THE GREAT STAY-IN

THE GREAT STAY-IN: IMPACTS OF COVID-19 ON PRIVATE CAPITAL MARKETS

A weekly retrospective

Week of 9 April 2020

The Great Stay-In (Fifth of a Series)

“As goes COVID-19, so goes the nation.”

Paraphrasing the famous 1950s dictum on General Motors’ relationship to the welfare of America highlights how the coronavirus has hijacked all aspects of the economy.

There’s consensus that once the disease runs its course, commercial activity will come back. It’s also agreed that between now and then GDP will be negative, perhaps alarmingly so. What’s not clear is how sharp or long the downturn will be. Or whether the recovery will be weak, temporary, or pick up where February left off.

For guidance we turned to Brian Nick, Nuveen’s chief investment strategist. Brian is a frequent commentator on top media outlets. He kindly offered to help our readers understand better the current economic and markets dynamics:

TLL: Brian, thank you for taking the time. First, let’s talk about job losses. You’ve said these feel like the tip of iceberg. How bad will it get before we’re done?

Brian Nick: This will be the worst labor shock since the Depression. The numbers are startling because it’s all happening at once. Ten million Americans have already filed for unemployment; I won’t be surprised to see ten million more in coming weeks.

An effective economic policy gets money to businesses to help keep workers (or bring them back) on their payrolls. If we see more million-claim weeks, the slower the bounce back will be. Keeping workers attached to jobs is key. Europe is attempting a more direct method of payroll subsidy that I expect will work better.

TLL: Various shapes – V, U, L – have been proposed for the kind of recovery we will have. Do you have a favorite letter?

BN: I like to say “Q” just to watch people try to sort that out. I think it’ll likely look like the Nike swoosh logo. It took until Q2 2011 for GDP to recover to the level it had peaked at in Q4 2007. I don’t think it will take that long this time around. More likely we’ll see a multi-staged recovery with certain sectors reopening while others remain closed. We can’t expect the lights to come back on as quickly as they’ve gone out.

TLL: Recognizing your advanced degree is in economics, not medicine, when do you think the virus part of the crisis will be over?

BN: I think we’ll see positive GDP growth in Europe and the U.S. in 3Q, assuming social distancing policies puts the economy in an induced coma while it fights off the virus. There are early signs we’re turning a corner in some of the hardest hit European countries. If true, by June the health care battle may feel like it’s largely won.

But if I’m still sitting home in August typing e-mails with nowhere to go, my economic assumptions today will prove too optimistic. But they don’t feel that optimistic now.

➢ Next week: We continue our conversation with Brian Nick on the economy.

###

Week of 30 March 2020

The Great Stay-In (Fourth of a Series)

“We did not underwrite for this.”

So said the managing partner of a top-tier middle market private equity firm. In a conversation last week, he spoke of the challenges and uncertainties surrounding the impact to businesses of COVID-19.

“We always model downside scenarios for any investment we consider,” he said. “But the zero revenue case wasn’t one of them. This is such a dramatic shift from anything anyone has ever encountered. We’re working 24/7 to figure it out.”

How are direct lenders helping their private equity clients navigate these uncharted waters? In recent updates with our peers, some common themes emerge.

The focus on new deals has pivoted sharply to existing credits. Lenders have quickened the pace of portfolio reviews. Same with sponsor dialogue about their strategies to battle the myriad COVID headwinds.

Liquidity is the number one shared concern among credit providers. Overall it appears anywhere from half to three-quarters of middle market issuers have drawn down on their revolving credits. That mirrors the RC drawdowns for the broadly syndicated market. Per S&P LCD, half of those issuers are investment grade.

Included in these concerns are delayed draw term loans. Used typically for add-on acquisitions and significant capex programs, lenders worry that sponsors will be tempted to use DDTLs to buttress their companies’ general liquidity. Are lenders seeing a rush of amendments? What about payment defaults?

“It’s early days,” one credit veteran told us. “Most companies have enough cash for 1Q interest payments, but June 30 is a long way off. It’s going to be ugly given the virus impact across multiple industries. Anything touching the consumer is affected.”

“We are working very closely with our sponsors,” another top lender reported. “The majority are being cooperative about being part of a solution. But visibility on their businesses is near zero. They don’t know how much capital they’ll need because they don’t know how bad it’s going to get. The outlook changes every day.”

The head of one leading direct lender said the game of big purchase price and leverage multiples is over. “Everyone’s trying to figure out structures that will work, given all the uncertainty. For strong credits, there’s still long-term faith in the business model. It’s the next month or two that everyone’s worried about.”

A credit op manager agreed. “By the fourth quarter, some normality will return to the financing markets. But until then, it’s ‘Battle stations!’”

➢ Next week: The economic outlook for 2020.

###

Week of 23 March 2020

The Great Stay-In (Third of a Series)

“The three main U.S. stock indices closed at record highs as concerns over the coronavirus outbreak’s economic impact seemed to fade.” – Barron’s, February 12, 2020.

Perhaps not the “Dewey Beats Truman” of media misreads, but this quote reflected widely shared sentiments among market participants. “Can anything stop this rally?” the columnist went on to ask rhetorically.

Barely six weeks ago, the Dow stood at 29,551. Today it’s 10,000 points lower, the economy at a standstill, global markets in shambles, Americans locked at home.

This, then, is the picture private equity sponsors are facing. As value investors by nature, these firms know at some point properties will present themselves at significantly lower prices. But how can you analyze a new investment when revenues and cash flows are uncertain, and in some cases, non-existent?

So for new deals, buyers and sellers faced with extreme lack of clarity on valuations are on hold. As Jamie Dimon famously put it, selling a house is not the same as selling a house on fire. In the meantime, PE shops are looking closer to home.

A survey of top sponsors reveals a number of common elements. First, since the coronavirus began to emerge earlier in the year, firms have been working hard to analyze how it will affect both portfolio companies and add-on transactions. This exercise mirrors work done last year amid China trade/tariff concerns.

At the same time, PE is in frequent dialogue with lenders to ensure relationship credit providers are “still there.” It’s early days, but as assessments of borrowers’ financial health continue, conversations will morph to specific requests for remedies to bridge issuers over the challenging quarters ahead.

In that regard, the often-heard watchword is “liquidity.” With circumstances changing daily, if not hourly, private equity owners aren’t looking too far ahead. In most cases the long-term value proposition of these properties remains sound. But does the company have enough cash to get through the next couple weeks?

Given the sweeping outages of employee attendance, few industries are being spared. Sponsors are triaging portfolio names, focusing on businesses requiring immediate financial support to make payroll. The others can wait until tomorrow.

Are screaming bargains to be had? Perhaps, but who’s willing to step into a falling elevator? We suspect once some stability returns, big investors will start making big bets on brand names (cf. Warren Buffett, Goldman in 2008). New business will then open up for the rest of us. It’s just a question of timing. Whenever that is.

➢ Next week: How are direct lenders supporting their private equity clients?

###

Week of 16 March 2020

The Great Stay-In (Second of a Series)

This week we’ve been doing bedchecks on our lender friends in the credit markets. We caught up with one long-time practitioner, hanging out in the home office with family (as he put it) in “bathrobes and bunny slippers.” But clearly plugged in.

“The capital markets went from price perfection to price combustion,” he told us. “Last month deals were sailing through. Today it’s a whole new ballgame. There’s a lot going on behind the scenes, and nothing going on in the market.”

A leading CLO manager had a similar assessment. “There’s a massive bid/ask spread with liquid names, but trading is going on. It’s not a lock-down yet. That’s been important for managers cleaning up positions in travel and airlines.”

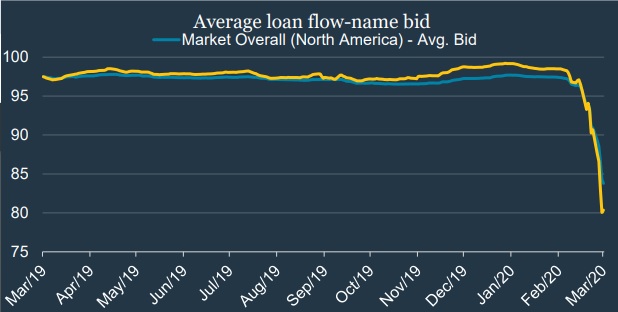

What impact, we wondered, does the cratering of secondary prices (Chart of the Week) have on primary issuance? The S&P/LSTA Leveraged Loan Index has tumbled in the last few days to a low 80’s context, down from 95 earlier in the month.

Another credit pro from a NY shop gave us some insights. “This is the first time since the depth of the Great Recession that none of the index names were priced at par. We’re nowhere near where we were post-Lehman, when the index bottomed at 67. But it’s early days. We still don’t know what the rating agencies will do.”

Unlike the early versions of CLOs, today’s models aren’t mark-to-market. “That’s true,” he said. “But warehouses are. Banks can govern the quality of assets in a warehouse by requiring margin calls. Remember the old BWICs? They were often warehouse portfolios being unwound. We could start seeing those again.”

Leveraged loan returns have taken a big hit this month, down 15%. What does this mean for loan investors?

“Loan managers don’t buy and sell the index,” our NY-based friend told us. “It’s comprised of over a thousand names. Portfolio managers focus on the more liquid issuers. It’s too early to distinguish active performance from the benchmark.”

You mentioned ratings. How will the agencies measure the impact of COVID-19? “Ah, that’s the real question,” he replied. “All this is unfolding real-time. So much of the US is shut down. The consumer, which has saved us in the past, is stuck at home. That’s not going to just hit travel and leisure. All kinds of spending is on hold.

“And it’s not just triple-C downgrades,” he went on. “It starts with negative credit watches. CLOs aren’t mark-to-market, but if triple-C baskets fill up, it hurts vehicles’ over-collateralization (OC) tests. That will compel asset managers to either put in more equity, or sell loans. In that event, the larger, more well-capitalized firms are better positioned.”

Chart of the week(1)

➢ Next week: We look at private equity activity. Are deals getting done?

###

Week of 9 March 2020

The Great Stay-In (First of a Series)

In our January 8th 2020 commentary, “Of Bubbles and Gum”, we reviewed credit market conditions in the wake of the assassination of Iranian General Suleimani. Could this be the exogenous factor that sparks a Middle East war, and triggers a recession? Or will it fade quickly like so many other candidates?

We concluded with the following observation: “Whether the Fed can continue mainlining enough liquidity all year to overcome any exogenous risks – bubbles or stickier stuff – remains to be seen.”

Little did we know, and as happens with these things, no one predicted, that the risk had already surfaced four weeks earlier. Not from mortgages, oil, high-tech, or leveraged loans, but a lethal virus originating in a seafood market in Wuhan, China.

Today that virus has upended global markets and captured worldwide attention in a way that nothing ever has. Did anyone notice North Korea’s three missile launches?

We have seen other dips that didn’t end up in a recession – 2011 when the US was downgraded and Congress squabbled about the debt limit. And 2018’s worries about China trade and tariffs. But this is different. As Bill Callahan, an investment strategist from Schroeders put it, “It affects the way people go about their lives.”

What’s driving the power of this threat is uncertainty. Beyond the obvious issues of personal health, how will rolling production stoppages, inventory shortages, worker absenteeism, consumer home bound-ism affect corporate earnings? How long will the effects last? And once the virus runs its course, will life return to normal?

It’s clear things in the U.S. will get worse before they get better. The first COVID-19 cases have just started to appear on the East Coast. Workplace and school closings are happening. One loan veteran has christened this The Great Stay-In.

The question for our readers is, what does this all mean for private credit, for private equity, for M&A, and for the capital markets overall? As a lawyer friend said to us the other day, if you can’t shake hands, how can you do deals?

Variables to examine are legion, the interrelationships complex. Interest rates are at astonishingly low levels, which hurts yields, but helps borrowers. Volatility challenges valuations, yet makes prices affordable. Throw oil into the mix – lowering operating costs and pummeling energy companies – and it’s a puzzle inside an enigma.

Armies of analysts are working to crack the code. We’ve reviewed a host of these studies examining the potential outlook for the economy, the markets, and the deal environment. Over the next several weeks we’ll try to sort through it all and make some sense of the situation for our fifty thousand Lead Left subscribers.

A word on risk Investments in middle market loans and junior capital are subject to certain risks. Please consider all risks carefully prior to investing in any particular strategy. These investments are subject to credit risk and potentially limited liquidity, as well as interest rate risk, currency risk, prepayment and extension risk, inflation risk, and risk of capital loss. This information does not constitute investment research as defined under MiFID. In Europe this document is issued by the offices and branches of Nuveen Real Estate Management Limited (reg. no. 2137726) or Nuveen UK Limited (reg. no. 08921833); (incorporated and registered in England and Wales with registered office at 201 Bishopsgate, London EC2M 3BN), both of which entities are authorized and regulated by the Financial Conduct Authority to provide investment products and services. Please note that branches of Nuveen Real Estate Management Limited or Nuveen UK Limited are subject to limited regulatory supervision by the responsible financial regulator in the country of the branch. The Lead Left is produced by Churchill Asset Management’s Head of Origination and Capital Markets, Randy Schwimmer. The Lead Left reviews deals and trends in the capital markets. Churchill Asset Management is a registered investment advisor and an affiliate of Nuveen, LLC. Nuveen provides investment advisory services through its investment specialists.

Weekly Investment Commentary: Munis offer yield relief from inflation’s heat

U.S. yields began the year at their highest starting level since 2011, and they have since risen further across the Treasury and municipal curves.

Global Weekly Commentary: Higher bar for U.S. earnings to deliver

We saw 2024 as a year of two stories. First, cooling inflation and solid corporate earnings would support upbeat risk appetite.

Global Markets Weekly Update: April 19, 2024

Review the performance of global stock and bond markets over the past week, along with relevant insights from T. Rowe Price economists and investment professionals.