The Case for Liquid Alternatives, Especially Now

While we have long advocated that alternatives should be a core allocation within any diversified investment portfolio, there are certain periods during an economic cycle in which it may be more advantageous to be hedged or have exposure to alternate sources of return than others. In this article, we will examine: 1) Why Envestnet I PMC believes that investors should own some liquid alternatives in their portfolios at all times, and 2) Why liquid alternatives make sense, especially in the current environment.

Why Liquid Alternatives

Liquid alternatives can do many things that traditional mutual funds can’t or don’t. For example, liquid alternatives can take short positions in stocks, making them less vulnerable to or even able to profit from a declining stock market. They can also go negative in bond duration, enabling them to profit from a rising interest rate environment. Additionally, liquid alts can participate in many investment strategies that have virtually no correlation to traditional investments, such as arbitrage and futures trading which makes them excellent diversifiers.

The major attraction of liquid alternatives is enhancing diversification of traditional portfolios, as evidenced during the past two major recessions and market crises – the dot-com bubble burst (2000 – 2002) and the financial crisis (2007 – 2009). During the dot-com bubble burst, the S&P 500 Index fell 44% from peak to trough (3/24/2000 – 10/9/2002) while the HFRX Global Hedge Fund Index, a proxy for liquid alternatives, gained 17% during the same period. During the financial crisis, the S&P 500 Index plunged 55% from peak to trough (10/9/2007 – 3/9/2009) while the HFRX Global Hedge Fund Index declined 23% – 3,000 basis points of relative outperformance.¹ The drop during the financial crisis is mostly due to the severe disruptions of financial markets that prevented many types of liquid alternatives from fully executing on their investment strategies. Notably, the disruptions were so significant that short-selling on bank stocks was temporarily banned in the U.S. during the Fall of 2008, an extremely rare and controversial move, making it nearly impossible for long/short and market-neutral equity liquid alternatives to fully carry out their investment strategies during this period.

It is extremely difficult to time when a recession, bear market or economic crises is going to take place and it is important to be properly diversified. Since liquid alternatives can still provide benefits to a portfolio in rising markets, they are solid stand-alone investments. Over the trailing 20-year period ended on June 30, 2018, which spans multiple full market cycles, the HFRX Global Hedge Fund Index had an annualized return of 4.3% versus 6.5% for the S&P 500 Index but with an annualized standard deviation of 5.9% versus 14.8%, resulting in a similar Sharpe ratio (the measure of risk-adjusted return) of 0.42 versus 0.37.¹ Certainly, they are underutilized by the average retail investors and may aid in providing a smoother return experience without sacrificing risk adjusted performance.

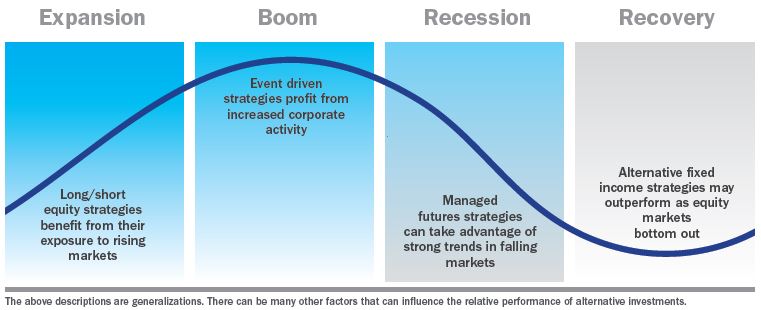

Why Liquid Alternatives – Especially Now

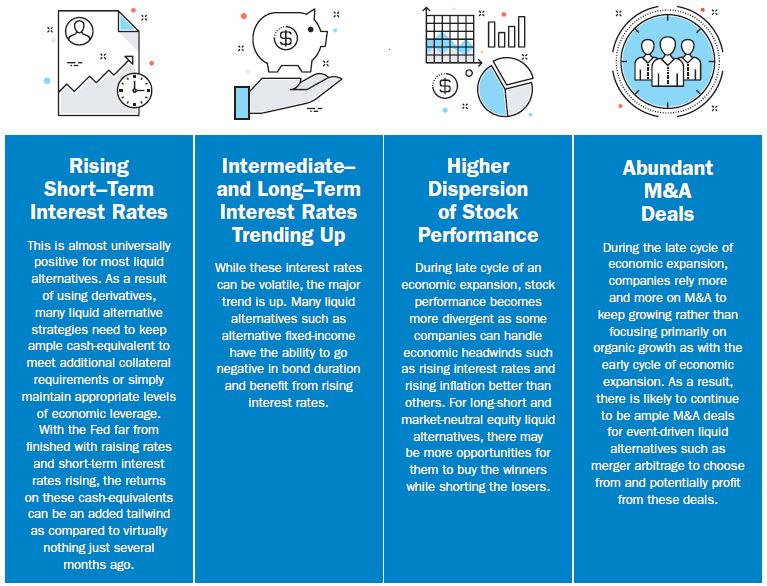

While no one knows for sure how long the current economic expansion will last and how high the stock market can go, there is little argument that we are currently in the late cycle of economic expansion. The unemployment rate is at or near its historical low, the Fed is raising short-term rates and tightening and M&A (merger & acquisition) is booming, to name a few – all hallmarks of a late-cycle period. This late-cycle market environment is very constructive for liquid alternatives and there are a number of ways in which they can benefit:

Conclusion

It is important to examine these strategies through a lens of diversification and capital preservation. Consequently, it should come as no surprise that strategies that aim to reduce downside capture will exhibit lower beta and may meaningfully underperform during market rallies. However, in order to protect capital, some tracking error in positive equity markets should be balanced out when markets reverse course.

History reinforces the importance of allocating assets to liquid alternatives at all times, but now seems like a particularly good time to invest. The additional return potential of equity markets seems limited due to the late stage of the market cycle and interest rates are on the rise, leaving many fixed-income portfolios exposed. Liquid alternative strategies may be the perfect solution, as their broadened toolkit with the ability to short and utilize leverage opportunistically could aid in protecting on the downside.

1 Source: Bloomberg

Author’s disclaimer: The opinions expressed herein reflect our judgment as of the date of writing and are subject to change at any time without notice. They are not intended to constitute legal, tax, securities, or investment advice or a recommended course of action in any given situation. Investment decisions should always be made based on the investor’s specific financial needs and objectives, goals, time horizon, and risk tolerance. Information obtained from third party resources are believed to be reliable but not guaranteed. This paper may contain ‘forward-looking’ information that is not purely historical in nature. Such information may include, among other things, projections and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this paper is at the sole discretion of the reader.

Demystifying private markets: The markets have changed, so have perspectives on allocations

We believe private markets can improve investors’ financial security and make financial plans more resilient.

The case for private markets: three things to know

Investors should consider three important benefits as they evaluate allocating to private markets.

The Case for Real Assets: Staying Ahead of Inflation

Investors’ real rate of return = Nominal rate of return – Inflation rate. Learn about how inflation can affect your clients' real assets.