Investment Strategy Commentary: Cryptocurrencies

Download this article: View PDF

Cryptocurrencies have captured investor attention due to sky-high historical returns. We think a good analogy to today’s crypto market is the tech stock bubble of the late 1990s. Underpinning both was a fundamental revolution – the explosion of the internet in the late 90s, and the emergence of blockchain technology this cycle. Like the late 90s, there will likely be casualties as the early pioneers fade away. But the potential economic efficiencies of blockchain technology are likely to lead to some big winners as well.

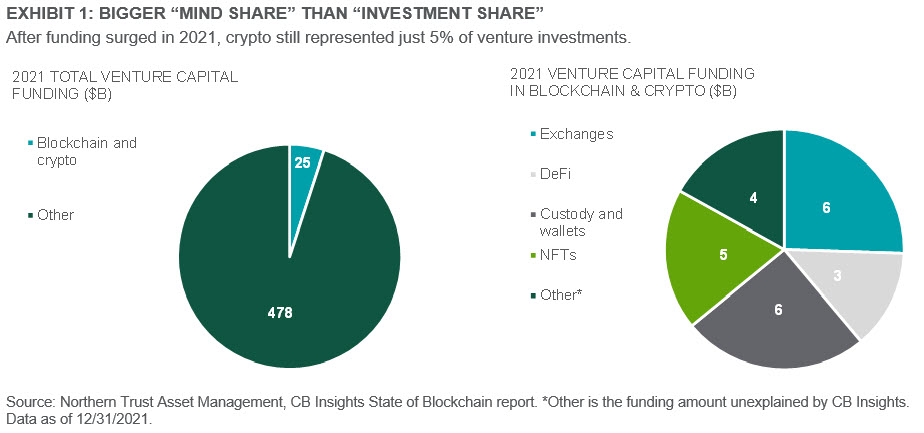

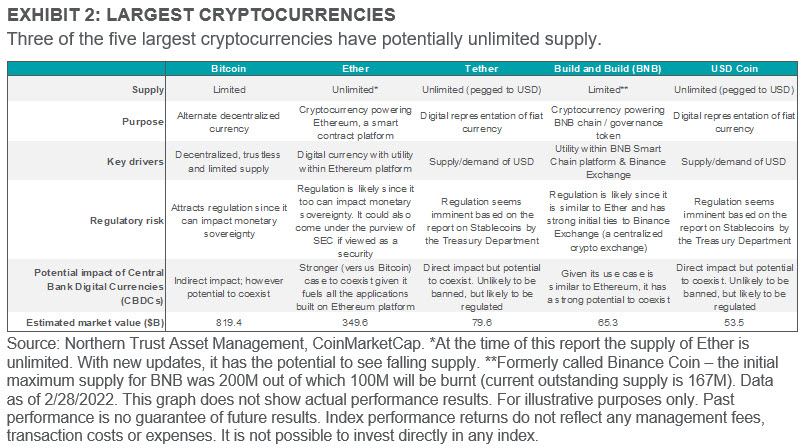

Bitcoin’s annualized return of over 150% the last 10 years has understandably generated booming interest in cryptocurrencies. In this report we will put “crypto” into perspective and analyze its effect on historical portfolio returns and risk. We will use Bitcoin as a crude proxy for all cryptocurrencies as it has the most robust historical pricing data. This probably flatters all cryptocurrencies as Bitcoin’s capped supply arguably makes it a more attractive long-term asset than some of the other leading crypto coins (see Exhibit 2). Exhibit 1 demonstrates our view that crypto has a much bigger share of media attention than investors’ wallets, as investment across blockchain and crypto technologies captured just 5% of overall venture capital investment in 2021. Another perspective is that the total value of all cryptocurrencies globally is currently just shy of $2 trillion, or 25% below the market cap of Apple Inc.

First – a disclaimer. We don’t profess to be crypto experts. The fact that this is a vast, fast moving area required that we focus our research on something we could tackle and that would also have utility. We settled on assessing the impact of including cryptocurrencies in a diversified portfolio. But there might just be an advantage to being an outsider in this situation – asking a cryptocurrency expert whether it makes sense to own crypto is probably like asking an emerging markets equity manager if they like emerging market stocks. The answer is likely to be yes.

One of the key observations from our work is the opportunities brought about by the crypto revolution go way beyond cryptocurrencies themselves. This includes areas like smart contracts, decentralized finance (defi), non-fungible tokens (NFTs) and the metaverse. Much of the investment opportunity in these areas resides in private markets which can only be accessed through venture capital or private investment. So, from a public market standpoint we are left with looking at what is accessible – and that is principally cryptocurrencies (for convenience, we will often refer to cryptocurrencies as coins). And this is no simple landscape – according to coinmarketcap.com (a respected crypto industry source) there are currently more than 17,000 cryptocurrencies (see prior comment about the eventual casualties of early pioneers). The current total value of digital coins globally is $1.9 trillion, with Bitcoin representing 40% of the value and the top 10 in total representing 80%.

We have approached this project from the vantage point of an investor – with a fiduciary responsibility over the portfolio they oversee. Critical to that analysis is an understanding of how to value an asset; what portfolio purpose it serves; and an understanding of the impact on the portfolio’s risk and return.

ASSESSING THE DIFFERENT TYPES OF CRYPTOCURRENCIES

We broadly categorize cryptocurrencies into three groups – those with limited supply (e.g., Bitcoin), those with potentially unlimited supply (e.g., historically Ether; Dogecoin) and those with unlimited supply but a peg to a fiat currency (e.g., Tether). Another industry categorization includes three groups – Bitcoin, Stablecoins (coins designed to have a stable value), and Altcoins (all other coins).

Intellectually, the long-term appreciation value of a cryptocurrency seems more appealing when the supply is limited (e.g., Bitcoin). But the landscape is quickly changing, and new altcoins with different characteristics are introduced seemingly daily. In fact, Ether has the potential to go from a currently unlimited supply to a decreasing supply in the future. Stablecoins have the attractive feature of a more predictable value but could be made obsolete by the issuance of Central Bank Digital Currencies. That said, if the stablecoin is properly collateralized, it shouldn’t lose value in this circumstance. Let’s turn to the task of analyzing the role of cryptocurrencies as an asset and in an asset allocation framework.

CRYPTO DOESN’T LEND ITSELF TO TRADITIONAL FINANCIAL ANALYSIS

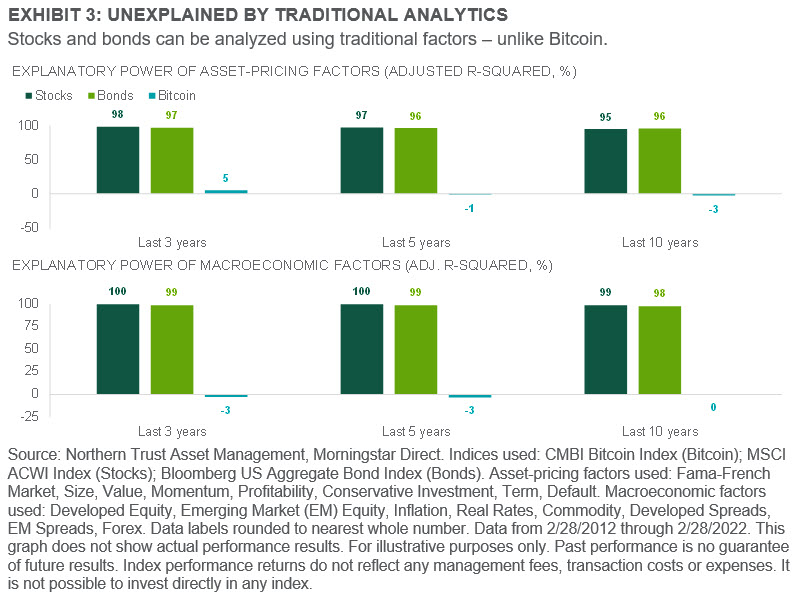

One of the biggest challenges in analyzing cryptocurrencies is understanding what drives their risk and return. One of Warren Buffett’s lessons is to never invest in businesses you don’t understand (or can’t price) – otherwise you are speculating. In this vein, many investors rely on risk factor models to help understand the key risk drivers of assets held, as well as assets worth considering for investment. But when these models are used to evaluate cryptocurrencies, they fail at providing any explanation behind what drives the variability of its performance. Exhibit 3 highlights the use of two of the most used risk factor models; one using the popular Fama-French asset-pricing factors and the other using a suite of macroeconomic state variables. For stocks and bonds, both risk factor models succeed at explaining more than 95% of the risks of traditional assets. However, they offer no useful insights into what drives Bitcoin’s price action. A crypto enthusiast would likely argue that this supports the investment – Bitcoin is that unique and represents a very idiosyncratic asset. However, from a fiduciary standpoint, if the asset is not influenced in any way by traditional methods of asset pricing or economic factors, it could be difficult to justify ownership – especially in the case of a bad outcome.

Another factor complicating a valuation analysis of coins is the rapidly changing regulatory environment. China effectively banned cryptocurrencies in 2021, starting with the prohibition of financial institutions engaging in crypto transactions; then banning crypto mining; and then finally a broad outlawing of crypto in September 2021. Countries are worried about losing control of their monopoly on monetary policy, as well as the environmental impact of coin mining. China has pivoted toward promoting the usage of its own digital yuan currency. For Bitcoin enthusiasts, these actions may just reinforce its outsider image – but it doesn’t seem these moves are constructive longer-term for broader adoption of independent coins. Technological advancement is another significant uncertainty facing the future value of individual coins. Bitcoin has a great head start, which may prove durable – but it isn’t immune to technological risk. The term “Flippening” captures this risk where Ether’s greater ease of use leads it to surpass Bitcoin. And “ETH Killers” are those blockchain systems that have the potential to overtake Ether (such as Solana, Dot and Avax).

CRYPTOCURRENCY’S ROLE IN A PORTFOLIO

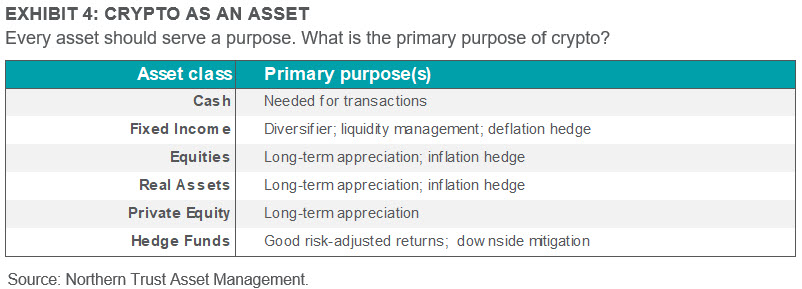

Let’s turn to a discussion of cryptocurrencies and their potential role in a portfolio. A central tenet of our portfolio construction approach is that we believe every asset “should have a purpose.” Some are fairly obvious – cash for transactions and “dry powder,” fixed income as a diversifier, liquidity manager, and deflation hedge, and so forth as shown in Exhibit 4. So, what role can crypto potentially play? We will spend most of the remainder of this report addressing that question.

CRYPTO IS A WILD (PRICE) RIDE

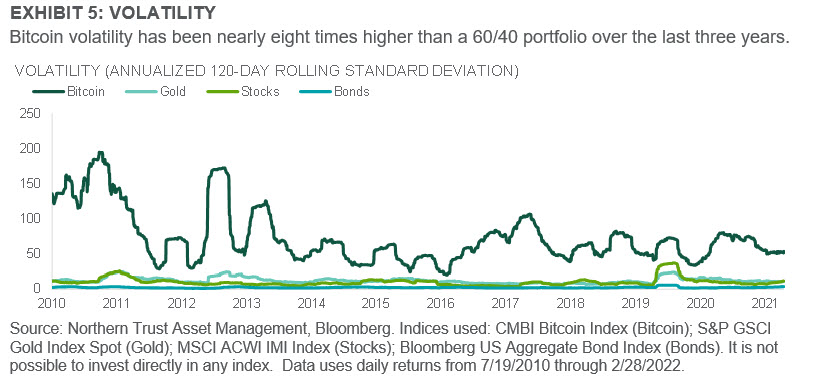

Bitcoin volatility has been quite elevated so far, with volatility nearly eight times that of a standard 60% equities/40% fixed income portfolio. Its overall risk levels have fallen considerably when comparing the last three years to the last ten, but it doesn’t seem to have improved meaningfully over the last five years. As of the end of February 2022, Bitcoin had a 54% standard deviation to the 60/40’s 7%.

CRYPTO DRAWDOWNS HAVE BEEN SEVERE

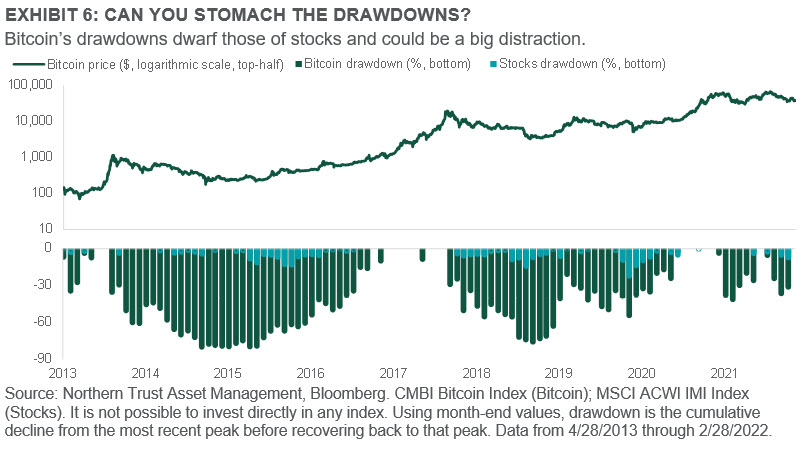

Another way to look at the volatility issue relates to drawdown experience – how much an asset declines from its most recent peak. Qualitatively, these large drawdowns would likely present problems for investment committees – especially when you don’t have fundamental valuation/cash flow/dividend metrics to try to assess further downside risk. Just how much of an investment committee meeting do you want to focus on one asset? In the graphic below, recent experience is somewhat understated due to the methodology of using month-end prices. In fact, Bitcoin experienced a 48% drawdown from its November 9, 2021 high of $67,734 to a January 22, 2022 low of $35,402.

CRYPTO IS INCREASINGLY TRADING LIKE A RISK ASSET

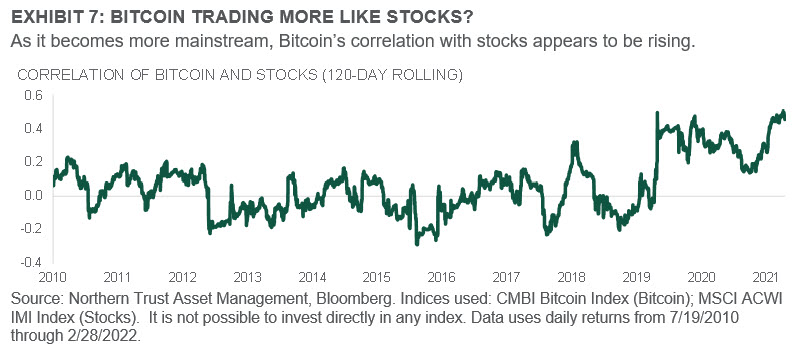

As mentioned earlier, one reason to add an asset to a portfolio is to increase diversification by focusing on uncorrelated assets. While recent history can change, Bitcoin’s positive correlation to equities has been on the rise in recent years – hurting the case for diversification and portfolio inclusion. For perspective, the correlation between stocks and investment grade fixed income – generally viewed as the ultimate diversifier for multi-asset portfolios – currently sits at -0.1 over the last 120 days and has rarely gone above 0.5. Bitcoin’s correlation to stocks is attempting to push through that level.

IF CRYPTO IS THE NEW GOLD, IT DOESN’T ACT LIKE THE OLD GOLD

Gold is probably the best known “alternative asset” for those looking for a store of value in times of uncertainty. Bitcoin is increasingly promoted as the new “digital gold” – and for a share of the investment class that is undoubtedly true. One of the most common valuation approaches for Bitcoin is to make an assumption about it reaching something like parity with gold – leading to projections of Bitcoin reaching a six-digit price level. We understand the conceptual appeal of Bitcoin as a safe haven asset in certain circumstances. Citizens in countries whose currencies have massively depreciated, or whose wealth is at risk of being confiscated certainly find cryptocurrencies an attractive alternative. But for an investor, does Bitcoin provide the safe haven attributes of gold – such as protection during periods of market stress or high inflation?

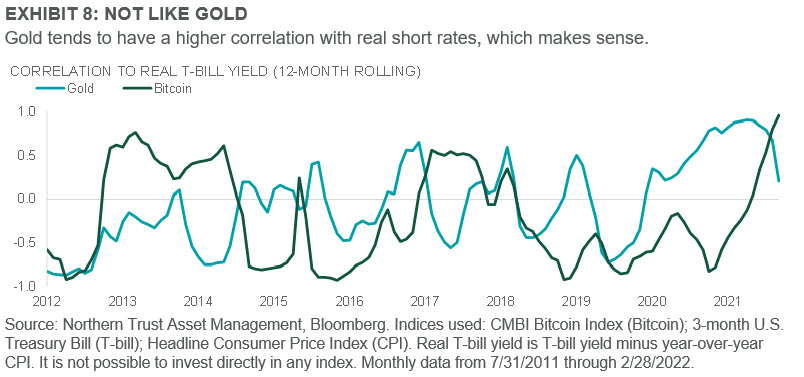

Over the last ten years, the correlation of Bitcoin to gold has ranged from negative 0.2 in 2016 to a high of 0.3 in 2020, before falling to around 0.1 currently. So, within this period, Bitcoin and gold certainly don’t trade similarly. We have never included gold in our strategic asset allocation due to its lack of utility and unclear long-term return potential. One factor that we believe is helpful in divining what gold prices may do is the path of short-term real interest rates. When short-term real rates are falling, it is usually because interest rates are falling (signs of trouble, risk aversion) and also potentially inflation is rising. The Fed’s quantitative easing (QE) from 2008-2012 was the one time we have included gold in our tactical asset allocation policy as it wasn’t clear when this period of monetary policy profligacy was going to end. When investors started to forecast the end of QE, we exited our gold positions.

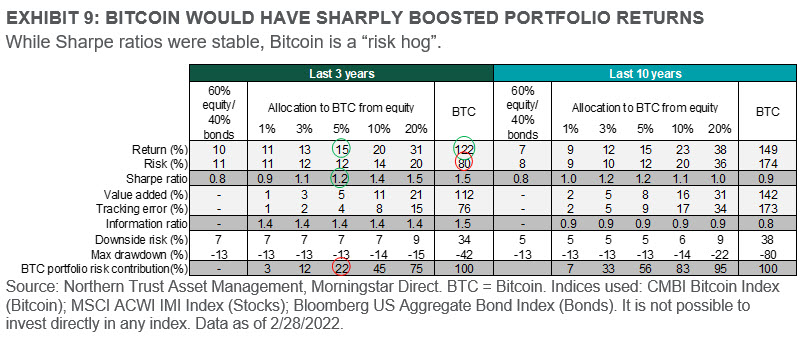

PAST PERFORMANCE IS NO GUARANTEE…

The historical data in Exhibit 9 shows that Bitcoin would have meaningfully improved portfolio returns, and even improved the risk-adjusted metrics (Sharpe ratio). However, there are several caveats (beyond past performance is no guarantee of future results). First, as discussed previously, Bitcoin has been highly volatile. Annual risk of 80% over the last three years and 174% over the last 10 years means that a Bitcoin allocation would have taken up a large proportion of a portfolio “risk budget.” A 5% allocation would have represented 22% of portfolio risk on a three-year basis and 56% of portfolio risk over the last 10 years. Second, the improvement in risk-adjusted returns is highly dependent on the great returns offsetting the high risk. Of course, they could both come down proportionally – which is certainly possible – and the improvement to risk-adjusted returns would persist.

CONCLUSION: THINK BEYOND CRYPTOCURRENCIES

The maturation and adoption of blockchain technology promises to be a meaningful investment and economic event over the coming years – as is reflected in the significant time and talent dedicated to developing technologies in this area. How does one capitalize on this mega-trend? One direct way is through venture capital where investments can be spread across different applications, technologies and founders to increase the odds of success. For public market investors, the opportunities are more limited, primarily contained within the cryptocurrency space. Using our “every asset should have a purpose” framework, we conclude that the primary role of cryptocurrencies would be for potential long-term appreciation. However, due to the risk factors mentioned earlier, we still would categorize the appreciation potential as speculative. We do believe cryptocurrencies will be an important component of the adoption of blockchain and Web 3.0 advances – but at present we find the risk too high to justify a meaningful position in an investor’s portfolios.

Special thanks to Christian Lambert, Rotational Development Associate, and Cynthia Arana, Rotational Development Associate, for their contributions to this report.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A.

IMPORTANT INFORMATION. For Asia-Pacific markets, this information is directed to institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. Northern Trust and its affiliates may have positions in and may effect transactions in the markets, contracts and related investments different than described in this information. This information is obtained from sources believed to be reliable, and its accuracy and completeness are not guaranteed. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor. Opinions and forecasts discussed are those of the author, do not necessarily reflect the views of Northern Trust and are subject to change without notice.

This report is provided for informational purposes only and is not intended to be, and should not be construed as, an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Recipients should not rely upon this information as a substitute for obtaining specific legal or tax advice from their own professional legal or tax advisors. Information is subject to change based on market or other conditions.

Past performance is no guarantee of future results. Performance returns and the principal value of an investment will fluctuate. Performance returns contained herein are subject to revision by Northern Trust. Comparative indices shown are provided as an indication of the performance of a particular segment of the capital markets and/or alternative strategies in general. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index. Gross performance returns contained herein include reinvestment of dividends and other earnings, transaction costs, and all fees and expenses other than investment management fees, unless indicated otherwise.

Northern Trust Asset Management is composed of Northern Trust Investments, Inc. Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K, NT Global Advisors Inc., 50 South Capital Advisors, LLC, Belvedere Advisors LLC and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company.

Weekly Investment Commentary: Munis offer yield relief from inflation’s heat

U.S. yields began the year at their highest starting level since 2011, and they have since risen further across the Treasury and municipal curves.

Global Weekly Commentary: Higher bar for U.S. earnings to deliver

We saw 2024 as a year of two stories. First, cooling inflation and solid corporate earnings would support upbeat risk appetite.

Global Markets Weekly Update: April 19, 2024

Review the performance of global stock and bond markets over the past week, along with relevant insights from T. Rowe Price economists and investment professionals.