Three Factors Shaping Prospects in Frontier Markets

KEY INSIGHTS

- Market conditions over the remainder of 2019 are generally expected to improve, as political and economic developments that have weighed on asset prices abate.

- With asset prices largely reflecting the challenges of the past year, a shift in sentiment could provide equities with an uplift.

- Primary catalysts set to drive asset prices include: elections, MSCI reclassifications, and geopolitical and trade developments.

Frontier markets experienced a challenging year in 2018, but as we enter the latter stages of 2019, we believe three distinct dynamics are working to drive a turnaround in performance in the sector.

The global economy presented headwinds in 2018, but the low correlation of the asset class with the global cycle has meant that country‑level political and economic developments have typically weighed on frontier markets the most.

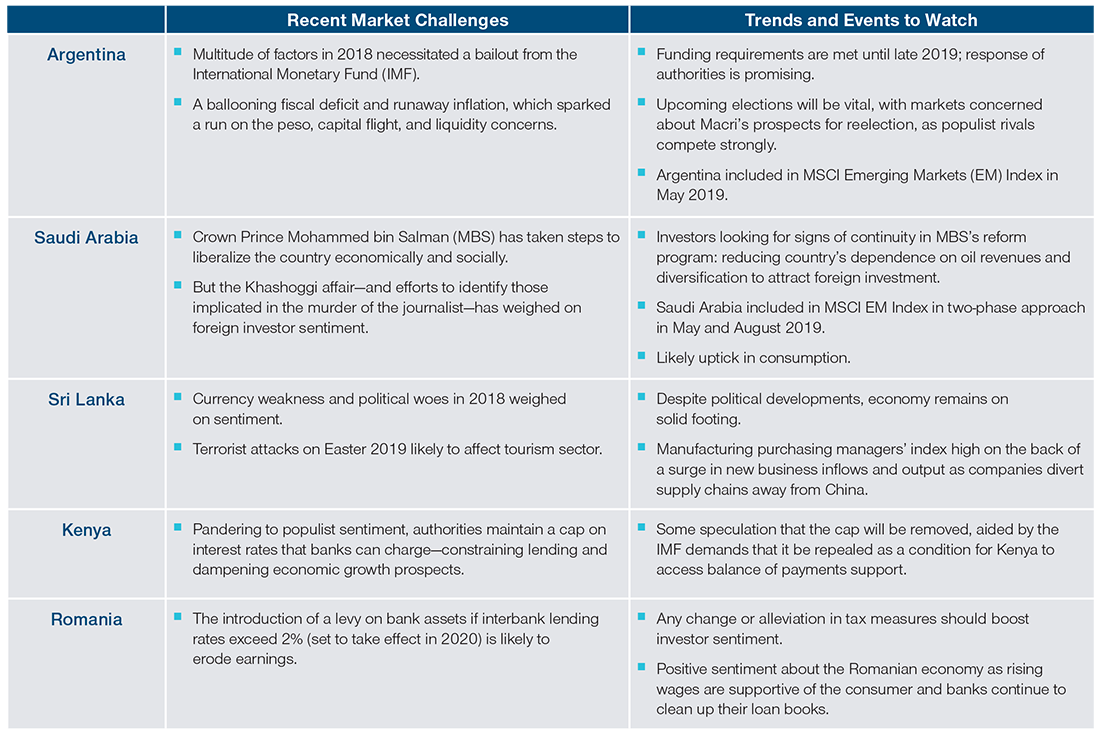

In 2018, Argentina was mired in a crisis, Saudi Arabia struggled with foreign investor perceptions, Sri Lanka faced a leadership vacuum, and harmful tax measures in Kenya and Romania took a toll on their respective financial sectors. As these issues are addressed or fade, 2019 could present a silver lining.

Catalysts Set to Drive Markets

Adopting a broad, overarching view, we have identified three factors that have the potential to drive frontier market performance: elections, MSCI reclassifications, and geopolitical and trade developments.

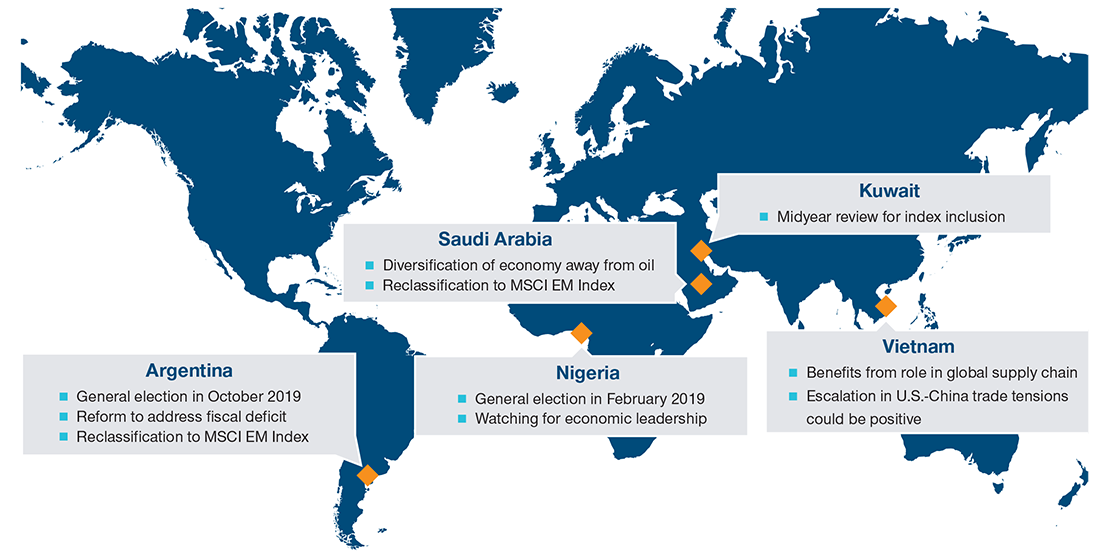

(FIG. 1) KEY DEVELOPMENTS IN FRONTIER MARKET COUNTRIES

Key events across the frontier markets spectrum.

Key Elections

Argentina is set for a crucial general election in October 2019, with reformist President Mauricio Macri running for reelection. Currency and equity markets were spooked by a heavy defeat for Macri in the August primary election, which was won by populist rival Alberto Fernandez whose running mate is former President Cristina Kirchner.

This result puts in serious doubt Macri’s ability to win the election in October and continue with his reform agenda and market‑friendly policies. If Macri manages to recover, this would be a positive catalyst for the asset class, as he is highly likely to continue his program of broad‑based fiscal adjustment. But the specter of default risk is likely to weigh heavily on Argentine assets until the election plays out.

Nigeria, meanwhile, went to the polls in February. Incumbent President Muhammadu Buhari of the All Progressives Congress ran against former Vice President Atiku Abubakar of the People’s Democratic Party, winning with 56% of votes. With the country emerging from recession, economic policies are crucial. The continuity of leadership is a positive for the country, and recent economic indicators have been encouraging, including the naira attaining a more appropriate valuation, the minimum wage increasing, and both oil and non‑oil sectors making gains. From here, we watch for a stronger government focus on economics and the convergence to one exchange rate. Investors would likely welcome efforts to deliver market‑driven policies and the introduction of measures to boost domestic business and investment.

"Argentina’s reform agenda and market‑friendly policies are at stake in the October presidential election."— Oliver Bell

Portfolio Manager, Frontier Markets Equity Fund

MSCI Reclassifications

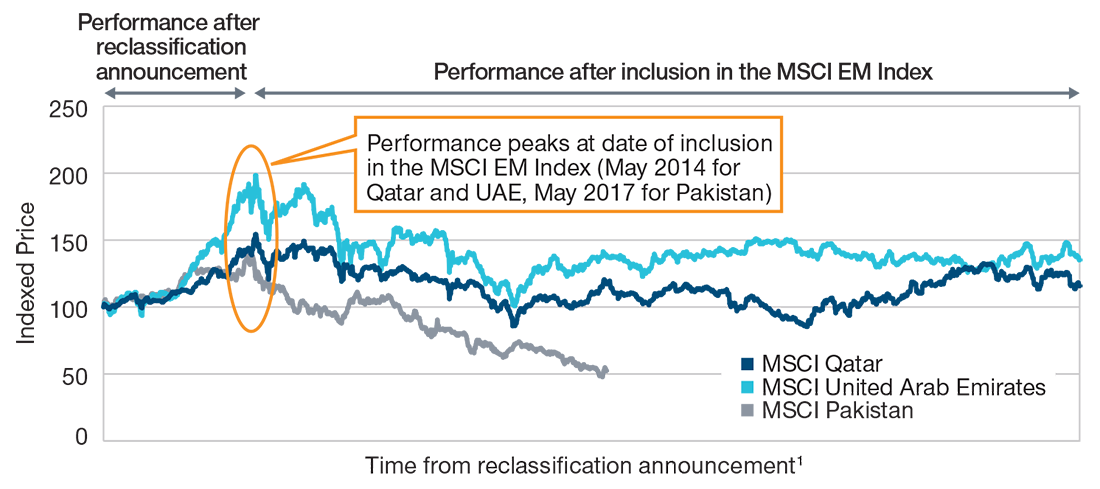

Countries shifting from the frontier to the emerging markets universe typically attract inflows ahead of index inclusion, as we have seen in the case of Qatar, the United Arab Emirates, and Pakistan in the past (see Figure 2).

Argentina was included in May 2019 and Saudi Arabia began a two‑phase inclusion, commencing in May and due for completion in August. Kuwait, which has already been upgraded by index provider FTSE, is due to be reviewed midyear by MSCI (for inclusion in 2020) and looks set to meet the criteria for inclusion.

(FIG. 2) CATCHING THE RECLASSIFICATION RALLY

Markets have tended to rally into index inclusion.

Past performance is not a reliable indicator of future performance.

Sources: MSCI via FactSet (see Additional Disclosures).

Data for illustrative purposes only.

Markets that are upgraded are typically subject to significant inflows ahead of inclusion, as passive fund investors look to fill quotas in accordance with the new weightings. This tends to benefit existing investors, and our approach is to gain exposure to this trend and gradually reduce our holdings after index inclusion if valuations have become too stretched through the process.

Of course, fundamentals must still be to be taken into account when determining the right level of exposure. Developments, such as those seen in Argentina recently, represent a stronger driver of performance than flows.

Geopolitical and Trade Developments

Investors are closely watching the ongoing trade tensions between the U.S. and China. A bout of volatility hit global markets in early August, following new tariff impositions by the U.S. Retaliatory currency depreciation by China raised the prospect of a currency war to accompany the trade impasse. If these tensions ease and negotiators are able to secure a trade deal, investor risk appetite should pick up, benefiting frontier markets.

Oct. 2019

Argentina set for crucial presidential election with reformist incumbent Macri up against populist rivals.

Meanwhile, countries such as Vietnam and Bangladesh, because of their role in the global supply chain, stand to benefit from ongoing tensions, as companies look to shift production away from China and are attracted by the cheap labor on offer. Vietnam, for its size, is disproportionately geared into the global economic cycle due to its large export market.

(FIG. 3) WHAT TO WATCH IN FRONTIER MARKETS

Key election, MSCI reclassifications, and geopolitical events.

Conclusion

Our bottom‑up stock selection has been guided by these catalysts, and we are well positioned in key areas should they come to have an impact. Maintaining a diversified portfolio helps in this regard. Investors should keep short‑term market volatility in perspective when compared with long‑term market results. Seeking to “time” equity markets in this environment will be very difficult. We believe selectivity is more likely to deliver durable returns during difficult periods.

In our view, the outlook for frontier markets should continue to improve as several of the country‑level developments weighing on markets resolve. With much of this already reflected in asset prices, markets are potentially primed for an improvement in sentiment as elections, MSCI reclassifications, and trade and geopolitical developments play out over the year.

WHAT WE’RE WATCHING NEXT

Against this backdrop, we are more favorable to Saudi Arabia (off benchmark), Sri Lanka, Vietnam, and Kuwait. On a sector basis, we are finding attractive investment opportunities in cheaply valued banks and consumer‑oriented stocks that benefit from favorable population dynamics in frontier markets.

Additional Disclosures

Financial data and analytics provider FactSet. Copyright 2019 FactSet. All Rights Reserved.

MSCI and its affiliates and third‑party sources and providers (collectively, “MSCI”) makes no express or implied warranties or representations and shall have no liability whatsoever with respect to any MSCI data contained herein. The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed, or produced by MSCI. Historical MSCI data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast or prediction. None of the MSCI data is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such.

Important Information

This material is provided for informational purposes only and is not intended to be investment advice or a recommendation to take any particular investment action.

The views contained herein are those of the authors as of August 2019 and are subject to change without notice; these views may differ from those of other T. Rowe Price associates.

This information is not intended to reflect a current or past recommendation, investment advice of any kind, or a solicitation of an offer to buy or sell any securities or investment services. The opinions and commentary provided do not take into account the investment objectives or financial situation of any particular investor or class of investor. Investors will need to consider their own circumstances before making an investment decision.

Information contained herein is based upon sources we consider to be reliable; we do not, however, guarantee its accuracy.

Past performance is not a reliable indicator of future performance. All investments are subject to market risk, including the possible loss of principal. All charts and tables are shown for illustrative purposes only.

T. Rowe Price Investment Services, Inc.

© 2019 T. Rowe Price. All rights reserved. T. Rowe Price, INVEST WITH CONFIDENCE, and the Bighorn Sheep design are, collectively and/or apart, trademarks of T. Rowe Price Group, Inc.

Weekly Investment Commentary: Earnings season: investment ideas

First-quarter earnings season has kicked off with the utilities and communication services sectors projected to deliver the strongest year-over-year EPS growth, while estimates for materials and energy are expected to decline the most.

Global Weekly Commentary: Earnings growth not just about tech

Solid U.S. economic and corporate earnings growth have supported risk appetite, driving stocks to all-time highs – even as bond yields have jumped. We think earnings will need to deliver on high expectations, especially after last week’s data showing sticky inflation spooked investors.

Global Markets Weekly Update: April 12, 2024

Review the performance of global stock and bond markets over the past week, along with relevant insights from T. Rowe Price economists and investment professionals.