3 Points About China

Clamping down on China has become a bipartisan effort in the United States, but I believe an outright conflict between China and Taiwan is a low-probability (albeit high-impact) event—and I remain constructive on the bottom-up, long-term investment opportunities in China, including the transition to a domestic-consumption-driven and lower-carbon economy.

Learn more by watching our Just a Minute videos or reading the transcripts below. And read Vivian’s 2023 outlook: China Reopening Should Drive Growth.

There’s no doubt we are in a rising geopolitical risk environment on the global level. Clamping down on China has become a bipartisan effort in the United States.

This creates a risk factor for investors that has little to do with fundamentals. If you look at restrictions on semiconductor sales to China, for example, China could deal with the problem technically and practically over time, but it does raise bigger concerns about the investability of Chinese equities.

A U.S.-based investor has to ask whether the U.S. government may eventually put China-based tech companies on the restricted entity list.

China-Taiwan Conflict is Likely A Low-Probability Event

We believe that the China-Taiwan conflict at this point stays as a low-probability but high-impact event.

If there were conflict happening to those two countries and regions, the impact is going to be more widespread, not just to China and Taiwan, and the industries that are impacted will be also very broad-based.

We believe that the risk premium of Chinese equities and certain Taiwanese equities will have to factor in the rising geopolitical risks.

But other than that, we’ll continue to focus on the fundamental cycle considerations, and then figure out the best risk-reward metrics for the companies we invest in.

Energy Transition Could Be a Chinese Growth Story

A long-term structural story we like a lot is energy transition, including electrical vehicle batteries, solar panels, and related companies.

These higher-valuation segments underperformed traditional energy companies in 2022, but we remain bullish on the long-term opportunities related to the transition to a lower-carbon economy.

We pay close attention to fundamental corporate earnings, which are already in recovery. If you combine the earnings recovery with attractive valuations and a stabilizing regulatory environment, plus reopening and policy support, 2023 may be a good year for quality growth investors.

Vivian Lin Thurston, CFA, partner, is a portfolio manager on William Blair’s global equity team.

Want more insights on the economy and investment landscape? Subscribe to our blog.

This content is for informational and educational purposes only and not intended as investment advice or a recommendation to buy or sell any security. Investment advice and recommendations can be provided only after careful consideration of an investor’s objectives, guidelines, and restrictions.

Information and opinions expressed are those of the authors and may not reflect the opinions of other investment teams within William Blair Investment Management, LLC, or affiliates. Factual information has been taken from sources we believe to be reliable, but its accuracy, completeness or interpretation cannot be guaranteed. Information is current as of the date appearing in this material only and subject to change without notice. Statements concerning financial market trends are based on current market conditions, which will fluctuate. This material may include estimates, outlooks, projections, and other forward-looking statements. Due to a variety of factors, actual events may differ significantly from those presented.

Investing involves risks, including the possible loss of principal. Equity securities may decline in value due to both real and perceived general market, economic, and industry conditions. The securities of smaller companies may be more volatile and less liquid than securities of larger companies. Investing in foreign denominated and/or domiciled securities may involve heightened risk due to currency fluctuations, and economic and political risks. These risks may be enhanced in emerging markets. Different investment styles may shift in and out of favor depending on market conditions. Individual securities may not perform as expected or a strategy used by the Adviser may fail to produce its intended result.

Investing in the bond market is subject to certain risks including market, interest rate, issuer, credit, and inflation risk. Rising interest rates generally cause bond prices to fall. High-yield, lower-rated, securities involve greater risk than higher-rated securities. Sovereign debt securities are subject to the risk that an entity may delay or refuse to pay interest or principal on its sovereign debt because of cash flow problems, insufficient foreign reserves, or political or other considerations. Derivatives may involve certain risks such as counterparty, liquidity, interest rate, market, credit, management, and the risk that a position could not be closed when most advantageous. Diversification does not ensure against loss. The inclusion of Environmental, Social and Governance (ESG) factors beyond traditional financial information in the selection of securities could result in a strategy's performance deviating from other strategies or benchmarks, depending on whether such factors are in or out of favor. ESG analysis may rely on certain values based criteria to eliminate exposures found in similar strategies or benchmarks, which could result in performance deviating.

There can be no assurance that investment objectives will be met. Any investment or strategy mentioned herein may not be appropriate for every investor. References to specific companies are for illustrative purposes only and should not be construed as investment advice or a recommendation to buy or sell any security. Past performance is not indicative of future returns.

Privacy & Security | Cookie Policy | Social Media Disclaimer | FINRA’s BrokerCheck | Glossary

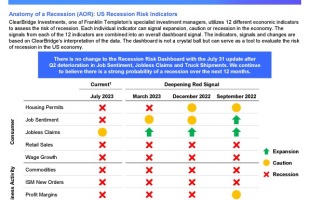

Anatomy of a Recession Update: Cracks in the Foundation

Get perspective on the most recent US economic data, the investor’s view, and how reviewing previous recessionary periods may help us today, in this conversation with Jeff Schulze, Head of Economic and Market Research at ClearBridge Investments.

AOR Update: When to expect a recession?

ClearBridge Investments: Despite improving economic sentiment now leaning the consensus view toward a soft landing, we continue to believe a recession is on the horizon.

Anatomy of a Recession: Economic and Market Outlook 3Q 2023 | August 1st

ClearBridge Investments, one of Franklin Templeton’s specialist investment managers, utilizes 12 different economic indicators to assess the risk of recession.