Uncertainty Increases

PREVIEW

As events in Ukraine see geopolitical tensions mount, the lack of an easy route to a stable resolution suggests that the impact of energy prices may persist. At the very least it compounds the uncertainty from an already challenging growth, inflation and policy mix. Policymakers seem to be walking a tightrope.

In attempting to navigate the challenges that the global economy and markets face, we need to be aware of our visceral response to shocking geopolitical developments. We continue to take proper note of rising uncertainties but resist any temptation to trade on short-term news flow or emotions.

MAJOR THEMES DRIVING OUR VIEWS

- Growth slowing towards trend

Growth is decelerating, and the risks are skewed to the downside, accentuated by the impact of geopolitics, Omicron and policy tightening. Broadly, consumers in developed economies remain in a strong financial position. A period of above-trend global expansion is still anticipated through the year.

- A challenging inflation environment

Ongoing supply bottlenecks are boosting inflation and hopes of these pressures peaking is now being challenged by energy shocks. Global inflation continues to exceed expectations, pulled higher by demand for goods. Cyclical pressures are overwhelming secular disinflationary forces, such as technology and globalization.

- Policy tightening away from highly accommodative conditions

For most central banks, the current geopolitical and economic situation increasingly feels like walking a tightrope. However, if growth disappoints, or geopolitical risks escalate further, policy may sway dovish. Even after the expected hikes, central bank rates will remain low or negative in real terms.

PRACTICAL POSITIONING

- Nimble management still required

Over a longer-term horizon, we believe global stocks still have greater performance potential than global bonds. Having tempered our equity preference to a more modest level, ahead of a sharp correction in global markets, we maintain our level of conviction but believe that a nimble investment style remains appropriate.

- Opportunities across equity markets

We are drawn to a diversified set of opportunities across equity markets, which supports our continued allocation preference toward stocks. We hold moderate conviction on the relative merits between these markets and regions, but in none do the local idiosyncrasies offset the broad appeal of equities over the longer term.

- Bonds still have a place

Our longer-term analysis shows that the return potential from global bonds, especially government bonds, remains depressed. However, the potential diversification attractions of lower-risk assets will remain evident for multi-asset investors. Strong growth supports the fundamental attractions of lower-rated fixed income sectors such as high-yield bonds and loans.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. The positioning of a specific portfolio may differ from the information presented herein due to various factors, including, but not limited to, allocations from the core portfolio and specific investment objectives, guidelines, strategy and restrictions of a portfolio. There is no assurance any forecast, projection or estimate will be realized. Stock prices fluctuate, sometimes rapidly and dramatically, due to factors affecting individual companies, particular industries or sectors, or general market conditions. Bond prices generally move in the opposite direction of interest rates. Thus, as the prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Investments in emerging markets, of which frontier markets are a subset, involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Because these frameworks are typically even less developed in frontier markets, as well as various factors including the increased potential for extreme price volatility, illiquidity, trade barriers and exchange controls, the risks associated with emerging markets are magnified in frontier markets. Derivatives, including currency management strategies, involve costs and can create economic leverage in a portfolio which may result in significant volatility and cause the portfolio to participate in losses (as well as enable gains) on an amount that exceeds the portfolio’s initial investment. A strategy may not achieve the anticipated benefits, and may realize losses, when a counterparty fails to perform as promised. Currency rates may fluctuate significantly over short periods of time and can reduce returns. Investing in the natural resources sector involves special risks, including increased susceptibility to adverse economic and regulatory developments affecting the sector—prices of such securities can be volatile, particularly over the short term. Investment in the commercial real estate sector, including in multifamily, involves special risks, such as declines in the value of real estate and increased susceptibility to adverse economic or regulatory developments affecting the sector.

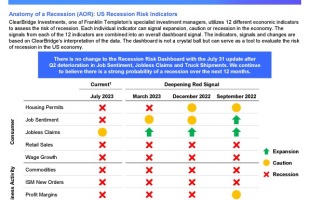

Anatomy of a Recession Update: Cracks in the Foundation

Get perspective on the most recent US economic data, the investor’s view, and how reviewing previous recessionary periods may help us today, in this conversation with Jeff Schulze, Head of Economic and Market Research at ClearBridge Investments.

AOR Update: When to expect a recession?

ClearBridge Investments: Despite improving economic sentiment now leaning the consensus view toward a soft landing, we continue to believe a recession is on the horizon.

Anatomy of a Recession: Economic and Market Outlook 3Q 2023 | August 1st

ClearBridge Investments, one of Franklin Templeton’s specialist investment managers, utilizes 12 different economic indicators to assess the risk of recession.