Understanding Gold: An Expensive Insurance Policy?

Key Takeaways

- Gold has enjoyed a stellar run, prompting some investors to rethink its viability as an investment.

- Gold also has a record of offsetting equity and inflation risks; these characteristics have increased its appeal in today’s uncertain environment.

- As a portfolio holding, the evidence is far less compelling.

- The merits of gold make for interesting debate, but it may be thought of as an expensive insurance policy that is best avoided.

Financial market moves can best be described with one word—unprecedented. The market moves have been nothing short of breathtaking, with the swift action of governments and central banks providing support in the form of fiscal stimulus and lower interest rates, which have no doubt played a role in the recovery. This comes despite the economic ramifications of COVID-19, which continues to filter through to weak economic data and company earnings announcements.

One of the most significant winners year-to-date in 2020 has been gold. The price of the precious metal has risen meaningfully since the beginning of the year, in the process becoming one of the most talked about trades of 2020. This has driven the performance of gold mining companies listed on global stock exchanges—many of which are up over 100% since the beginning of the year. Even long-term gold cynic, Warren Buffett, made news headlines recently when it was announced that his company, Berkshire Hathaway, added a small stake in Toronto-based Barrick Gold (one of the world’s largest gold producers) to its portfolio in the second quarter of the year.

So, what is behind the sudden interest in the yellow metal? We look at the history of gold as an investment and what may have been driving the rise in the price of gold in 2020.

A Historic Look at Gold as an Investment

Is buying gold speculation, or can we call it an “investment”? On one hand, gold doesn’t produce cash flows, so can’t be valued. Or said another way—its price varies based on something other than its ability to provide investors future cash flows. This makes it a challenging asset for investors (especially for valuation-driven investors like us), with any investment thesis relying instead on supply/demand inputs and price discovery based on what the next investor thinks it is worth.

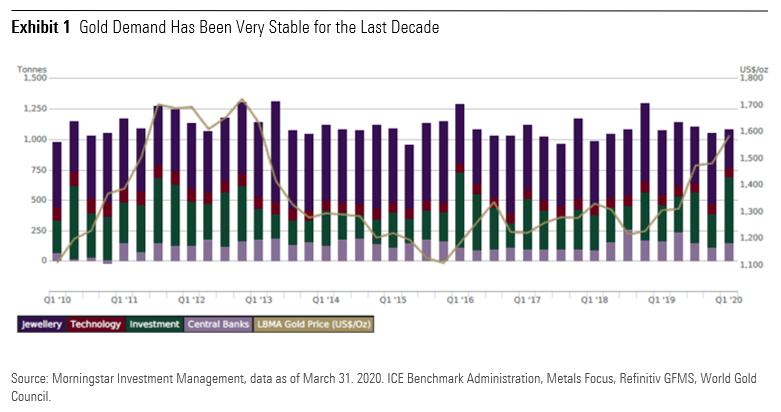

These characteristics limit an investor’s ability to assess a potential investment, creating a wider range of potential outcomes than say bonds. On this basis, investor sentiment is a difficult variable and gold does have a history of enduring major setbacks, with drawdowns of over 10% not uncommon. Even in today’s environment, where some people argue for a path toward higher demand for gold from central banks and asset holders, the evidence is less clear.

On the other side, gold has a long and alluring history as a safe-haven investment. This is largely since the price of gold is independent of other asset classes, which means that the metal has generally performed well during periods of market stress or volatility. Gold has also traditionally been a refuge against U.S. dollar weakness, largely due to the inverse relationship between what is generally accepted as the world’s reserve currency and commodity prices.

We have an additional layer of consideration too, as investments in gold generally take place in one of three forms: buying the commodity itself (gold bullion), buying so-called derivative investments (like options or futures based on changes to the gold price), or buying shares of companies that mine and sell gold (gold equity, like Barrick Gold).

Of note, investments in gold stocks bring different return/risk drivers to a portfolio, as business decisions impact corporate revenues and cash flows. Additionally, due to the impact of leverage (both financial and operating), investments in gold stocks tend to be more volatile than the direct investment in the physical commodity. Importantly, these companies produce cash flows that can be valued.

Investing in Gold as Protection Against Market Declines

Historically, gold is broadly uncorrelated to other major asset classes. That said, it has created a reputation for excelling during periods of significant market declines and periods of unusually high market volatility. During several market panics over the last century, the metal posted significantly better returns during market drawdowns and in some cases, has even notched positive total returns during periods of steep losses in equity markets.

More recently, the COVID-19 sell-off provided an interesting case study in that although gold fared better than stocks, it still posted a small loss during the “panic phase”. Market commentators have attributed this to many factors, including the fact that the sell-off was liquidity-driven (and therefore all encompassing) and the feeling that interest rate cuts will support the U.S. dollar (a negative for commodity prices). Lockdown measures introduced across the globe also caused mine closures and production shutdowns which affected gold producers negatively. Gold did, however, reverse course, moving significantly higher in the months following the market sell-off.

Gold as an Inflation Hedge

Despite often being regarded as a hedge against inflation, it is interesting to note that gold’s record of protection is rather mixed. The metal did provide significant protection during the high inflationary period of the 1970s, when higher oil prices and an expanding money supply pushed inflation to extreme levels in the United States and elsewhere. During more muted periods of inflation, including the early 1980s and between 1988-91, gold delivered negative returns, lagging equity markets in the process.

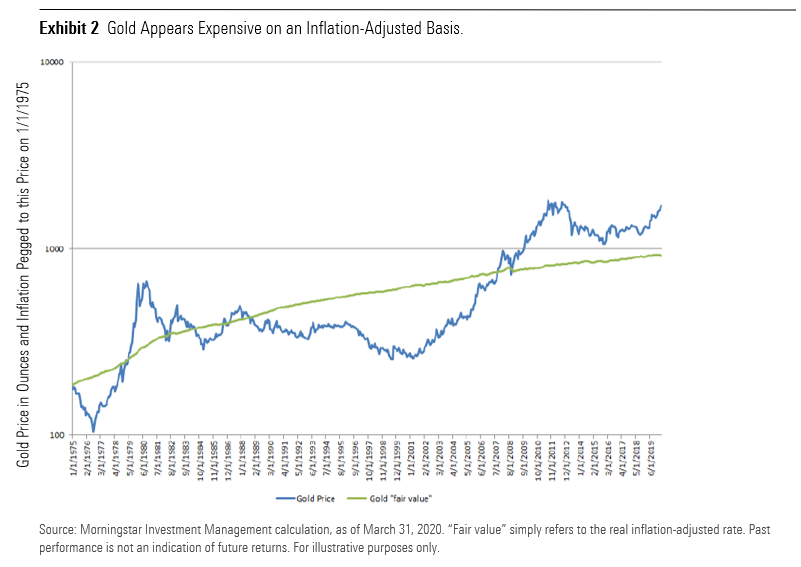

Given the unprecedented levels of fiscal stimulus delivered by major central banks and governments in response to the pandemic, concerns have been raised that this may lead to a significant uptick in inflation. While this may be true, the evidence suggests that gold’s role as an inflation hedge may be overdone and that there is no guarantee that the metal will provide protection if inflation becomes a problem. Related to this, we can see in Exhibit 2 that today’s pricing makes this a challenge. On a real basis (after inflation), gold is already expensive and could therefore suffer a material drawdown, on our analysis.

Put frankly, we must look forward through the windshield rather than backward through the rear-vision mirror. On a forward-looking basis, it is not conclusive that adding gold allocations to a portfolio will be beneficial, especially given the drawdown risk it may face.

So, What Should We Conclude About Gold From the Evidence?

Gold does not produce any cash flows and could experience a meaningful drawdown from current levels. Practically speaking, it is important to remember that the track record of the precious metal is mixed, and gold can go through long periods of underperformance. While an investor might expect gold to keep up with inflation in the very long-run, the strongest evidence for holding gold appears to be as a safe haven in periods of significant market volatility.

In this sense, it may be better viewed as an expensive insurance policy rather than a core holding. Investors should also be wary of the hype currently surrounding the price movements of gold—after all, as Warren Buffett once famously said: “What the wise man does in the beginning, the fool does in the end."

Opinions expressed are as of the current date; such opinions are subject to change without notice. Morningstar Investment Management shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions or their use. This commentary is for informational purposes only. The information, data, analyses, and opinions presented herein do not constitute investment advice, are provided solely for informational purposes and therefore are not an offer to buy or sell a security. Please note that references to specific securities or other investment options within this piece should not be considered an offer (as defined by the Securities and Exchange Act) to purchase or sell that specific investment. Performance data shown represents past performance. Past performance does not guarantee future results. All investments involve risk, including the loss of principal. There can be no assurance that any financial strategy will be successful. Morningstar Investment Management does not guarantee that the results of their advice, recommendations or objectives of a strategy will be achieved. This commentary contains certain forward-looking statements. We use words such as “expects”, “anticipates”, “believes”, “estimates”, “forecasts”, and similar expressions to identify forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason. Past performance does not guarantee future results. Morningstar® Managed PortfoliosSM are offered by the entities within Morningstar’s Investment Management group, which includes subsidiaries of Morningstar, Inc. that are authorized in the appropriate jurisdiction to provide consulting or advisory services in North America, Europe, Asia, Australia, and Africa. In the United States, Morningstar Managed Portfolios are offered by Morningstar Investment Services LLC or Morningstar Investment Management LLC, both registered investment advisers, as part of various advisory services offered on a discretionary or non-discretionary basis. Portfolio construction and on-going monitoring and maintenance of the portfolios within the program is provided on Morningstar Investment Services behalf by Morningstar Investment Management LLC. Morningstar Managed Portfolios offered by Morningstar Investment Services LLC or Morningstar Investment Management LLC are intended for citizens or legal residents of the United States or its territories and can only be offered by a registered investment adviser or investment adviser representative. Investing in international securities involve additional risks. These risks include, but are not limited to, currency risk, political risk, and risk associated with varying accounting standards. Investing in emerging markets may increase these risks. Emerging markets are countries with relatively young stock and bond markets. Typically, emerging-markets investments have the potential for losses and gains larger than those of developed-market investments. A debt security refers to money borrowed that must be repaid that has a fixed amount, a maturity date(s), and usually a specific rate of interest. Some debt securities are discounted in the original purchase price. Examples of debt securities are treasury bills, bonds and commercial paper. The borrower pays interest for the use of the money and pays the principal amount on a specified date. The indexes noted are unmanaged and cannot be directly invested in. Individual index performance is provided as a reference only. Since indexes and/or composition levels may change over time, actual return and risk characteristics may be higher or lower than those presented. Although index performance data is gathered from reliable sources, Morningstar Investment Management cannot guarantee its accuracy, completeness or reliability.

Demystifying private markets: The markets have changed, so have perspectives on allocations

We believe private markets can improve investors’ financial security and make financial plans more resilient.

The case for private markets: three things to know

Investors should consider three important benefits as they evaluate allocating to private markets.

The Case for Real Assets: Staying Ahead of Inflation

Investors’ real rate of return = Nominal rate of return – Inflation rate. Learn about how inflation can affect your clients' real assets.