Global Convictions: Latest Asset Class Research

Key takeaways

- The goal of assigning a conviction level to an asset class is to distill the attractiveness of an investment opportunity into a single rank. The term “conviction” derives from the Latin verb “convincere,” which means to argue.

- In assigning an asset class conviction, an analyst trades off the aspects of an investment opportunity that argue for and against it, culminating in the expression of a conviction level. The conviction level is expressed on a five- point scale (Low, Low to Medium, Medium, Medium to High, and High), and serves as a key input into our asset allocation process.

- Our conviction scoring system is based on four criteria: absolute valuation; relative valuation; contrarian indicators; and fundamental risk.

For General Educational Use Only.

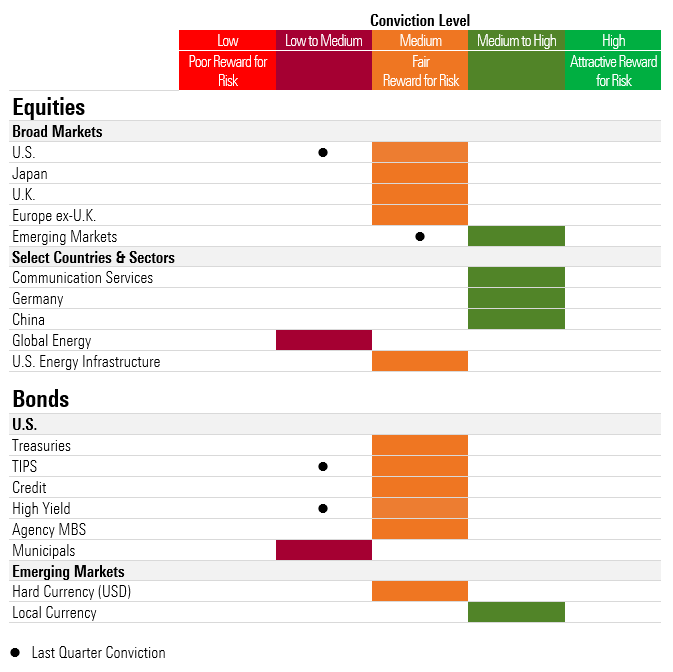

You can download the full version of this document in PDF, or read below for our asset class convictions.

Recent Developments

As we get closer to the end of 2022, it’s clearly become a year that’s tested even the most hardened of investors. Exuberance has given way to pessimism, driven by weakening corporate profits, concerns about slowing consumer demand, liquidity tightening, and a potential recession as central banks redouble their commitment to bring inflation down.

With a contrarian mindset, this has seen our convictions move positively, especially in selected fixed-income assets, although we remain broadly balanced in our long-term views. Notably, among several conviction upgrades, we reviewed our conviction on U.S. equities, which has been upgraded to Medium.

[1] Source: Morningstar Investment Management LLC. Views as of October 15th, 2022 and subject to change. For illustrative purposes only.

Overall Market Context

The market troubles are heavily influenced by inflation—which has remained stubbornly high—with core inflation becoming a contributing driver (earlier, it was energy prices that drove inflation). The ongoing war in Ukraine has also continued to wreak havoc on global supply chains and energy supplies. In addition, corporate vulnerabilities are starting to show, with warnings from high-profile global companies, such as FedEx, spooking investors.

Indeed, we are swimming in a sea of red, offsetting some of the prior gains that investors had enjoyed. The experience of 2022 so far also shows that sometimes market rules of thumb—such as bonds moving in the opposite direction of stocks—are a sign that a broader definition of diversification may be needed.

Among equities, there have been few places to hide. Whether we’re talking about value versus growth, or large versus small companies, there are very few winners. Even the defensive sectors have sold off, including healthcare and consumer staples. One key issue is that the market is anticipating a decline in corporate earnings on the horizon—the magnitude and duration of which are hard to know in advance.

Turning to fixed income, both government and corporate bonds have felt the pain, with broad-based losses across the risk spectrum. The most aggressive moves continue to come from long-duration bonds, which carry a higher sensitivity to interest rate changes. The silver lining is that the yields on most fixed-income assets are much higher.

With so few places to hide, it’s understandable that investors are feeling very nervous. However, for those still investing, the outlook is improving as lower prices could potentially imply higher returns. Valuations, on almost every measure, continue to improve. In such environments, it’s helpful to think about investing as a little like farming, there are times when we are harvesting previous gains and times when we are sowing the seeds for future return potential. As prices fall, it can be prudent to move into sowing season.

Finally, for valuation-driven investors (who aim to buy assets at discounts to what they’re worth), periods like this may result in good opportunities. The uncertainty that dominates the headlines today can lead investors to cut and run, leaving potential upside for those willing to invest and stay the course for the long run.

U.S. Equities Outlook - Medium Conviction

U.S. stocks have had a difficult year, with the froth in the market coming off. In particular, we have observed an unwinding in the more speculative pockets of the equity market, with one of these categories the “innovative” companies that often grab the financial headlines and garner attention from investors looking to own the next big winner.

This started with a contraction in valuations—with the Price/Earnings ratio coming back toward normal levels—but markets have since turned their focus toward the trajectory of future earnings. In this regard, corporate profits appear high versus historical levels and potentially vulnerable, especially in an environment consisting of persistent inflation and moderating economic growth. This is a regime in which it could become more difficult to pass on cost increases through pricing, with aggregate earnings potentially falling from record highs at a point where the economy is at risk from recessionary pressures. That said, we note that financial conditions, by many observations, remain fairly robust.

It’s important to note that upon review of our conviction for the US equity market as a whole, we landed with a Medium overall conviction – the first time this has been the case in quite a while. The scores across two key “pillars” – absolute valuation and relative valuation—improved moderately, while scores for contrarian indicators and fundamental risk remained unchanged. The weak stock market backdrop, as characterized above, certainly played a role in improving the outlook in this market. This is not to say that we consider U.S. equities to be an outright bargain—we don’t. But our process tells us that the situation has moderately improved, which is reflected in our conviction upgrade.

At a deeper level, valuation spreads—the disparity in valuation levels between sectors—has narrowed. More pointedly, in this environment we see fewer opportunities to be granular. In 2020-21, we identified opportunities clustered in more cyclical (or economically sensitive) areas of the market. Specifically, regarding energy stocks: our valuation approach incorporates a reversion framework for energy prices longer-term, which leads us to conclude that energy producers in particular have become fairly valued, but we acknowledge that a prolonged period of structurally higher commodity prices is not priced into these shares and also that companies have shown fairly strong capital discipline even as pricing has firmed, which is a significant, positive departure from previous cycles. Energy infrastructure shares remain relatively appealing to us within the energy sector. On financials, our research leads us to believe that large U.S. banks are still relatively attractive. The last area on our radar is defensive sectors, most notably healthcare, which have improved in our relative rankings and could help offset equity risk as it is not highly correlated with economic cycles. Regarding technology stocks, we don’t assess these stocks with a broad brush, though our own sentiment index would suggest the extreme popularity has subsided. That said, the sector in aggregate has been “over-earning” relative to its own history (meaning, profit margins of late have been elevated versus long-term averages) for good reason in some ways. Moreover, valuation challenges persist beyond the recent declines, so care is required in this space, especially with interest-rate rises and valuation multiple implications from those increases.

All this is to say—a long-term perspective remains a critical ingredient for investors. This is perhaps even more relevant during periods of market turbulence.

Europe ex.-U.K. Equities- Medium Conviction

European stocks are challenged, with supply-side issues evident and a difficult inflation backdrop stemming from the Ukraine/Russian war. The euro has also deteriorated meaningfully against the U.S. dollar, coming back to parity, which hurts importers but improves the attractiveness of exporters.

While we generally like European stocks, we find attractive opportunities when we dig into country and sector differentials. For example, we’ve reaffirmed our attraction to German stocks which remain an appealing area despite the impact of the Russian conflict. In aggregate, we find German stocks offer solid balance sheets and potential upside to earnings—without eye-popping valuations. At a sector level, our positive view on European integrated-energy companies has moderated following recent strength, as it no longer offers the same valuation appeal. European banks, on the other hand, look more attractive on our analysis.

U.K. Equities - Medium Conviction

The United Kingdom has a relatively large exposure to energy and financial stocks,especially in the large cap space, which has supported the market in recent times.

This comes despite the general consensus that the U.K. economy is vulnerable, with political change and the associated volatility from the so-called “mini budget”. We note the composition of U.K. stocks is buffered from domestic issues, given their international business models with the majority of revenues derived offshore.

Our overall conviction score for the U.K. remains at Medium. While relative valuations remain at Medium to High, absolute valuations have fallen to a Low to Medium reflecting recent performance.

This means our long-standing belief that investors were being compensated for the risk of investing in U.K. stocks has softened, coming more in line with international peers. That said, they remain a strong dividend play, where we have seen many companies reinstate their dividends, although most are targeting more conservative payout policies going forward. While revenue is cyclical given the underlying key sectors of Financials, Energy and Materials, we believe it is stable. Both operating and financial leverage are also stable. From a fundamental standpoint, we note that certain scenarios pose a risk to corporate profitability.

Australian Equities - Medium Conviction

Australian shares have fallen over the course of 2022 but have outpaced large global markets such as the USA. High volatility from rising inflation and interest-rate expectations, recession fears and commodity prices continuing to fall from abnormal highs have also weighed on prices over the year. Investor sentiment remains on the weak side, especially for smaller, richly priced and faster growing companies which have fallen significantly year to date.

Internal political uncertainty has somewhat subsided, although economic vulnerabilities to foreign demand and the associated geopolitics remain. Corporate profits could also be sensitive to an economic setback, with profit margins near cyclical highs (especially among the miners) and aggregate earnings slipping.

Australian shares have improved in attractiveness over the year, according to our analysis. Poor performance and a revision of our fundamental assumptions have seen our conviction score for Australian Shares move up to Medium. While opportunities do exist at a more granular level—especially for those willing to invest differently to the index—we continue to see greater merit in global exposure, including Germany, China, and other select emerging markets.

It would take a further decline in prices before we see outright attraction in this asset class.

Japanese Equities - Medium Conviction

Japanese stocks have had a unique experience, often moving out of lockstep with the rest of the global equity market. They continue to offer a diversified revenue source, especially for unhedged exposure, with the Japanese yen showing incredible value (near multi-decade deviations against other developed market currencies).

We continue to see merit in Japanese equities. For the most part, our conviction in Japanese stocks is built on some major structural change taking place at a corporate level. While much of this structural tailwind is now behind us, we still see scope for a continuation of improving shareholder interests, rising dividend payouts, and board independence. Japanese stocks also carry attractive diversifying properties that may help in broad market setbacks. With this in mind, we see attraction in domestic-facing companies, most notably financials. Sentiment toward Japanese financials had been hindered by the Bank of Japan’s prolonged quantitative-easing program, making it difficult for banks to make money (and lowering investment income for insurers). While this is likely to remain a challenge, the upside is meaningful if and when the normalization takes hold.

Emerging-Markets Equities - Medium to High Conviction

The broad emerging-markets basket remains challenged by high inflation, higher funding costs, and volatile local currencies. As usual, investors in emerging markets must also price in regulatory and geopolitical risk.

We have upgraded our conviction to Medium to High. We consider emerging-markets equities to be among our preferred equity regions (alongside selected European and Japanese equities). As part of this, we need to remember that emerging markets are heterogeneous. Investors tend to bucket emerging markets as one, but often the real opportunities present themselves at a country, sector, or regional level. For example, China continues to offer better absolute and relative value, with the Chinese government providing regulatory relief for various industries and re-opening after COVID spikes hit major metropolitan areas. Fundamental risks are on the higher side, but we see a contrarian opportunity in China, especially in the technology space, which has suffered from negative sentiment.

Global Sectors

At a sector level, we’ve seen significant divergence as inflation and high commodity prices influence investors. Perhaps the most notable is the stellar run for energy companies in 2022, which have significantly outpaced other sectors, albeit from a low base. At the other end, technology is still struggling, which is perhaps not surprising given the long-duration nature and the unwinding of monetary stimulus. Defensive sectors have played an important role too, helping manage volatility and providing the characteristics that people seek in a market setback.

The opportunity to add value via sector positioning has narrowed. That said, we continue to see opportunities, especially at the defensive end.

Let’s start with energy stocks, given their extraordinary run. This sector was among our highest-ranking opportunity last year and has enjoyed a period of elevated commodity prices. However, this opportunity has narrowed.

In our view, communication services also now possesses one of the most attractive opportunities among the sectors we cover, in part a function of weak recent share price returns. Encompassing internet media companies, media and entertainment companies, and telecom services providers the sector has been impacted by rising discount rates together with macroeconomic concerns. While we do see a potentially more significant level of fundamental risk present in the sector as opposed to other asset classes, valuations (both absolute and relative) as well as contrarian elements tip the scales on our conviction in favor of Medium to High overall.

Defensive value-oriented areas of the market continue to live up to their reputation and have held up relatively well during the downdraft. Sectors include healthcare, utilities, and consumer staples, all of which provide services that are required in both good and bad times. Generally, stocks in these categories are less volatile and less affected by the ups and downs of long-term market cycles. This could be important if we see a broad-based decline in corporate earnings.

Developed-Markets Sovereign

- U.S. - Medium Conviction

- Europe - Low to Medium Conviction

- Japan - Medium Conviction

Locally and globally, government bonds remain volatile. We note the large uptick in yields for short-term bonds as investors reset their interest rate expectations. In the U.S., this has caused the yield curve to “invert” once again (where investors get a higher yield for short-term bonds than longer-term bonds), which is often seen as a recessionary signal.

That said, there are some signs that longer-term government bonds are finally showing their defensive characteristics again, following a rough period. The synchronized declines were of great concern to cautious investors who typically hold a higher proportion in bonds and are used to a more stable return.

The material increase in bond yields has improved the forward-looking prospects, which applies positively to the U.S., U.K., and Australia. Europe is also rising from a very low base, although the absolute yields remain broadly unattractive. In all cases, yields fail to cover inflation, but that ought to be expected given the environment.

Going slightly deeper, the ability to add income to portfolios while mitigating duration/default risk looks attractive to us currently. Rising government bonds are a positive for future return potential, and we expect this asset class to continue playing a role for investors.

That said, overall, we feel that managing duration risk makes sense in most scenarios. We are cognizant of the rather sizeable drawdown in government bonds year-to-date and adding materially to duration might make sense at some point, but any changes should be measured and deliberate, given the fast-changing response from central banks.

In this sense, government bonds are in an odd spot. On the one hand, the global macro environment is widely uncertain with a range of outcomes. The domestic economy is challenged with slowing growth and surging inflation that has the potential to reduce aggregate demand. To complicate matters, central banks have been late to make decisions to address inflation that could ultimately lead them to a tough bridge – fight inflation aggressively or do what you can to maintain the economic recovery. Unfortunately, at this stage, these decisions seem to be mutually exclusive.

Further, given the delicate nature of both the domestic and global economy, long-term sovereign bonds seem appropriate to hedge against risks, whether that is aggressive central bank action, a weakening of demand, or both.

Investment-Grade Credit

- U.S. - Medium Conviction

- Europe - Low to Medium Conviction

We’ve seen a meaningful shift in corporate bonds. The initial uptick in yields was primarily a shift in the risk-free rate (mirroring the rise in government bond yields), but we’ve since seen credit spreads widen which is a sign of corporate vulnerabilities and recessionary nerves.

From a duration standpoint, corporate bonds have shared a similar experience to government bonds, where longer-dated bonds have underperformed in this environment. Shorter-dated bonds have held up, relatively speaking.

Both locally and globally, the higher yields have improved the attractiveness of this asset class to us, albeit from a low base. A key element is credit spreads—the difference between corporate-bond yields and government-bond yields—which have moved closer to fair value in our analysis, although not enough to be deemed attractive.

In this regard, one should be aware of the historically high percentage of BBB-rated issuers (the lowest level still considered investment-grade) in this space. This credit-quality development needs to be monitored carefully, as a heightened default cycle can’t be ruled out.

From a fundamental standpoint, the Federal Reserve’s increased involvement in this asset class had provided a backstop, although withdrawal of that support, increasing leverage ratios, and the possibility of higher yields are a cause for concern over the medium to long term.

In summary, this space has improved, but the inherent appeal remains muted. We see some attraction as a middle ground—providing some extra yield versus government bonds and a duration profile that can help in portfolio construction.

High-Yield Credit

- U.S. - Medium Conviction

- Europe - Medium Conviction

High-yield credit has offered a tempestuous ride in recent years, with yields increasing quite meaningfully. Headline yields now look very tempting, oscillating in the high single-digit range, which we haven’t seen since the COVID panic and before that in early 2016.

We note that the type of volatility experienced year-to-date isn’t unusual for high-yield bonds, which sit at the riskier end of the bond market—often moving more with equity markets than with other bonds. This was certainly the case during the height of the COVID-19 crisis, with high-yield–bond prices seesawing in line with broader equity market sentiment. Again, it is seemingly happening now with the added complication of rising rates.

Improved valuation, both on an absolute and relative basis, has caused us to upgrade our overall conviction to Medium. In our view, this bears watching—but it’s not a “fat pitch” opportunity yet. While headline default risks are still deemed to be low, this could change with central banks tightening conditions and recessionary preconditions festering. A shorter duration profile relative to other bonds is also a potential positive in a rising-rate environment.

Emerging-Markets Bonds

- Local Currency - Medium to High Conviction

- Hard Currency - Medium Conviction

Emerging-market bonds have experienced dispersion, with challenging fundamentals and currency moves a major component of weakness.

Like high yield bonds, the headline yields are rising to enticing levels, also in the high single digits. This reflects the reality that many emerging-market central banks have had to raise interest rates to combat inflation pressures and to bolster currencies.

Emerging-market debt in local currency (which we still prefer over hard currency) offers healthy absolute yields, accounting for the added risk. Our view remains that many emerging-market sovereigns, though with notable exceptions, have improved their fundamental strength compared to history. This includes improved current account balances, enhanced reserves, movement to orthodox monetary policy, and a build-out of local investor base allowing for a shift to local currency funding. In addition, the aggregation of emerging-market currencies also look undervalued overall and could offer a tailwind over time.

The area can be volatile, yet even allowing for some pessimistic assumptions, our research suggests that investors could see upside if they’re willing to risk short-term volatility. In other words, we think investors may get compensated for this risk over time, especially for local-currency bonds.

U.S Agency MBS - Medium Conviction

U.S. mortgage-backed securities (MBS) have experienced a sizeable setback year-to-date as a sharp rally in interest rates led to meaningful extension in duration. Fundamentally, the housing market is slowing as a result of higher interest rates and home prices. The MBS market is also pricing in the tightening of monetary stimulus.

Overall, considerable weakness has been experienced year-to-date while fundamentals remain solid and technicals look much more attractive to us today. Given the sharp rally in mortgage rates and significant duration extension, the attractiveness of this asset class has improved. Heading into the second half of 2022, investors will be keen on watching inflation and the result it has on overall consumer demand. The idea of slowing economic activity should support AAA assets such as Agency MBS as there is little inherent default risk. That said, further spread widening may take place before it turns in investors favor.

Global Inflation-Linked Bonds - Medium Conviction

With policy yields rising, bonds have suffered broadly, and inflation-linked bonds are no exception. We’ve seen the breakeven rate (the difference between nominal government bonds and inflation-protected bonds) fall back after a recent spike. Meanwhile, the U.S. real yield curve is now positive.

We’ve upgraded our conviction for Treasury Inflation-Protected Securities (TIPS) to Medium (from Low to Medium). Absolute and relative valuations have pushed into attractive territory, while fundamentals have improved as well.

Within that context, a key consideration is whether inflation-linked bonds can help diversify the risk drivers of other assets. Keep in mind that with inflation-linked bonds such as TIPS, the value of the principal rises (or falls) with changes in inflation expectations rather than the actual inflation rate. Inflation expectations are notoriously difficult to forecast, so this can be a key benefit.

Of course, inflationary pressures are proving quite sticky at the moment, yet it wouldn’t take much for markets to reprice inflation should something give. One important consideration is duration risk, where inflation-linked bonds are often longer-dated securities with meaningful interest-rate sensitivity.

U.S. Municipal Bonds - Medium Conviction

Municipal bonds have also experienced recent setbacks against a backdrop of rich valuations and increasing yields. High-yield municipal bonds have been among the most volatile during this environment.

Yields on high-quality municipal bonds have trended higher and look attractive on a tax-adjusted basis. Considering the uncertain economic environment, we expect volatility to persist, however given the higher quality nature of municipal securities, downside risks look manageable compared to similar quality corporate bonds.

Fundamentals of state and local governments have held up better than expected in the wake of the pandemic. That said, uncertainty around further interest rate increases and high inflation could lead to further outflows which can hinder the performance of the overall asset class.

Global Infrastructure - Low to Medium Conviction

- U.S. Energy Infra & MLPs - Medium Conviction

Infrastructure assets are a diverse basket, with airports, rail, and energy-related holdings all carrying differing performance drivers. Over the quarter, long duration assets that exhibit more sensitivity to rising interest rates were among the worst performers – this included Communications Infrastructure and Toll Roads. Of particular note, energy-related investments have staged an incredible run, and while the path ahead remains uncertain, valuations have become less attractive to us. We’ve also seen takeover activity by unlisted and/or private investors increase for listed transportation infrastructure assets, mainly in the airport and toll roads sub-sectors. This is being driven by these assets being more highly valued in the unlisted market.

While infrastructure has generally become more attractively priced, due to rising interest rate and recession concerns (the latter mainly negatively impacting railroads and airports), we continue to see better value in other areas of the equities market.

Oil prices are significantly higher, and energy infrastructure equity prices have rebounded strongly—which has served, at the margin, to mute our historically-positive view of this asset class. That said, we continue to see some appeal given the relatively high dividend yields and continued demand recovery. We also cite further governance and capital-allocation discipline. Specifically, our expectation is for a meaningful reduction in capital expenditures by energy infrastructure companies, with overall spend being reduced towards maintenance, or steady-state levels. Headwinds remain amid the push to address climate change, but the transition to renewable energy is likely to be a long path, potentially allowing for an extended period of robust free-cash-flow generation for the industry—which we anticipate will be used to strengthen balance sheets and return cash to shareholders.

Listed Property - Low to Medium

Global real estate investment trusts (GREITs) have had a unique run since the COVID crisis started, with solid gains before a more recent setback. Recent weakness has come about due to concerns on a number of fronts: rising interest rates negatively impacting upon valuations and expected debt funding costs, recessionary concerns negatively impacting rental outlooks, and rising construction costs posing potential profit margin downside for companies with property development businesses. Over the past quarter, the dual concerns of recession and rising debt funding costs particularly negatively impacted U.K. real estate, while Japan real estate assets held up better as interest rates are not expected to rise significantly in Japan.

While moves to reopen global economies have broadly progressed, we believe that earnings risks remain elevated. Investors in office REITs face a more depressed rental-growth outlook over the short term and an uncertain outlook over the medium to long term. Time will tell if the trends toward accelerating online sales and working-from-home persists. With debt funding costs and construction costs on the rise, investors need to be wary of trusts exhibiting highly leveraged balance sheets and/or large property development exposure. Following recent price falls, listed property is starting to present better value, but remains relatively unattractively valued compared to broader equities at the present time.

Alternatives

Alternatives have offered a partial ballast during the 2022 setback, though in many cases they haven’t offered the outright diversification investors were hoping for.

Of course, this depends on the strategy being adopted. Our view remains that alternative offerings should exhibit genuinely diversifying assets with reasonable costs and liquidity.

More specifically, with rising bond yields implicating both stocks and bonds in similar ways, alternative assets can appeal given that returns from this asset class tend to have a lower direct relationship with the performance of traditional asset classes such as equities and bonds.

Currency

While currencies are notoriously volatile, we tend to think of currency convictions via the lens of robustness (focusing on those currencies with defensive characteristics where sensible) but also as a potential source of upside at extremes.

Recently, the U.S. dollar has strengthened meaningfully, surpassing parity with the euro, which is a major development for currency markets. The Japanese yen has also experienced considerable weakness.

Looking ahead, we see merit in currencies outside the U.S. dollar, despite the oft-referenced safe-haven status. The yen has the potential to provide diversification qualities and potentially help preserve capital in times of extreme economic and market stress, as well as provide potential upside.

Cash

In today’s inflation environment, cash is a near-guaranteed way to lose purchasing power.

However, we balance this view, as the market vulnerabilities are worth protecting against. Specifically, our research still points to some meaningful dispersion across asset classes, which presents an opportunity for investors.

More pointedly, we see cash serving three purposes. First, cash helps reduce the sensitivity to interest-rate rises, especially relative to long-dated bonds, which is still an important risk to manage. Second, cash should help buffer from any future volatility resulting from a fall in equity markets. And third, cash provides ample liquidity to take advantage of investment opportunities as they arise.

*The Overall Conviction level and Key Long-Term Drivers reflect the opinion of Morningstar Investment Management. These opinions are as of the date written, are subject to change without notice, do not constitute investment advice, and are provided solely for informational purposes. Morningstar Investment Management shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses, or opinions, or their use. This document contains certain forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties, and other factors that may cause the actual results to differ materially and/or substantially from any future results, performance, or achievements expressed or implied by those projected in the forward-looking statements for any reason. This commentary is for general educational and informational purposes only. The information, data, analyses, and opinions presented herein are designed to provide general information about investing, to inform investors about developments in the broader financial ecosystem, and/or to help investors interpret market and regulatory shifts. This material is not an offer of our investment advisory services or an offer to buy or sell a security. Investments in securities (e.g., mutual funds, exchange-traded funds, common stocks) are subject to investment risk, including possible loss of principal, and will not always be profitable. Prices of securities may fluctuate from time to time and may even become valueless. Securities in this report are not FDIC-insured, may lose value, and are not guaranteed by a bank or other financial institution. There can be no assurance any financial strategy will be successful. Diversification and asset allocation are methods used to help manage risk; they do not ensure a profit or protect against a loss. Morningstar Investment Management LLC is a registered investment adviser and subsidiary of Morningstar, Inc. Investment research is produced and issued by Morningstar, Inc. or subsidiaries of Morningstar, Inc. including, but not limited to, Morningstar Research Services LLC, registered with and governed by the U.S. Securities and Exchange Commission. The terms “we,” “us,” and “our” throughout this document refer to Morningstar Investment Management LLC. The term “Morningstar” refers to Morningstar’s Equity Research Group. The information, data, analyses, and opinions presented herein do not constitute investment advice; are provided solely for informational purposes and therefore are not an offer to buy or sell a security; and are not warranted to be correct, complete, or accurate. The information contained herein is the proprietary property of Morningstar Investment Management and Morningstar Investment Services and may not be reproduced, in whole or in part, or used in any manner, without the prior written consent of Morningstar Investment Management. The opinions expressed herein are those of Morningstar Investment Management, are as of the date written and are subject to change without notice, do not constitute investment advice, and are provided solely for informational purposes. Morningstar Investment Management shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses, or opinions, or their use. The commentary contains certain forward-looking statements. Forward-looking statements involve known and unknown risks, uncertainties, and other factors that may cause the actual results to differ materially and/or substantially from any future results, performance, or achievements expressed or implied by those projected in the forward-looking statements for any reason. Morningstar Investment Management do not guarantee that the results of their advice, recommendations, or the objectives of your portfolio will be achieved. There is no guarantee that negative returns can or will be avoided in any of the portfolios. An investment made in a security may differ substantially from its historical performance and as a result, you may incur a loss. Past performance is not a guarantee of future results. The indexes noted are unmanaged and cannot be directly invested in. Individual index performance is provided as a reference only. Since indexes and/or composition levels may change over time, actual return and risk characteristics may be higher or lower than those presented. Although index performance data is gathered from reliable sources, Morningstar Investment Management cannot guarantee its accuracy, completeness, or reliability. The Price/Earnings Ratio or P/E Ratio is a stock's current price divided by the company's trailing 12-month earnings per share from continuous operations. The CAPE ratio is a valuation measure that uses real earnings per share (EPS) over a 10-year period to smooth out fluctuations in corporate profits that occur over different periods of a business cycle. The ratio is generally applied to broad equity indexes to assess whether the market is undervalued or overvalued. Individual index performance is provided as a reference only. Each index is unmanaged and is not available for direct investment. Since indexes and/or composition levels may change over time, actual return and risk characteristics may be higher or lower than those presented. Although Index performance data is gathered from reliable sources, Morningstar Investment Management cannot guarantee its accuracy, completeness or reliability. S&P 500: Market-capitalization-weighted Index of 500 widely held stocks. Member companies are chosen based on market size, liquidity, and industry group representation. Included are the stocks of industrial, financial, utility and transportation companies. Morningstar US Market: The index is a diversified broad market index that targets 97% market capitalization coverage of the investable universe. The index is float market capitalization weighted, reconstituted semi-annually, and rebalanced quarterly. Morningstar US Large Cap: The index measures the performance of US large-cap stocks. These stocks represent the largest 70% capitalization of the investable universe. Morningstar US Mid Cap: The index tracks the performance of US mid-cap stocks that fall between 70th and 90th percentile in market capitalization of the investable universe. In aggregate the Mid Cap Index represents 20% of the investable universe. Morningstar US Small Cap: The index tracks the performance of US small-cap stocks that fall between 90th and 97th percentile in market capitalization of the investable universe. In aggregate, the Small Cap Index represents 7% of the investable universe. MSCI ACWI ex USA: The MSCI ACWI ex USA Index captures large and mid-cap representation across 23 Developed Markets (DM) countries (excluding the US) and 26 Emerging Markets (EM) countries. MSCI EAFE: The MSCI EAFE Index is an equity index which captures large and mid-cap representation across Developed Markets countries around the world, excluding the US and Canada. MSCI EM: A free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. Bloomberg Barclays US Universal: The index measures the performance of USD-denominated, taxable bonds that are rated either investment grade or high-yield. It represents the union of the U.S. Aggregate Index, U.S. Corporate High Yield Index, Investment Grade 144A Index, Eurodollar Index, U.S. Emerging Markets Index, and the non-ERISA eligible portion of the CMBS Index. Bloomberg Barclays US Agg Bond: The index measures the performance of investment grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM passthroughs), ABS, and CMBS. It rolls up into other Barclays flagship indices, such as the multi-currency Global Aggregate Index and the U.S. Universal Index, which includes high yield and emerging markets debt. Bloomberg Barclays US Government Bond: The index measures the performance of the U.S. Treasury and U.S. Agency Indices, including Treasuries and U.S. agency debentures. It is a component of the U.S. Government/Credit Index and the U.S. Aggregate Index. Bloomberg Barclays US Corporate Bond: The index measures the performance of the investment grade, U.S. dollar-denominated, fixed-rate, taxable corporate bond market. It includes USD-denominated securities publicly issued by U.S. and non-U.S. industrial, utility, and financial issuers that meet specified maturity, liquidity, and quality requirements. Bloomberg Barclays US Corporate High Yield: The Index covers the USD-denominated, non-investment grade, fixed rate, taxable corporate bond market. Securities are classified as high-yield if the middle rating of Moody’s, Fitch, and S&P is Ba1/BB+/BB+ or below. The index excludes emerging market debt. Bloomberg Barclays Gbl Infl Linked US TIPS: The index tracks inflation-protected securities issued by the U.S. Treasury. In order to prevent the erosion of purchasing power, TIPS are indexed to the non-seasonally adjusted Consumer Price Index for All Urban Consumers. Bloomberg Barclays Municipal Managed Money: The index measures the performance of tax-exempt bond market. All bonds in the National Municipal Bond Index must be rated Aa3/AA- or higher by at least two of the following statistical ratings agencies: Moody's, S&P and Fitch. It is rules-based and market-value weighted. Citi WGBI NonUSD: The index measures the performance of government bonds issued by governments outside the U.S. JPM EMBI Plus: The JP Morgan Emerging Markets Bond Index Plus (EMBI+) tracks total returns for traded external debt instruments (external meaning foreign currency denominated fixed income) in the emerging markets. The regular EMBI Index covers U.S. dollar denominated Brady bonds, loans and Eurobon…

Weekly Investment Commentary: Earnings season: investment ideas

First-quarter earnings season has kicked off with the utilities and communication services sectors projected to deliver the strongest year-over-year EPS growth, while estimates for materials and energy are expected to decline the most.

Global Weekly Commentary: Earnings growth not just about tech

Solid U.S. economic and corporate earnings growth have supported risk appetite, driving stocks to all-time highs – even as bond yields have jumped. We think earnings will need to deliver on high expectations, especially after last week’s data showing sticky inflation spooked investors.

Global Markets Weekly Update: April 12, 2024

Review the performance of global stock and bond markets over the past week, along with relevant insights from T. Rowe Price economists and investment professionals.