Ten Lessons From Ten Years

KEY INSIGHTS

- While the current global market environment is undoubtedly extreme, it does not require any fundamental shifts in investor behavior, in our view.

- Although markets are cyclical, the primary forces that drive asset prices—greed and fear—are timeless.

- We believe that disciplined portfolio managers who follow a sound and repeatable investment process still can add value for their clients across market cycles.

Now that we have passed the 10‑year anniversary1 of the launch of the International Disciplined Equity Fund (IDE), I have been reflecting on the journey so far and what I have learned from it—lessons that I think are highly relevant to investing today.

Although the denizens of every age have viewed their era as unique and different from the past, the truth is that we do not live in exceptional times. We are not special; our era is not special. I believe the primary forces that drive financial asset prices—greed and fear—are timeless. Although the particular stock, commodity, or asset class in question may change, and the specific reasons why bull markets begin and end may change, we will always have overvaluations and bubbles, followed by corrections, fear, and, in some cases, recession.

While the current global investment environment is undoubtedly extreme—featuring historically low bond yields, interest rates at or near zero, record fiscal and monetary stimulus, and high debt—in my view, these are only factors that need to be considered, not monumental shifts in investor behavior or how stocks are valued.

I believe that prudent portfolio managers who understand these timeless realities of investing can add value for their clients across market cycles. But having a sound and repeatable investment process is critical. In that sense, investing is like boxing in many ways. We have to bob and weave, doing our best to avoid punches, while taking our shots at attractive opportunities if and when they appear.

To box effectively, one must have stamina. Likewise, markets may threaten to wear us out, forcing us to “go the distance” when we would very much like the fight to be over. But, by sticking to our strengths and jabbing until we see an opening, I believe skilled investors can take advantage of their opponent’s weaknesses—the cyclical extremes of greed and fear that seem to be inherent in market behavior.

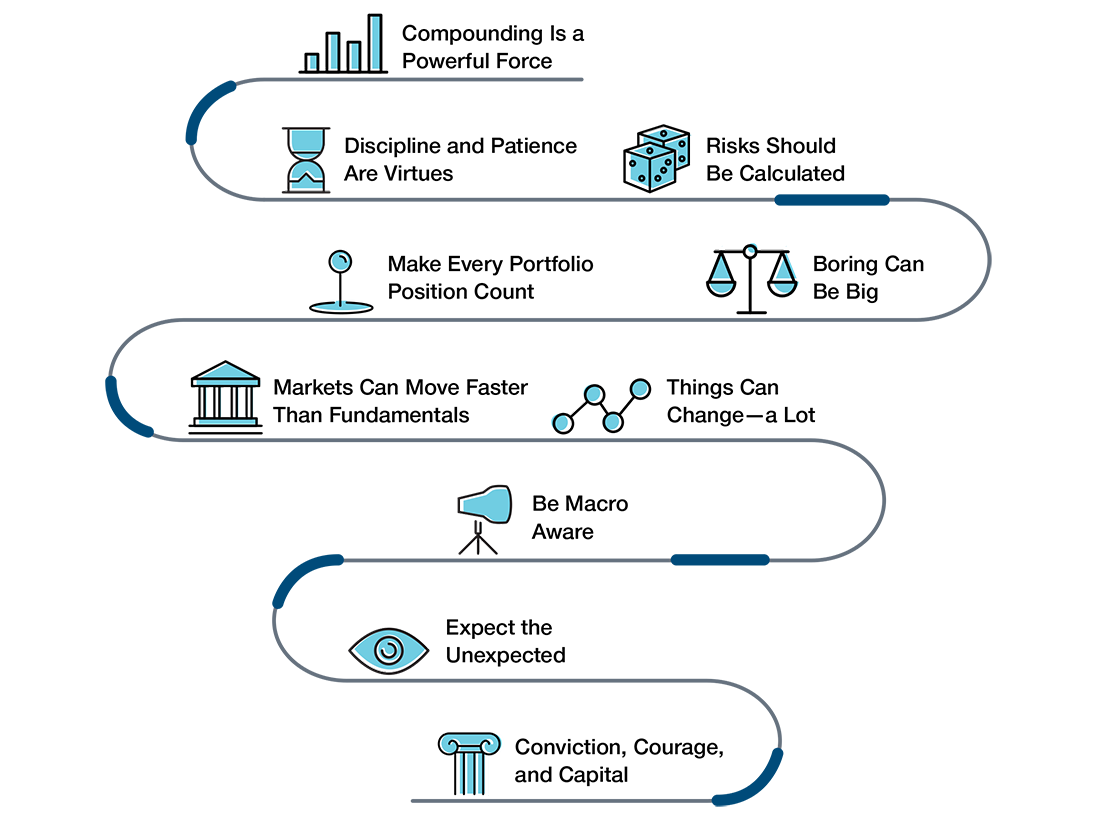

(Fig. 1) Ten key thoughts for international equity investors

And so I offer these 10 thoughts for investors to consider, distilled from my experience over the past 10 years of managing the IDE.

1. Compounding Is a Powerful Force

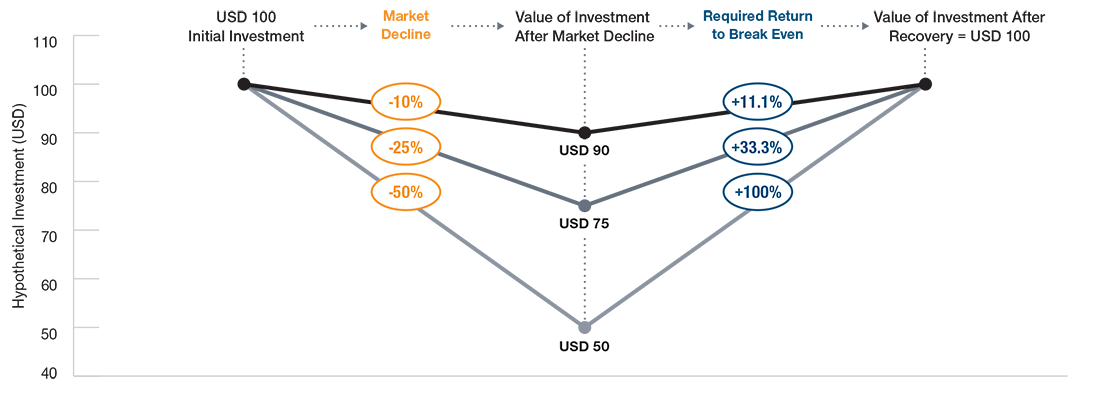

This is a simple concept, often overlooked in periods when returns have been consistently strong but highly relevant when markets turn volatile. For any given percentage loss suffered in a market decline, an even larger percentage gain is required to get back to even. In my view, the best defense against this math is to focus on quality companies—those that typically have exhibited positive returns across past market cycles, with durable free cash flows and histories of strong corporate governance and featuring relatively attractive valuations. I believe investing in such companies may help to mitigate losses in market drawdowns, thus potentially letting compounding work toward long‑term portfolio growth, not against it (Figure 2).

2. Discipline and Patience Are Virtues

Being an investor does not always mean your only choice is what to buy, but also when to buy. Sometimes, the best investment is in time and patience. Executing the analysis and identifying attractive companies is half the battle. Buying at the right price is the other half. The key to seeking potential alpha (i.e., excess returns), in our view, is getting in at a low entry price. Investors should stay patient, find the right entry point, and let their entry price do the heavy lifting from there.

3. Risks Should Be Calculated

Skilled active management means taking calculated risks, as the potential to generate excess returns above benchmarks and peer manager averages typically requires a willingness to be different. While no investor will get every call correct, a sound, repeatable, and tested process should build confidence, which is the foundation needed to take the right risk at the right time and to stick with a contrarian view even when the market is temporarily moving the other way.

4. Boring Can Be Big

Looking at the IDE’s best‑performing stocks over the past decade, I’m struck by how many of them could be considered “run‑of‑the mill” names in the telecommunications, financials, and consumer sectors. They could even be described as boring. What separated them from their peers, in our view, was that we saw them as predictable businesses with durable cash flows, and we were able to obtain them at attractive entry prices—creating a potentially attractive risk/reward profile. At the end of the day, investing is about risk‑adjusted performance, not how exciting a business story sounds.

THE POTENTIAL BENEFITS OF DOWNSIDE RISK MANAGEMENT

(Fig. 2) The greater the downside, the greater the required upside to break even

5. Make Every Portfolio Position Count

Investing isn’t just about owning the right stock, but also owning enough of it. It’s not just about avoiding mistakes, but not compounding a mistake by throwing good money after bad. When investors have conviction, that should be reflected in their portfolios—big bets potentially can lead to big returns. But if conviction has waned and the risk/reward profile supports only a small position, it would be better to utilize that capital elsewhere.

6. Markets Can Move Faster Than Fundamentals

Market valuations—such as price/earnings ratios—tend to move quickly, often much faster than company fundamentals. Over the long term, prices should reflect fundamentals, not narratives. Investors should be prepared to retest their thesis and trade accordingly. The emphasis should be on managing to risk/return potential, not to holding periods.

7. Things Can Change—a Lot

There is a natural human tendency to extrapolate. Investors tend to draw straight lines into the future, and this is an oversimplification. It’s not wise to assume that what has worked in the past will always work or that what has not worked will never work in the future. Doing so potentially means missed opportunities. Every era will have its unique characteristics—the most recent decade was all about growth, technology, and momentum, for example—but investors shouldn’t let long‑standing trends blind them to the potential for changes in market leadership.

8. Be Macro Aware

Security selection can drive potentially sustainable returns, but understanding the macroeconomic environment can be a powerful ally for stock pickers. For example, the structural decline of global interest rates has been a key factor behind the IDE’s underweight to banks in recent years. Staying macro aware doesn’t require a change in process, but it does suggest tweaking the analysis to account for the macro environment. Stocks do not operate in a bubble, and excellent companies still can find themselves in the wrong place at the wrong time.

9. Expect the Unexpected

“Black swans”—unexpected events that cannot be forecast—are more common that we think. Just over the past 10 years, we’ve seen a major tsunami, Brexit, unprecedented central bank policies, and a global pandemic. Investors need to embrace the possibility that unforeseen events might create losses. Investors need to understand the risk exposures—both direct and indirect—of the businesses they own and anticipate not just the potential upside but the potential downside as well.

10. Conviction, Courage, and Capital

Investors need to have conviction in their investment process, the courage to act on it, and the capital to see their strategy through. The capital issue is often overlooked. Whether it means establishing close partnerships with clients, or keeping dry powder to act quickly when markets move, access to capital is a key component to successful investing.

Conclusions

Over the last 10 years I have sought to apply these lessons in managing the IDE fund. Our fund first seeks to grow capital. That is done through investing in what we believe are quality companies, purchased at attractive valuations, across styles, countries, and market capitalizations.

The risk/reward relationship is incorporated in every step of our portfolio construction process, from security analysis and selection to macro awareness. We seek to utilize a highly disciplined approach to position sizing in a relatively limited number of names with the goal of driving alpha from stock selection.

Equity markets have experienced a lot since the launch of the IDE, but we believe the next decade is likely to be different from a market regime perspective. If we look back at history, it has not been often that the same trade has worked for much longer than a 10‑year period. Growth and technology have led the way over the past decade; perhaps something else will take their place in the coming one. Perhaps it will be value. After an extended period of disinflation or even outright deflation, perhaps inflation will accelerate.

Whatever happens, we resist the temptation to view market conditions as “extraordinary”—requiring a new investment approach that isn’t grounded in business or economic fundamentals. We will stay true to our style and process and, above all, remain disciplined.

1 The Institutional International Disciplined Equity Fund (formerly the Institutional International Concentrated Equity Fund) was launched on July 27, 2010. The version of the fund available to U.S. individual investors (International Disciplined Equity Fund) was launched on August 22, 2014.

Important Information

Call 1-800-225-5132 to request a prospectus or summary prospectus; each includes investment objectives, risks, fees, expenses, and other information you should read and consider carefully before investing.

This material is provided for informational purposes only and is not intended to be investment advice or a recommendation to take any particular investment action.

The views contained herein are those of the authors as of October 2020 and are subject to change without notice; these views may differ from those of other T. Rowe Price associates.

This information is not intended to reflect a current or past recommendation concerning investments, investment strategies, or account types, advice of any kind, or a solicitation of an offer to buy or sell any securities or investment services. The opinions and commentary provided do not take into account the investment objectives or financial situation of any particular investor or class of investor. Please consider your own circumstances before making an investment decision.

Information contained herein is based upon sources we consider to be reliable; we do not, however, guarantee its accuracy.

Past performance is not a reliable indicator of future performance. All investments are subject to market risk, including the possible loss of principal. The fund is “nondiversified,” meaning it may invest a greater portion of its assets in a single company and own more of the company’s voting securities than is permissible for a “diversified” fund. The fund’s share price can be expected to fluctuate more than that of a comparable diversified fund. International investments can be riskier than U.S. investments due to the adverse effects of currency exchange rates, differences in market structure and liquidity, as well as specific country, regional, and economic developments. All charts and tables are shown for illustrative purposes only.

T. Rowe Price Investment Services, Inc.

© 2020 T. Rowe Price. All rights reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE, and the bighorn sheep design are, collectively and/or apart, trademarks or registered trademarks of T. Rowe Price Group, Inc.

Peeling back the onion: A concentric approach to investment decision making

Portfolio Managers Greg Wilensky and Jeremiah Buckley offer a framework for interpreting economic news for investment decision making.

What is ESG and why do we care?

Michelle Dunstan, Janus Henderson’s Chief Responsibility Officer, explores ESG considerations and highlights how ESG integration helps Janus Henderson deliver on client goals and aspirations.

Hiding in plain sight: The investment case for healthcare

Though healthcare may have flown under the market’s radar this year, the sector’s attractive valuations and new growth opportunities are not to be overlooked, say Portfolio Managers Andy Acker and Dan Lyons.