads are likely to widen to reflect the risks that securitized assets are already pricing in. If a recession does not materialize, then we think securitized spreads should tighten even more, providing a tailwind for returns in those sectors.

Exhibit 2: Current spread as a percentage of 10-year average spread

Relative to corporates, securitized sectors are trading much wider than their 10-year averages.

Source: Bloomberg, as of 11 November 2022. Indices used to represent asset classes: ABS (Bloomberg U.S. Agg ABS Index), MBS (Bloomberg U.S. MBS Index), IG CLOs (JP Morgan CLOIE Investment-grade Index), CMBS (Bloomberg U.S. CMBS Investment Grade Index), IG corporates (Bloomberg U.S. Corporate Investment Grade Index), HY corporates (Bloomberg U.S. Corporate High Yield Index). Index performance does not reflect the expenses of managing a portfolio as an index is unmanaged and not available for direct investment.

Long-term opportunity and short-term volatility

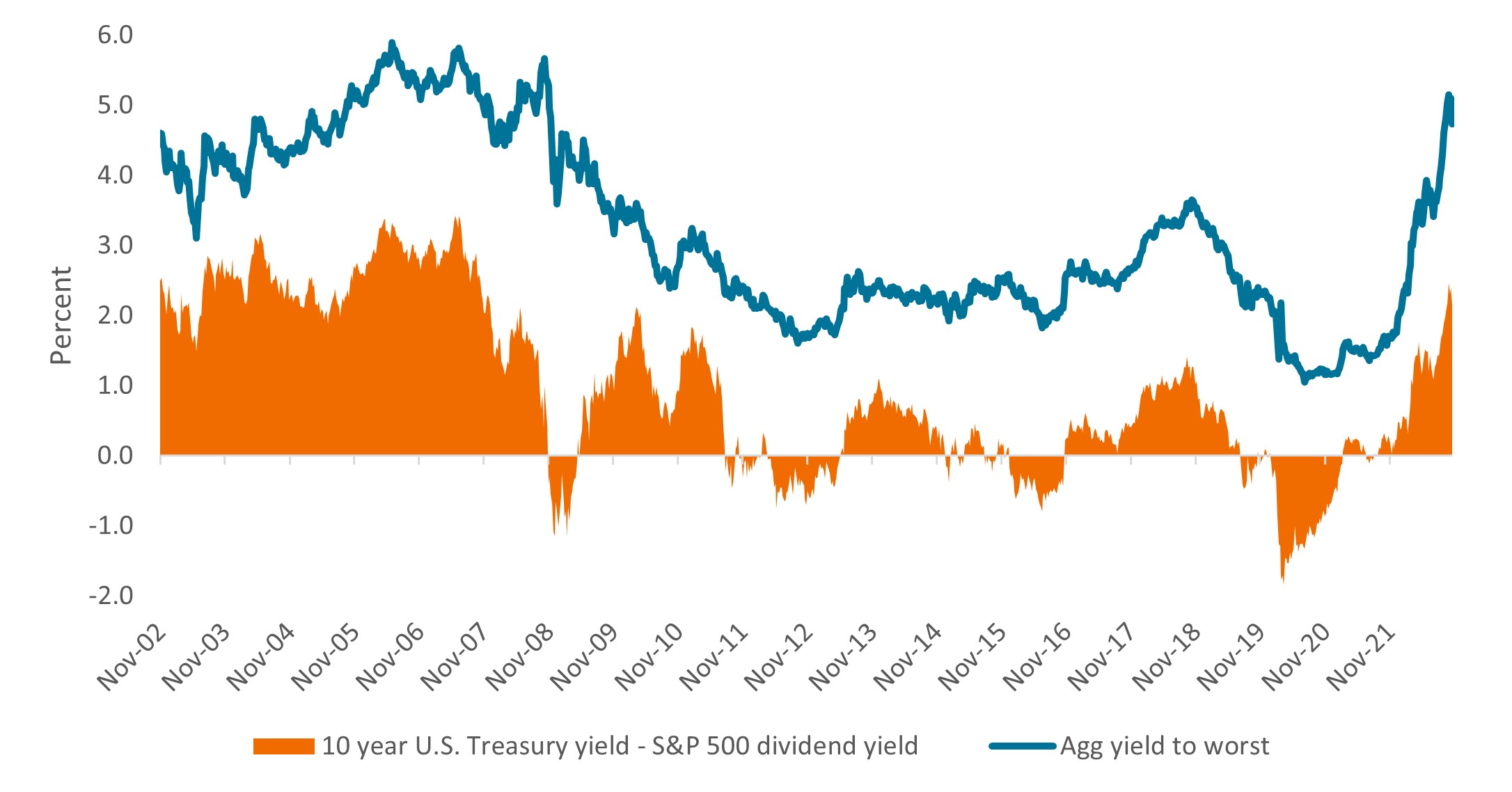

While the short-run view remains cloudy, we believe the long-run view for fixed income looks quite sunny. As previously mentioned, the starting point of higher yields – due to a combination of higher Treasury yields and wider spreads – will have a significant impact on expected intermediate and long-term returns. As shown in Exhibit 3, fixed income looks more attractive in both absolute and relative terms than it has since the Global Financial Crisis. Investors are finally getting the “income” they expect from their fixed income allocations, and TINA (there is no alternative to stocks) can no longer claim to be the prevailing mantra.

Exhibit 3: Bonds look attractive again in absolute and relative terms

Source: Bloomberg, Janus Henderson Investors, as of 11 November 2022.

On a final note, we do expect market volatility to continue in 2023, although we anticipate it will come down as the Fed gets closer to the end of its rate hiking cycle. While higher volatility in the short run can be unnerving for investors, it can be seen as an opportunity for active managers to add assets at favorable prices in pursuit of better risk-adjusted returns. The key here is to maintain a nimble, research-driven approach, and to be disciplined in executing one’s strategy.

Footnotes and definitions

Bond prices generally move in the opposite direction of interest rates, thus bond prices may decline as interest rates rise, and vice versa.

Collateralized Loan Obligations (CLOs) are debt securities issued in different tranches, with varying degrees of risk, and backed by an underlying portfolio consisting primarily of below investment grade corporate loans. The return of principal is not guaranteed, and prices may decline if payments are not made timely or credit strength weakens. CLOs are subject to liquidity risk, interest rate risk, credit risk, call risk and the risk of default of the underlying assets.

Credit Spread is the difference in yield between securities with similar maturity but different credit quality. Widening spreads generally indicate deteriorating creditworthiness of corporate borrowers, and narrowing indicate improving.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

Quantitative Easing (QE) is a government monetary policy occasionally used to increase the money supply by buying government securities or other securities from the market

Securitized products, such as mortgage- and asset-backed securities, are more sensitive to interest rate changes, have extension and prepayment risk, and are subject to more credit, valuation and liquidity risk than other fixed-income securities.

Volatility measures risk using the dispersion of returns for a given investment.

IMPORTANT INFORMATION

Collateralized Loan Obligations (CLOs) are debt securities issued in different tranches, with varying degrees of risk, and backed by an underlying portfolio consisting primarily of below investment grade corporate loans. The return of principal is not guaranteed, and prices may decline if payments are not made timely or credit strength weakens. CLOs are subject to liquidity risk, interest rate risk, credit risk, call risk and the risk of default of the underlying assets.

Fixed income securities are subject to interest rate, inflation, credit and default risk. The bond market is volatile. As interest rates rise, bond prices usually fall, and vice versa. The return of principal is not guaranteed, and prices may decline if an issuer fails to make timely payments or its credit strength weakens.

Securitized products, such as mortgage- and asset-backed securities, are more sensitive to interest rate changes, have extension and prepayment risk, and are subject to more credit, valuation and liquidity risk than other fixed-income securities.

The opinions and views expressed are as of the date published and are subject to change. They are for information purposes only and should not be used or construed as an offer to sell, a solicitation of an offer to buy, or a recommendation to buy, sell or hold any security, investment strategy or market sector. No forecasts can be guaranteed. Opinions and examples are meant as an illustration of broader themes, are not an indication of trading intent and may not reflect the views of others in the organization. It is not intended to indicate or imply that any illustration/example mentioned is now or was ever held in any portfolio. Janus Henderson Group plc through its subsidiaries may manage investment products with a financial interest in securities mentioned herein and any comments should not be construed as a reflection on the past or future profitability. There is no guarantee that the information supplied is accurate, complete, or timely, nor are there any warranties with regards to the results obtained from its use. Past performance does not predict future returns. Investing involves risk, including the possible loss of principal and fluctuation of value.

Janus Henderson Group plc ©

Weekly Fixed Income Commentary: Treasury yields rise on hawkish Fed comments

U.S. Treasury yields rose again amid hawkish rhetoric from U.S. Federal Reserve officials and continued strong U.S. economic data.

Weekly Fixed Income Commentary: Treasury yields rise on surprising inflation data

U.S. Treasury yields rose again last week after U.S. inflation data surprised to the upside, sparking a reassessment of near-term U.S. Federal Reserve rate cuts. The market is now pricing only 1.8 total cuts this year.

Weekly Fixed Income Commentary: Strong employment data boost Treasury yields

U.S. Treasury yields rose on strong U.S. economic data, and spread sectors generally outperformed. The overall solid data further reduced expectations for near-term U.S. Federal Reserve easing, though markets still price the first rate cut for June.