The Appeal of a Dividend Strategy Amid Chaotic Markets

KEY INSIGHTS

- Investors with reasonable time horizons should consider taking advantage of opportunities created by recent market volatility despite greater uncertainty.

- With the economy in recession, some cyclical sectors such as industrials and financials offer attractive values and upside potential.

- Although more companies are cutting dividends, a dividend growth strategy remains viable, particularly for income‑oriented investors.

Uncertainty and volatility remain high as the new coronavirus has caused massive disruption to economies around the world. Tom Huber, who recently marked his 20th anniversary managing the Dividend Growth Fund, discusses the current investment environment, his investment strategy amid a growing number of dividend cuts, and some useful insights he has gained over the past two decades. The fund is focused on dividend‑paying stocks that have the potential to increase dividends over time.

Q. How do you view the current market environment and outlook?

We are experiencing a truly unique market environment, but the significant fiscal and monetary response to the economic upheaval is buying us some room. The underlying carnage is even worse than it looks because the five largest companies account for about a fifth of the S&P 500’s market capitalization and have significantly outperformed. The direction of the market in the near term will depend on the progress we make in reopening the United States and other countries at an acceptable pace and without a resurgence in the pandemic. How successful we are in developing treatments for COVID‑19, the disease caused by the coronavirus, until a vaccine is discovered will also be crucial.

In the meantime, volatility will persist. What’s unusual about the sell‑off is that companies that would be expected to offer some defensiveness just haven’t. Ross Stores, for example, has typically done well in recessions but now their entire fleet of stores is closed. However, periods of severe market volatility and dislocation have historically shown to be good times to invest in high‑quality companies—and we don’t believe this time is different.

Q. How do you assess earnings prospects and valuations now?

You really have to look at earnings on a case‑by‑case and industry‑by‑industry basis. For industries that have been in the eye of the storm—such as travel, retail, and airlines—you can’t focus on the near term. We are looking out to 2021 and 2022 and making investment decisions based on some reasonable level of potential earnings over that time frame. If you are looking out several years, we believe there is still good value in the market, assuming that this pandemic is eventually behind us. Even looking out a year, there appear to be attractive opportunities in some cyclicals, particularly industrials and financials, that have underperformed and should have upside potential.

DIVIDEND GROWERS HAVE OUTPERFORMED

(Fig. 1) S&P 500 Index: returns and volatility

March 31, 1972, to March 31, 2020.

Past performance is not a reliable indicator of future performance. For illustrative purposes only. It is not possible to invest directly in an index.

Source: Copyright 2020 Ned Davis Research, Inc. Further distribution prohibited without prior permission. All Rights Reserved. See “Additional Disclosures” for methodology and additional information on the data.

Q. Companies in the S&P 500 Index and more broadly have been cutting or suspending dividends at the fastest pace since the global financial crisis. Do you expect this trend to continue?

Yes. So far, it’s been concentrated in those industries most directly affected by the pandemic, including travel‑related sectors, some retailers, and energy, which also had an oil supply shock. While we have had a few companies in the fund cut their dividends, we do not expect any impairment in our ability to find attractive stocks.

We have been willing to give companies such as a Hilton or Marriott a little more leash since this situation was not of their making; there was no big strategic mistake. We expect many companies that are suspending dividends will reinstate them at some point. On the brighter side, the two biggest dividend‑paying sectors are technology, where companies tend to have high cash flow, and financials, which tend to have lower payout ratios and are well capitalized. At this point, we think bank dividends will not be suspended, but that could change if this recession lasts more than two or three quarters. However, regulators could require banks to temporarily suspend dividends to preserve capital, as they have already done with share repurchases.

I think the demand for yield will be stronger on the other side of this pandemic than it was going in. Companies with strong balance sheets and durable business models that can maintain and grow their dividends should be attractive for yield‑oriented investors as rates and returns on fixed income securities are likely to remain relatively low. We believe the trend over recent years of companies returning cash to shareholders should continue. A potential dividend yield of 2% to 3% with dividend growth should be valuable.1 It’s also worth remembering that paid dividends are the only portion of stock return that is always positive—earnings growth and share price appreciation certainly are not.

Q. How have you reacted to the market volatility in your investment strategy?

We try to balance our risk‑aware approach to stock selection against the need to move quickly and efficiently as attractive opportunities arise. The indiscriminate sell‑off in March provided the opportunity to buy high‑quality cyclicals with attractive risk/reward characteristics over the intermediate to longer term, especially information technology and industrial companies developing innovative products.

"If you are looking out several years, we believe there is still good value in the market, assuming that this pandemic is eventually behind us."

We used periods like this to add some new companies to the fund that we had been interested in but where the valuations had not been that attractive. We also looked to increase some existing positions at better prices. At the same time, we sold some positions due to concerns about their balance sheets, which are critical when times get tough. So, overall, we were able upgrade quality at more reasonable valuations.

We have long been overweight health care, our second‑largest allocation. Among the defensive sectors of the market, it appears to offer the best combination of fundamentals and valuation. In an election year, there is political risk, particularly for drug companies and managed care. We believe health care companies are proving their value in the pandemic, however, so the political pressure may ease. We have added to several positions, favoring biotechnology and health care equipment and supplies.

We remain overweight industrials and financials—cyclical sectors that have underperformed through this crisis. Within financials, we like insurance and insurance brokers, which have held up reasonably well. The rate environment has hurt the banks’ business models, but valuation is on your side. If we get back on the road to recovery this year, there are good opportunities in both these sectors for investors with reasonable time horizons.

Information technology is our largest underweight position compared with our benchmark but remains one of our top absolute weights. Some companies are poised for strong secular growth. Our holdings are largely focused on IT services and software companies that should benefit from increasing demand for business technology solutions. We also own some quality semiconductor companies.

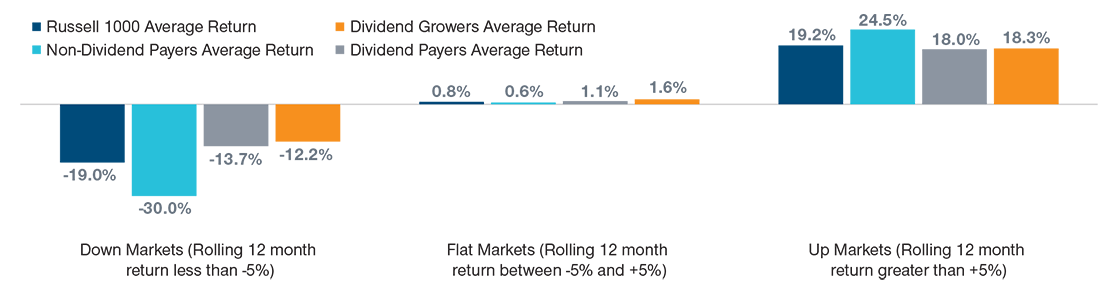

PERFORMANCE IN DIFFERENT MARKET ENVIRONMENTS BY DIVIDEND POLICY

(Fig. 2) Dividend growers have outperformed in down markets

Based on rolling 12 month returns, measured monthly, from 12/31/85 to 12/31/19.

Past performance is not a reliable indicator of future performance.

Sources: Data provided by Compustat (see Additional Disclosures); data analysis by T. Rowe Price. Non Dividend Payers, Dividend Growers and Dividend Payers are subsets of the Russell 1000 Index (see Additional Disclosures for more detail on methodology).

Our investment approach hasn’t changed in 20 years. We try to identify high‑quality companies with reasonable valuations, a defendable business model not subject to disruption, and consistent cash flow that should enable management to invest in the business and pay a dividend that grows over time. And we typically have low turnover; we want these investments to compound for us over at least three to five years.

We believe that our strategy can continue generating strong risk‑adjusted returns, especially when measured over complete market cycles.

"Dividend growers have historically outperformed the market over the long term with less volatility."

Q. In such a tough operating environment, what’s the case for a dividend growth strategy?

Dividend growers have historically outperformed the market over the long term with less volatility. A T. Rowe Price analysis shows that dividend growth stocks in the Russell 1000 Index achieved an annualized total return of 11.3% from the end of 1985 through 2019 compared with 10.8% for dividend payers and 10.5% for the index overall. Also, companies that had both a high dividend yield and high dividend growth, on average, significantly outperformed the dividend payers overall in the index over that period.2

Reinvested dividends accounted for nearly half the S&P 500 Index’s total return over the past 30 years. If we go back to an environment of moderate growth and high debt levels around the world, it’s reasonable to assume equity returns may be less than the long‑term average for some time. In that environment, dividends would be a more important component of the return.

The strategy should work because companies that have a strong record of dividend growth tend to have strong balance sheets and generate consistent cash flow and earnings. They also generally held up better in down markets, although that has not been the case recently. With the entire economy being shut down, yield‑oriented sectors such as industrials, consumer discretionary, financials, and energy were hit relatively harder than they might have been in a normal recession.

There is no such thing as a safe equity strategy, but this investment approach typically focuses on high‑quality businesses. A dividend‑oriented strategy really should be looked at over full market cycles.

DIVIDENDS HAVE BEEN A LARGE PORTION OF TOTAL RETURNS

(Fig. 3) S&P 500 Index: principal versus total return

As of March 31, 2020.

Past performance is not a reliable indicator of future performance.

Source: Standard & Poor’s (see Additional Disclosures). Data analysis by T. Rowe Price.

Since 1986 over 54% of the total return of the S&P 500 Index came from the reinvestment of dividends. Index performance is for illustrative purposes only and is not indicative of any specific investment. Investors cannot invest directly in an index.

Q. What are some of the investment insights you have gained over 20 years managing the Dividend Growth Fund?

Our experience shows that successful long‑term investing requires disciplined adherence to an investment philosophy and process, as well as the ability to look past short‑term market swings to focus on the underlying fundamentals. When you find a solid business run by a competent management team, let it potentially compound for you over time. Time and time again, we’ve learned the lesson that in periods of crisis, a company with a solid balance sheet can pay a strong dividend in terms of performance. Stick to your strategy, try not to be emotional about your holdings, and take a long‑term view.

WHAT WE’RE WATCHING NEXT

We are closely following the reopening of the U.S. economy and whether that ignites a second wave of the coronavirus outbreak. That is key to ascertaining how markets respond. Also, we’ll monitor progress on the development of a coronavirus treatment or vaccine. Success on either front would be a major positive. A rise in tensions between the U.S. and China could destabilize markets, in our view. In the second half of the year, investors will focus more on the U.S. elections. A Democratic sweep could heighten concerns about potential increases in regulation and taxes.

1 Dividends are not guaranteed and are subject to change.

2 Past results are not a reliable indicator of future results. For illustrative purposes only. It is not possible to invest directly in an index. Dividend payers and dividend growers are subsets of the Russell 1000 Index (see Additional Disclosure).

The companies mentioned above represented the following allocations in the Dividend Growth Fund as of March 31, 2020: Ross Stores: 1.04%; Marriott International: 0.50%; Hilton Worldwide Holdings: 0.56%.

Additional Disclosure

Figure 1 shows the historical total returns of S&P 500 component stocks based on their dividend policies. Each stock’s dividend policy is determined by its indicated annual dividend. Ned Davis Research classifies a stock as a dividend-paying stock if the company indicates that it is going to be paying a dividend within the year. This is determined programmatically using indicated annual dividend data. A stock is classified as a non-payer if the stock’s indicated annual dividend is zero. Prior to July 2000, the indicated annual dividends were updated on a quarterly basis. Since July 2000, the indicated annual dividends are updated on a daily basis, so the most up-to-date information is used.

The index returns are calculated using monthly equal-weighted geometric averages of the total returns of all dividend-paying (or non-paying) stocks. A stock’s return is only included during the period if it is a component of the S&P 500 index. The dividend figure used to categorize the stock is the company’s indicated annual dividend, which may be different from the actual dividends paid in a particular month.

Each dividend-paying stock is further classified based on changes to their dividend policy over the previous 12 months. Dividend Growers and Initiators include stocks that increased their dividend anytime in the last 12 months. Once an increase occurs, it remains classified as a grower for 12 months or until another change in dividend policy. Dividend Cutters and Eliminators are companies that have lowered or eliminated their dividend anytime in the last 12 months. Once a decrease occurs, it remains classified as a cutter for 12 months or until another change in dividend policy.

The indices are equal-weighted geometric indices based on monthly total returns, with the constituents of each index reconstituted monthly. This chart thus offers historical perspective on how stock returns and company dividend policy have been related over time. The chart is for perspective purposes only.

T. Rowe Price analysis of performance by dividend policy- At the start of every month, T. Rowe Price categorizes the Russell 1000 index into various categories depending on dividend policy. We then calculate that month’s market-cap weighted returns for each category. We accumulate the returns during the full periods and calculate the annualized total returns for each category. Dividend growers consist of companies whose dividend growth over the prior 12 months was greater than zero. Dividend payers consist of companies whose current dividend yield is greater than zero. Non-dividend payers consist of companies whose current dividend yield equals zero.

London Stock Exchange Group plc and its group undertakings (collectively, the “LSE Group”). © LSE Group 2020. FTSE Russell is a trading name of certain of the LSE Group companies. Russell® is a trade mark(s) of the relevant LSE Group companies and is used by any other LSE Group company under license. All rights in the FTSE Russell indexes or data vest in the relevant LSE Group company which owns the index or the data. Neither LSE Group nor its licensors accept any liability for any errors or omissions in the indexes or data and no party may rely on any indexes or data contained in this communication. No further distribution of data from the LSE Group is permitted without the relevant LSE Group company’s express written consent. The LSE Group does not promote, sponsor or endorse the content of this communication. The LSE Group is not responsible for the formatting or configuration of this material or for any inaccuracy in T. Rowe Price Associates’ presentation thereof.

Copyright © 2020, S&P Global Market Intelligence (and its affiliates, as applicable). Reproduction of any information, data or material, including ratings (“Content”) in any form is prohibited except with the prior written permission of the relevant party. Such party, its affiliates and suppliers (“Content Providers”) do not guarantee the accuracy, adequacy, completeness, timeliness or availability of any Content and are not responsible for any errors or omissions (negligent or otherwise), regardless of the cause, or for the results obtained from the use of such Content. In no event shall Content Providers be liable for any damages, costs, expenses, legal fees, or losses (including lost income or lost profit and opportunity costs) in connection with any use of the Content. A reference to a particular investment or security, a rating or any observation concerning an investment that is part of the Content is not a recommendation to buy, sell or hold such investment or security, does not address the suitability of an investment or security and should not be relied on as investment advice. Credit ratings are statements of opinions and are not statements of fact.

Important Information

Call 1-800-225-5132 to request a prospectus or summary prospectus; each includes investment objectives, risks, fees, expenses, and other information you should read and consider carefully before investing.

This material is provided for informational purposes only and is not intended to be investment advice or a recommendation to take any particular investment action.

The views contained herein are those of the authors as of May 2020 and are subject to change without notice; these views may differ from those of other T. Rowe Price associates.

This information is not intended to reflect a current or past recommendation, investment advice of any kind, or a solicitation of an offer to buy or sell any securities or investment services. The opinions and commentary provided do not take into account the investment objectives or financial situation of any particular investor or class of investor. Investors will need to consider their own circumstances before making an investment decision.

Information contained herein is based upon sources we consider to be reliable; we do not, however, guarantee its accuracy.

Past performance is not a reliable indicator of future performance. All investments are subject to market risk, including the possible loss of principal. Dividends are not guaranteed and are subject to change. The fund’s emphasis on dividend-paying companies could result in significant investments in large‑capitalization stocks. Dividend-paying stocks may lag shares of smaller, faster-growing companies. Also, stocks that appear temporarily out of favor may remain out of favor for a long time. All charts and tables are shown for illustrative purposes only.

T. Rowe Price Investment Services, Inc.

© 2020 T. Rowe Price. All rights reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the bighorn sheep design are, collectively and/or apart, trademarks or registered trademarks of T. Rowe Price Group, Inc.

Global Weekly Commentary: Higher bar for U.S. earnings to deliver

We saw 2024 as a year of two stories. First, cooling inflation and solid corporate earnings would support upbeat risk appetite.

Global Markets Weekly Update: April 19, 2024

Review the performance of global stock and bond markets over the past week, along with relevant insights from T. Rowe Price economists and investment professionals.

Weekly Investment Commentary: Earnings season: investment ideas

First-quarter earnings season has kicked off with the utilities and communication services sectors projected to deliver the strongest year-over-year EPS growth, while estimates for materials and energy are expected to decline the most.