In 2022, Don't Predict. Prepare.

Key takeaways

- Our focus is to guide investors through whatever challenges may come so that they can achieve their goals. We are not economists. We don’t predict. We invest. Our job is to prepare.

- Volatility, the rise and fall of prices, is inevitable, particularly over shorter time horizons. Rather, we aim to judiciously compound returns and avoid permanent capital impairment.

- We counsel careful consideration for investment goals, thoughtful portfolio selection, and periodic checks to ensure the portfolio is still a fit—meaning that goals or circumstances haven’t changed so much that a new portfolio is in order.

According to an old Yiddish proverb, “We plan; God laughs.” Wherever you fall along the spectrum of belief, that dynamic applies to investing as well, particularly for those who think they can time the market or reliably predict what returns they will reap and when.

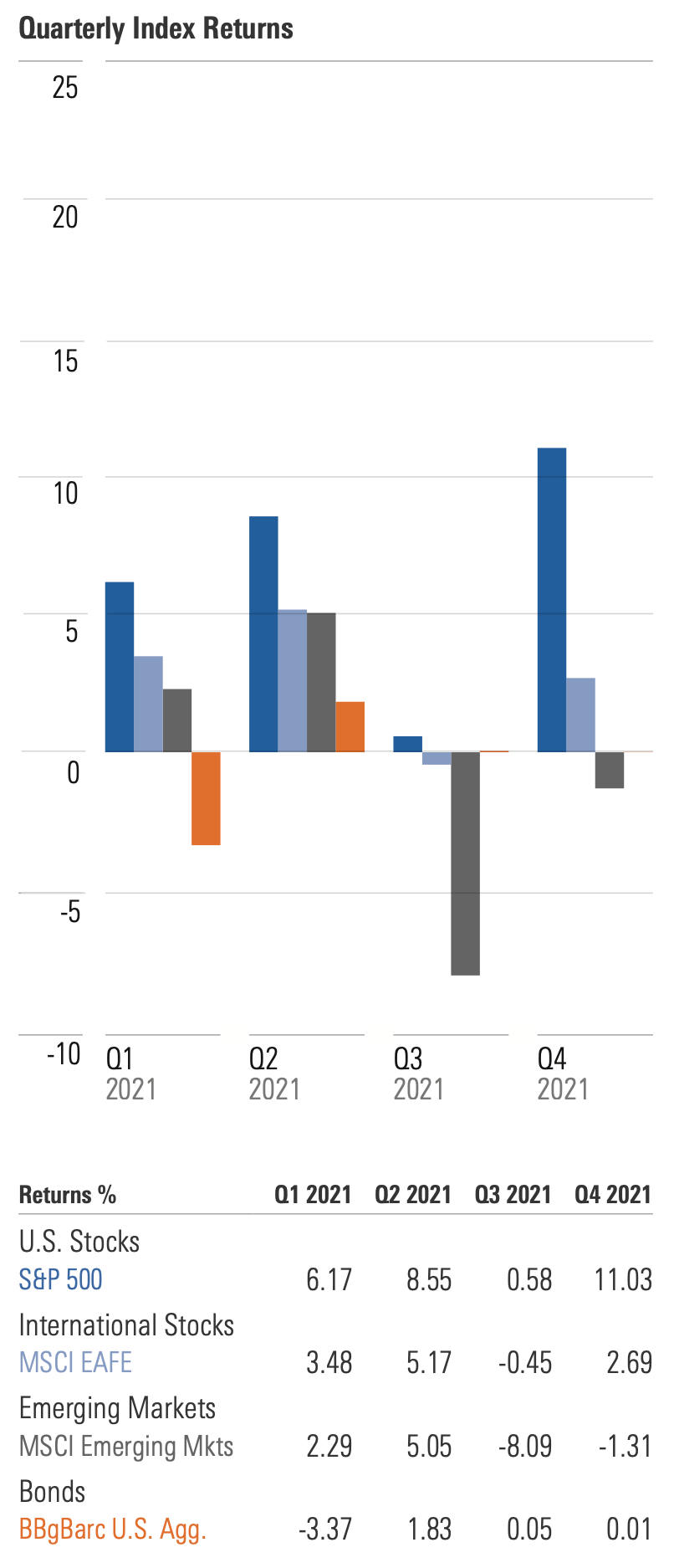

Now, that is in no way meant to wrap up 2021 on a pessimistic note. Far from it, as the 12 months coming to a close mark the 10th double-digit gain for U.S. equities (as measured by the Morningstar US Total Market Index) in the 13 years since 2008.

However, in the fixed-income realm, U.S. core bonds lost modest ground as investors fretted about the prospect of rising rates and sustained increases in inflation over the coming year. Those investors may soon find themselves in a growing crowd as any number of worries begin to take hold, from the aforementioned rates and inflation to the suspicion that the unrelenting success of equities is a streak that must come to an end, making a pullback feel inevitable.

Risks abound, from those we can see now to whatever’s hiding around the corner. And the soothsaying game has left a long line of those who got it wrong in their wake, which is why we don’t play it. Instead, our focus is to guide investors through whatever challenges may come so that they can achieve their goals.

We are not economists. We don’t predict. We invest. Our job is to prepare.

We start with valuation, or the prices we pay for different asset classes. We aim to invest in opportunities, be they particular countries or sectors, when we believe they are priced below their fair value. Not unlike the post-holiday shopper seeking two-for-one sales in the Sunday circular, we want to get more for what we pay.

Next, we consider the market environment. We don’t fixate on one; we consider a range of eventualities. We consider how asset classes could behave in a prolonged period of high inflation, for example, or a sustained market sell-off due to a new and fast-spreading COVID variant. We test the potential for rising rates and their resulting impact on stocks and bonds, and even the possibility for the stock market’s prolonged rally to continue.

The idea is not to dodge every loss or snatch every gain. Volatility, the rise and fall of prices, is inevitable, particularly over shorter time horizons. Rather, we aim to judiciously compound returns and avoid permanent capital impairment, which is an inelegant way of describing losses from which an investment cannot recover. That is the most serious consideration for investors who have actual goals attached to their portfolios.

We believe that when it’s carefully implemented, a dual focus—a valuation mindset and an effort to balance the risks portfolios may encounter as market conditions evolve—gives us the best chances of seeing portfolios deliver on their objectives over the long term. Because again, we’re not trying to predict. We’re trying to prepare. We are not market timers.

Why not? Research repeatedly shows that attempts at market timing—to cash out and wait for happier times—will very often lead to worse investment outcomes. Counterintuitively, it can be a matter of missing the upside: studies show that while market timers may manage to miss some of the market’s losses, they rarely can foresee when markets swing back to gains, ultimately remaining in cash while the market grinds higher.

Rather than encouraging advisors and their clients to swing in and out of the market, we counsel careful consideration for investment goals, thoughtful portfolio selection, and periodic checks to ensure the portfolio is still a fit—meaning that goals or circumstances haven’t changed so much that a new portfolio is in order—and to ensure a good night's sleep.

In other words, let us worry about what’s next. Not as a matter of prediction but as a matter of preparation. That’s what we are here for, and we’re grateful that you’re with us to end one year and ring in a new one. We value you and your trust in our partnership, and we look forward to spending 2022 with you.

Opinions expressed are as of the current date; such opinions are subject to change without notice. Morningstar Investment Management shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions or their use. This commentary is for informational purposes only. The information, data, analyses, and opinions presented herein do not constitute investment advice, are provided solely for informational purposes and therefore are not an offer to buy or sell a security. Please note that references to specific securities or other investment options within this piece should not be considered an offer (as defined by the Securities and Exchange Act) to purchase or sell that specific investment. Performance data shown represents past performance. Past performance does not guarantee future results. All investments involve risk, including the loss of principal. There can be no assurance that any financial strategy will be successful. Morningstar Investment Management does not guarantee that the results of their advice, recommendations or objectives of a strategy will be achieved. This commentary contains certain forward-looking statements. We use words such as “expects”, “anticipates”, “believes”, “estimates”, “forecasts”, and similar expressions to identify forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason. Past performance does not guarantee future results. Morningstar® Managed PortfoliosSM are offered by the entities within Morningstar’s Investment Management group, which includes subsidiaries of Morningstar, Inc. that are authorized in the appropriate jurisdiction to provide consulting or advisory services in North America, Europe, Asia, Australia, and Africa. In the United States, Morningstar Managed Portfolios are offered by Morningstar Investment Services LLC or Morningstar Investment Management LLC, both registered investment advisers, as part of various advisory services offered on a discretionary or non-discretionary basis. Portfolio construction and on-going monitoring and maintenance of the portfolios within the program is provided on Morningstar Investment Services behalf by Morningstar Investment Management LLC. Morningstar Managed Portfolios offered by Morningstar Investment Services LLC or Morningstar Investment Management LLC are intended for citizens or legal residents of the United States or its territories and can only be offered by a registered investment adviser or investment adviser representative. Investing in international securities involve additional risks. These risks include, but are not limited to, currency risk, political risk, and risk associated with varying accounting standards. Investing in emerging markets may increase these risks. Emerging markets are countries with relatively young stock and bond markets. Typically, emerging-markets investments have the potential for losses and gains larger than those of developed-market investments. A debt security refers to money borrowed that must be repaid that has a fixed amount, a maturity date(s), and usually a specific rate of interest. Some debt securities are discounted in the original purchase price. Examples of debt securities are treasury bills, bonds and commercial paper. The borrower pays interest for the use of the money and pays the principal amount on a specified date. The indexes noted are unmanaged and cannot be directly invested in. Individual index performance is provided as a reference only. Since indexes and/or composition levels may change over time, actual return and risk characteristics may be higher or lower than those presented. Although index performance data is gathered from reliable sources, Morningstar Investment Management cannot guarantee its accuracy, completeness or reliability.

Weekly Investment Commentary: Munis offer yield relief from inflation’s heat

U.S. yields began the year at their highest starting level since 2011, and they have since risen further across the Treasury and municipal curves.

Global Weekly Commentary: Higher bar for U.S. earnings to deliver

We saw 2024 as a year of two stories. First, cooling inflation and solid corporate earnings would support upbeat risk appetite.

Global Markets Weekly Update: April 19, 2024

Review the performance of global stock and bond markets over the past week, along with relevant insights from T. Rowe Price economists and investment professionals.