Global Equities and Bond Yields Rise, Economic Indicators May Show Damage from Ukraine Conflict

Last Week Review

Investor sentiment struck a positive tone last week with global equities rallying 5.8% and credit spreads tightening. U.S. equities led the charge (+6.3%), followed by developed ex-U.S. equities (+5.1%) and emerging market equities (+3.4%). China’s equity volatility contributed to a 5.1% drop in emerging market equities through last Tuesday before bouncing back. The Federal Reserve’s first interest rate hike since 2018 and heightened inflation risks resulted in the two-year Treasury yield rising 0.19% to 1.94% and the 10-year yield increasing 0.16% to 2.15%. The 10-year German Bund yield also rose, up 0.12% to 0.37%.

Russia-Ukraine Conflict Eludes Peaceful Resolution

NATO spillover risk was elevated early last week following Russian missile attacks near Poland’s border, however that risk subsided as the week advanced. Comments from Ukrainian and Russian officials suggested progress on a peace agreement. However, those comments were later contradicted by statements from leaders on both sides as well as continued attacks around major population centers in Ukraine. While hints of optimism on a peace agreement contributed to somewhat more positive risk sentiment, most investors do not expect a near-term peaceful resolution. As the war prolongs, the odds of a decisive victory by either side are shrinking. For now, the situation remains fluid with elevated uncertainty.

Federal Reserve Initiates Liftoff

The Federal Reserve delivered its first rate hike since 2018, of 0.25%. The dot plot of Fed members’ projections of the policy rate was slightly more hawkish than expected. The median projection for the 2022 Fed funds rate was revised up to 1.9% from 0.9% and the 2023 projection was revised up to 2.8% from 1.6%. Economic growth forecasts were revised lower and inflation forecasts revised up, but in the post-meeting press conference Chairman Jerome Powell struck a positive tone on future economic growth. Initially, Treasury yields rose and equities declined, but later in the day Treasuries pared some of the losses and equities turned positive. The Bank of England also raised its policy rate 0.25%. That said, the central bank communicated a cautious approach to future policy given Russia-Ukraine uncertainty.

Volatility Hits China’s Equity Markets

A COVID-19 outbreak led to lockdowns across major China cities per the nation’s zero-COVID policy. Political risk also weighed on investing sentiment after Russia asked China for military supplies. China denied it, but news of the move nonetheless put the spotlight on China’s key role in the conflict. When U.S. President Joe Biden and Chinese President Xi Jinping met toward the end of last week, Biden warned of consequences if China supports Russia’s invasion. Further, the potential for U.S. de-listings of China stocks also weighed on China equities. After steep declines, equity markets bounced back when China authorities pledged capital market support.

This Week Preview

Biden to Attend NATO Summit

We think Russia has shown few signs of slowing its invasion and is likely to escalate conflict until it can claim some sort of win. Despite last week’s somewhat positive signals on a diplomatic resolution, Russian President Vladimir Putin has not shown a willingness to compromise. On Thursday, Biden will attend a NATO summit to discuss what more can be done to slow Russia’s advance. Investors may continue to evaluate the evolving situation, including the military conflict and sanctions response.

Economic Data Sheds Light on Global Economic Activity

The direct and indirect impacts of the war in Ukraine have been negative for global economic growth outlook. The U.S. appears less exposed than Europe and emerging markets. This week’s flash Purchasing Managers’ Index data will offer a look into the extent of the economic damage. Manufacturing and services for the U.S. and Europe are expected to retreat from prior levels, but remain at solid levels overall.

Central Bank Leaders To Speak

Several major central bank leaders will speak throughout this week, including Powell, European Central Bank President Christine Lagarde and Bank of England Governor Andrew Bailey. Russia-Ukraine impacts have made it more difficult for central banks to keep a lid on inflation without materially slowing down economic growth. Investors will look for insight into how central banks are planning to use monetary policy to thread this needle.

See our latest insights and research.

IMPORTANT INFORMATION. For Asia-Pacific markets, this information is directed to institutional, professional and wholesale clients or investors only and should not be relied upon by retail clients or investors. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. Northern Trust and its affiliates may have positions in and may effect transactions in the markets, contracts and related investments different than described in this information. This information is obtained from sources believed to be reliable, and its accuracy and completeness are not guaranteed. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor. Opinions and forecasts discussed are those of the author, do not necessarily reflect the views of Northern Trust and are subject to change without notice.

This report is provided for informational purposes only and is not intended to be, and should not be construed as, an offer, solicitation or recommendation with respect to any transaction and should not be treated as legal advice, investment advice or tax advice. Recipients should not rely upon this information as a substitute for obtaining specific legal or tax advice from their own professional legal or tax advisors. Information is subject to change based on market or other conditions.

Forward-looking statements and assumptions are Northern Trust’s current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information.

Past performance is no guarantee of future results. Performance returns and the principal value of an investment will fluctuate. Performance returns contained herein are subject to revision by Northern Trust. Comparative indices shown are provided as an indication of the performance of a particular segment of the capital markets and/or alternative strategies in general. Index performance returns do not reflect any management fees, transaction costs or expenses. It is not possible to invest directly in any index. Gross performance returns contained herein include reinvestment of dividends and other earnings, transaction costs, and all fees and expenses other than investment management fees, unless indicated otherwise. Investment management/advisory fees are described in Northern Trust Investments, Inc. Form ADV Part 2A.

Northern Trust Asset Management is composed of Northern Trust Investments, Inc. Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K., NT Global Advisors Inc., 50 South Capital Advisors, LLC, Belvedere Advisors LLC and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company.

© 2022 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A.

P-032122–2089689–052022

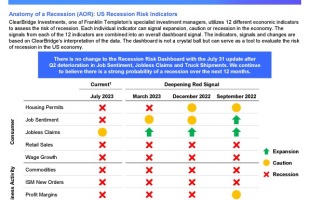

Anatomy of a Recession Update: Cracks in the Foundation

Get perspective on the most recent US economic data, the investor’s view, and how reviewing previous recessionary periods may help us today, in this conversation with Jeff Schulze, Head of Economic and Market Research at ClearBridge Investments.

AOR Update: When to expect a recession?

ClearBridge Investments: Despite improving economic sentiment now leaning the consensus view toward a soft landing, we continue to believe a recession is on the horizon.

Anatomy of a Recession: Economic and Market Outlook 3Q 2023 | August 1st

ClearBridge Investments, one of Franklin Templeton’s specialist investment managers, utilizes 12 different economic indicators to assess the risk of recession.