Rate Angst

OUTLOOK

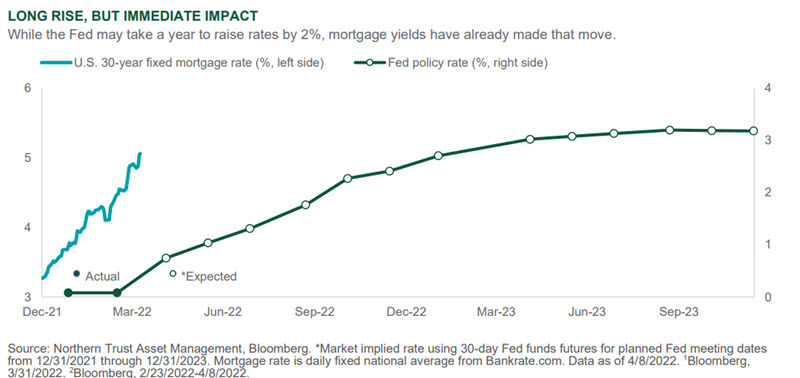

The U.S. bond market just exited its worst quarter in years, with Treasuries down 5.6%, corporate bonds down 7.4% and a broad municipal bond index down 6.2%.1After shaking off the rise in inflation in 2021, a swing in the outlook for Federal Reserve policy led to a jump in interest rates this year with the 10-year Treasury yield increasing from 1.51% to 2.71% currently. The Fed entered this year only expecting to hike rates three times, leading to a year-end Fed funds rate below 1.00%. The persistence of high inflation has now led the market to price in nearly 10 hikes with a Fed Funds rate over 2% by year-end. Central banks seek to tighten financial conditions to slow growth and therefore hopefully inflation – and as shown below 30-year mortgage rates have jumped from ~3.3% at the start of the year to 5.0% currently. That should likely lead to some eventual cooling in the pace of housing price rises.

Unfortunately, the war in Ukraine remains a core risk as the humanitarian crisis continues and signs of war atrocities are rising. This is only increasing the resolve of the West, which boosts momentum toward further Russian sanctions. Major supply shocks are in some respects still to unfold, but as shown by the 20% rise in wheat prices since February 23rd markets are reflecting the perceived eventual impacts.2 Further military escalation remains a risk case, with the potential for the use of unconventional weapons or further geographic incursions. Our base case scenario envisions a long, drawn-out affair without clear resolution.

In the wake of persistent inflation, the Ukraine war, and lingering COVID problems, global growth is slowing. Europe is at risk of recession, and China is suffering from the effects of COVID-related shutdowns. U.S. growth is holding up relatively better, and nominal growth in the second quarter could hit 10%. A risk case for us is the global slowdown leaking into the U.S., leading to disappointing growth. Nevertheless, U.S. growth looks better insulated than Europe or China and we resultingly favor U.S. equities over developed ex-U.S. and emerging market stocks. We also continue to favor natural resources equities, which have provided significant benefit to portfolios this year as commodities are benefitting from shortages and inflation concerns. Finally, we continue to like high yield bonds due to their attractive yield and strong fundamentals. The sharp tightening of credit spreads over the last month should give some comfort to those worried that an inversion of the yield curve is a certain sign about impending recession.

INTEREST RATES

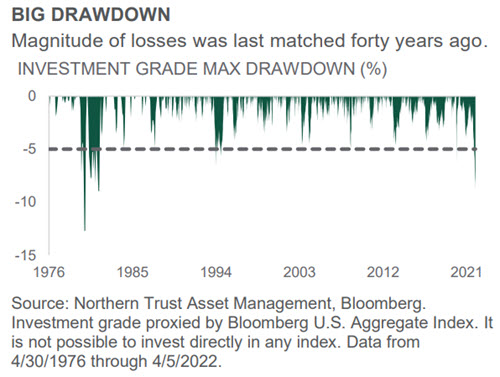

- The length of the current drawdown in bonds is nearly historic.

- There is unusual uncertainty about near-term fixed income returns.

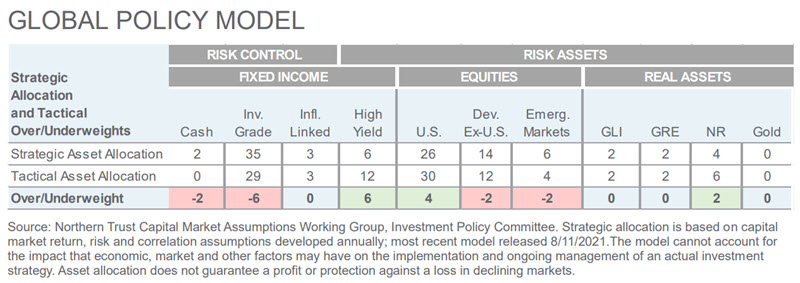

- We remain underweight fixed income in our global policy model.

Currently at around -9%, the current investment grade drawdown is one of the largest ones since the late 1970’s/early 1980’s when Paul Volcker’s Fed was fighting inflation with all hands on deck (~13% drawdown). The current drawdown is the longest on record, going on 20 months versus an average drawdown period of eight months. Historically, drawdowns have been shallower because current yield helped compensate the duration loss. For example, the investment grade yield during the Volcker years was about 13-16%. During the 1994 drawdown it was 7%. Today the yield is around 3%.

We are currently forecasting a return of 4.4% for investment grade. If our interest rate and credit forecasts are 50 basis points (bps) too low, the return would be 0%. If we rally 50 basis points below our targets then the return should be nearly 9%. The yet-to-be-determined Fed terminal rate (the market is currently projecting nearly 3%) will likely face an also yet-to-be-seen neutral rate (the rate where the economy starts to tighten). The current FOMC projection is 2.38%. The economy of course may evolve unexpectedly. We will continue to monitor economic data closely for signs of market rates affecting the consumer, along with the myriad of other forces at play.

CREDIT MARKETS

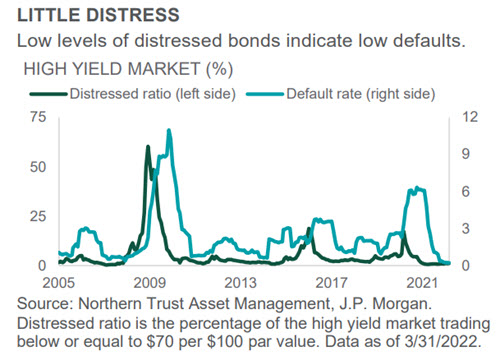

- Fundamental outlook for high yield looks good with low default levels expected.

- Companies have actively refinanced, so current maturities are relatively low.

- With a current yield of 6.3% and little interest rate sensitivity, high yield remains attractive.

With heightened volatility amid concerns of the Russian invasion of Ukraine, elevated oil prices, rapidly rising inflation, COVID-19, an inverted yield curve and uncertainty surrounding the Fed policy path, the economic growth outlook is in question. High yield relies heavily on underlying fundamentals and prospects for growth. The historically low distressed ratio indicates that market participants remain constructive on fundamentals (see chart). Moreover, the distressed ratio is considered a leading indicator for future default rates, and thus its current level is a positive signal that defaults are expected to remain near historic lows. One factor influencing the distressed ratio is the current maturity wall through 2023 is only $95B. This compares to refinancing volumes of $20B year-to-date and $290B in 2021.3

With rates and spreads near historic lows over the past two years, companies have been opportunistically refinancing near-term maturities to improve their balance sheets and reduce interest costs. Extended maturity profiles offer a cushion for companies to manage through heightened economic uncertainty over the near term. Given strong underlying fundamentals, high yield looks attractive on a yield basis at current levels.

3Bloomberg, 2/23/2022 - 4/8/2022

EQUITIES

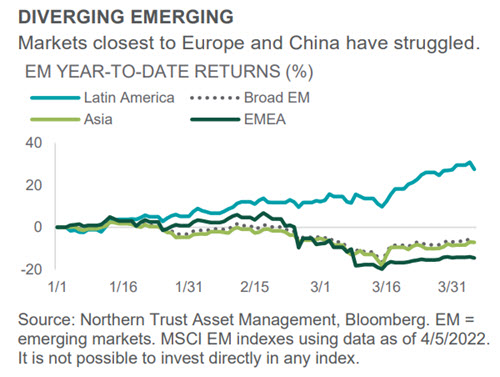

- The Ukraine war and China COVID issues have hit the EMEA and Asian markets hardest.

- Commodity-sensitive Latin American markets have performed strongly.

- We favor U.S. over non-U.S. equities due to greater confidence in the economic outlook.

Global equities bounced back from the previous month’s war-induced selloff, rising 6.7% for the month.4 The start of ceasefire negotiations combined with clear signs that Russia’s military advance has stalled came as a relief to investors. Europe, which had been most affected by the previous selloff, also recovered the most, rising more than 10%. U.S. equities rose more than 6% while EM lagged with a rise of 1.7%.4 Within EM the impact of the crisis in Ukraine and the associated worries around energy supply are visible in the underperformance of the EMEA part of the index, whereas the more commodity-sensitive Latin America part of the index did very well (see chart). However, the much larger Asia part of the index also struggled – and not just because of higher commodity prices. A rise in COVID-19 cases (now spreading into mainland China) dampened investor sentiment. With China still holding onto its zero-COVID policy, the amount of economic disruption from restrictions and regional lockdowns is rising and likely to continue to climb.

Given risk associated with the conflict in Ukraine and China’s zero-COVID policy, we maintained underweights across non-U.S. equities in the global policy model. We remain overweight the more insulated U.S. equities.

REAL ASSETS

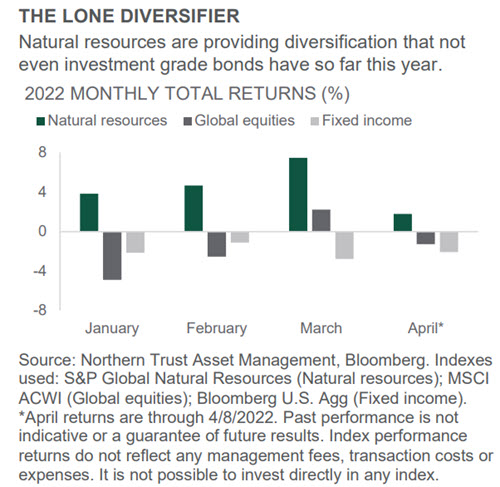

- Natural resources (NR) have been providing the trifecta of diversification, returns and income.

- Continued high commodity prices can mean continued returns and elevated dividend yields.

- We remain tactically overweight NR in the global policy model.

Natural resources (NR) have been a valuable component in a multi-asset portfolio thus far in 2022, providing diversification, returns and income. First on diversification, NR have done what investment grade bonds (IG) have not been able to so far this year – go up when broader equities are going down. As seen in the chart, while global equity returns have been spotty, IG returns have been worse – leaving NR to serve as the ballast to the portfolio. We defended that NR’s previous underperformance – driven by low inflation – was allowing the rest of the portfolio (both equity and fixed income) to do well. Now that the shoe is on the other foot (and geopolitical tensions are high), NR is making up for lost time – and lost performance.

That performance has been strong. NR is up over 18%, year to date, versus the -6% return out of global equities and -8% from IG.5 Less appreciated, NR has provided notable income of late. Given high commodity prices and management’s desire to return those cash flows to shareholders, dividend yields – at over 3% – are actually higher than those from “cash flow” assets (real estate/listed infrastructure). So long as commodity prices remain high (seemingly a good bet), NR remains attractive – and we remain tactically overweight in the global policy model.

4Bloomberg, 4/4/2022, 5Bloomberg, 4/8/2022

- Jim McDonald, Chief Investment Strategist

IN EMEA AND APAC, THIS PUBLICATION IS NOT INTENDED FOR RETAIL CLIENTS

© 2022 Northern Trust Corporation.

The information contained herein is intended for use with current or prospective clients of Northern Trust Investments, Inc. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. This information is obtained from sources believed to be reliable, and its accuracy and completeness are not guaranteed. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor. Forward-looking statements and assumptions are Northern Trust's current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information. Investments can go down as well as up.

Northern Trust Asset Management is composed of Northern Trust Investments, Inc., Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K., NT Global Advisors, Inc., 50 South Capital Advisors, LLC, Belvedere Advisors LLC and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company.

Issued in the United Kingdom by Northern Trust Global Investments Limited.

Weekly Investment Commentary: Earnings season: investment ideas

First-quarter earnings season has kicked off with the utilities and communication services sectors projected to deliver the strongest year-over-year EPS growth, while estimates for materials and energy are expected to decline the most.

Global Weekly Commentary: Earnings growth not just about tech

Solid U.S. economic and corporate earnings growth have supported risk appetite, driving stocks to all-time highs – even as bond yields have jumped. We think earnings will need to deliver on high expectations, especially after last week’s data showing sticky inflation spooked investors.

Global Markets Weekly Update: April 12, 2024

Review the performance of global stock and bond markets over the past week, along with relevant insights from T. Rowe Price economists and investment professionals.