Anatomy of a Recession: Is Labor Market Economic Kevlar or Achilles Heel?

Key Takeaways

- While the labor market remains an economic bright spot, the Federal Reserve (Fed) may continue its tightening policy until more signs emerge that job growth and wages are experiencing substantial slowdowns. Both have cooled from their peaks but remain elevated compared to pre-pandemic norms.

- Failure to address elevated inflation in the near term may stave off a shallower recession now, but risks unleashing a wage-price spiral that may require an even deeper recession later to restore price stability.

- Deteriorating margins caused Profit Margins on the ClearBridge Recession Risk Dashboard to worsen from yellow to red this month and could lead to increased layoffs in 2023.

Robust Wages and Job Creation May Keep the Fed Hawkish

Economic data has pointed to a downshift in the pace of growth over the last several months, culminating with the headline Institute for Supply Management (ISM) Manufacturing Purchasing Managers' Index (PMI) slipping into contractionary territory (below 50) with a 49.0 reading for November. However, the strength of the labor market has remained an economic bright spot with 263,000 net hires last month. Over the last four months, job creation has averaged 277,000, substantially stronger than the average of 156,000 seen during the second half of 2018 and 2019. We believe that period represents something close to the sustainable pace of job creation, given the unemployment rate stayed below 4% throughout it.

Unfortunately, the strength of the labor market, which many view as a Kevlar shield protecting the economy, could ultimately prove to be its Achilles heel. With inflation remaining elevated, the Fed has targeted labor market weakness as one of the key signals in determining how far to tighten monetary policy. In a speech last week, Fed Chairman Jerome Powell laid out four criteria necessary to restore price stability and bring inflation back to 2%, with the labor market being the only one that hasn’t seen signs of improvement. Excess demand for labor continues to drive wages to unsustainably strong levels well above what would be consistent with 2% inflation. As such, the Fed may continue its tightening policy until policymakers see more signs the labor market is softening and wages are cooling.

Historically, the labor market has been one of the last dominoes to fall as the economy slips into recession. This means that the Fed’s laser focus on the labor market runs the risk of overtightening, and by the time the data suggests backing off it could already be too late. While the Fed is certainly aware of this lag, it finds itself between a rock and a hard place given the prolonged, elevated rate of inflation. Current conditions risk unleashing a wage-price spiral – a phenomenon where workers request and receive larger wage hikes to combat rising prices, allowing them to consume more and push prices even higher, creating a feedback loop between wages and inflation – or a recession. A wage-price spiral was a key feature of the inflationary 1970s and would likely be the worse outcome, requiring a deeper recession down the road to restore price stability.

There is hope, however, that both outcomes can be avoided if the labor market tightens without destroying too many jobs, something we have dubbed the “immaculate slackening.” Specifically, JOLTS (Job Openings and Labor Turnover Survey) job openings are substantially higher than pre-pandemic levels (10.3 million today vs 7.0 million in February 2020) while the total number of people employed is not (153.5 million today vs. 152.5 million in February 2020). This suggests there is room to cool labor demand and slow wage growth without incurring too many job losses. Although job openings have come down from their 11.9 million peak earlier this year, like the ricochet of Terry Bradshaw’s pass before Franco Harris finally hauled it in for a touchdown dubbed the “Immaculate Reception,” there is still a long way to go for the immaculate slackening to play out.

Exhibit 1: The Immaculate Slackening

Job openings data as of Oct. 31, 2022. Unemployment data as of Nov. 30, 2022. Source: Bureau of Labor Statistics, National Bureau of Economic Research and Bloomberg.

The labor market has slowed but remains elevated relative to history. In addition to job openings, the quits rate - a subcomponent of the JOLTS data - has eased from a high of 3.0% one year ago to 2.6% last month, suggesting declining optimism as workers are less likely to quit without having a new job lined up, or confidence they can find a new one easily. Still, the 2.6% rate is higher than the pre-pandemic peak of 2.4% over the roughly 20-year history of the series.

Furthermore, the percentage of respondents in the NFIB Small Business Economic Trends Survey listing hiring as their top operating problem has dropped from 51% last fall to 46%, but still remains well above its historical peak of 33% prior to the pandemic. While all three data sets suggest things are headed in the right direction, substantial further progress is needed to convince the Fed that employment and inflation will fall to more sustainable levels.

Wages are demonstrating similar behavior, with most wage metrics having peaked in the first quarter of this year before slowing to a pace that remains hotter than the Fed would like. Average Hourly Earnings have fallen from 5.6% in March to 5.1% but are still well above the 3.6% peak seen during the last expansion.1 Job creation has also downshifted from an average of 590,000 new jobs per month in the second half of 2021 and 444,000 over the first half of 2022 to just 277,000 over the last four months.2 Additionally, the household survey of the jobs report used to calculate the unemployment rate has been much weaker than the establishment survey (the source of headline non-farm payrolls) over the last two months, registering negative prints while headline job numbers remain solidly positive. Historically, the household survey has provided a better read at recessionary inflection points, which is something to monitor as we head into the new year.

Contracting Margins May Soon Force Layoffs

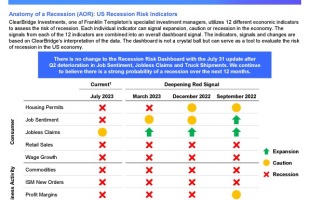

Corporate margins are one of the catalysts bolstering the labor market. With profits flush and labor scarce coming out of the pandemic, companies have been more hesitant to trim headcount. However, this could be changing as we move into 2023 as corporate profits come under increased pressure. Margins peaked approximately one year ago, but their deterioration has recently accelerated and could jump start a more traditional recessionary layoff cycle. In fact, this month saw the Profit Margins indicator on the ClearBridge Recession Risk Dashboard worsen from yellow to red, indicating that the threshold for reduced headcounts could be approaching. With no other signal changes this month, the overall reading remains firmly in recessionary, or red, territory.

Exhibit 2: ClearBridge Recession Risk Dashboard

Source: ClearBridge Investments.

Last month we highlighted our view that the bounce from the mid-October lows represented a countertrend rally, and an extension of the forecast we laid out the previous month. We continue to believe the lows for this bear market are still to come, and that a rally following the midterm elections is not surprising from a historical perspective. While many are hopeful the labor market will be this expansion’s Kevlar armor, the further Fed tightening it may induce could ultimately prove its Achilles heel. We continue to see a choppy path for equities as investors navigate an unsettled environment, and as the lagged effects of monetary tightening bump into a surprisingly resilient consumer. As such, we continue to advocate equity tilts toward defensive sectors and a quality bias over the intermediate term.

Endnotes

- Source: U.S. Bureau of Labor Statistics.

- Ibid.

Definitions

The ClearBridge Recession Risk Dashboard is a group of 12 indicators that examine the health of the U.S. economy and the likelihood of a downturn.

The Institute for Supply Management’s (ISM) Purchasing Managers Index (PMI) for the US manufacturing sector measures sentiment based on survey data collected from a representative panel of manufacturing and services firms. PMI levels greater than 50 indicate expansion; below 50, contraction.

In economic terms, Kevlar shield means protection for the economy having high tensile strength and temperate resistance.

Achilles heel is defined as a weakness or vulnerable point.

WHAT ARE THE RISKS?

Past performance is no guarantee of future results. Please note that an investor cannot invest directly in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges.

Equity securities are subject to price fluctuation and possible loss of principal. Fixed-income securities involve interest rate, credit, inflation and reinvestment risks; and possible loss of principal. As interest rates rise, the value of fixed income securities falls. International investments are subject to special risks including currency fluctuations, social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets. Commodities and currencies contain heightened risk that include market, political, regulatory, and natural conditions and may not be suitable for all investors.

U.S. Treasuries are direct debt obligations issued and backed by the “full faith and credit” of the U.S. government. The U.S. government guarantees the principal and interest payments on U.S. Treasuries when the securities are held to maturity. Unlike U.S. Treasuries, debt securities issued by the federal agencies and instrumentalities and related investments may or may not be backed by the full faith and credit of the U.S. government. Even when the U.S. government guarantees principal and interest payments on securities, this guarantee does not apply to losses resulting from declines in the market value of these securities.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Distributors, LLC, One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com - Franklin Distributors, LLC is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

Franklin Distributors, LLC

Anatomy of a Recession Update: Cracks in the Foundation

Get perspective on the most recent US economic data, the investor’s view, and how reviewing previous recessionary periods may help us today, in this conversation with Jeff Schulze, Head of Economic and Market Research at ClearBridge Investments.

AOR Update: When to expect a recession?

ClearBridge Investments: Despite improving economic sentiment now leaning the consensus view toward a soft landing, we continue to believe a recession is on the horizon.

Anatomy of a Recession: Economic and Market Outlook 3Q 2023 | August 1st

ClearBridge Investments, one of Franklin Templeton’s specialist investment managers, utilizes 12 different economic indicators to assess the risk of recession.