The More Things Change...

Key Takeaways

- The overall economic backdrop remains healthy as illustrated by a continued green signal for the ClearBridge Recession Risk Dashboard, despite softer Retail Sales and consumer confidence.

- A strong print for ISM Manufacturing New Orders and positive signals from several other ISM sub-components suggest building optimism as we enter fall.

- The disappointing August jobs report was primarily due to the impact of the Delta variant on leisure and hospitality employment but sets up the potential for a goldilocks scenario with the Federal Reserve on hold longer, and a possible economic reacceleration as Delta subsides.

Economy and Markets Continue to Defy Wall of Worry

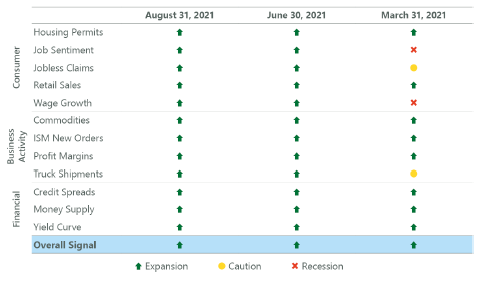

With fall upon us, change is in the air. The days are getting shorter, the mornings chillier, and back-to-school has arrived. However, the more things change, they more they stay the same. The ClearBridge Recession Risk Dashboard continues to emanate an overall green expansionary signal, with no changes this month meaning all 12 underlying indicators remain green. In fact, more signals saw improvement beneath the surface than deterioration over the last month, meaning the overall reading continues to improve from a very strong starting point.

Exhibit 1: ClearBridge Recession Risk Dashboard

Another thing that hasn’t changed is market and macro fear and risk. Some market observers are worried about an economic soft patch in the coming months. This week expanded unemployment insurance (UI) benefits expire in the remaining 25 states that did not opt out early, impacting about 11 million individuals. Further, the rise in COVID-19 cases from the spread of the Delta variant has caused some individuals to retrench. This is evident in recent data with Retail Sales widely missing expectations although year-over-year (YoY) growth – which the dashboard focuses on – remains quite robust at +15.8%.

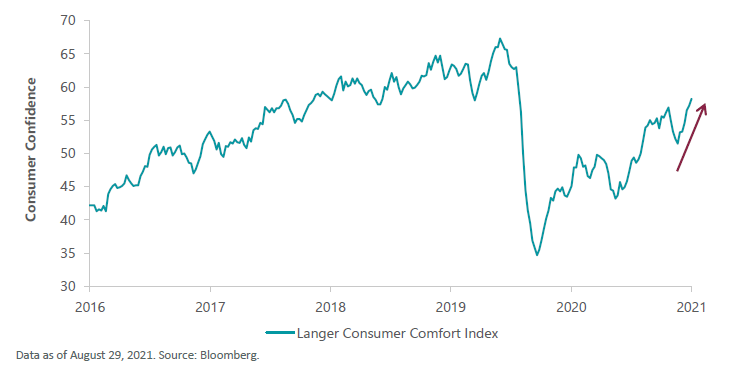

Another example is consumer confidence, which has plunged over the last two months. The dashboard’s Job Sentiment metric utilizes data contained within the Conference Board survey, specifically the differential between jobs “plentiful” and jobs “hard to get” responses, which held up much better, declining a meager 1.3 points from last month’s two-decade high. Importantly, the rapid decline in the headline metric could prove to be a contra-indicator. When consumer confidence has historically seen a decline equivalent or worse than the -15.1 points seen over the last two months, the S&P 500 Index has delivered a 12.9% return over the subsequent year. When looking at the six non-recessionary periods only – likely a more appropriate comparison given current economic conditions – the return is an even stronger 16.5% with all six periods delivering positive returns. Similarly encouraging is the rebound in the weekly Consumer Comfort Index which printed a new post-pandemic high last week.

Exhibit 2: Despite Recent Weakness, Consumer Confidence Could Prove Resilient

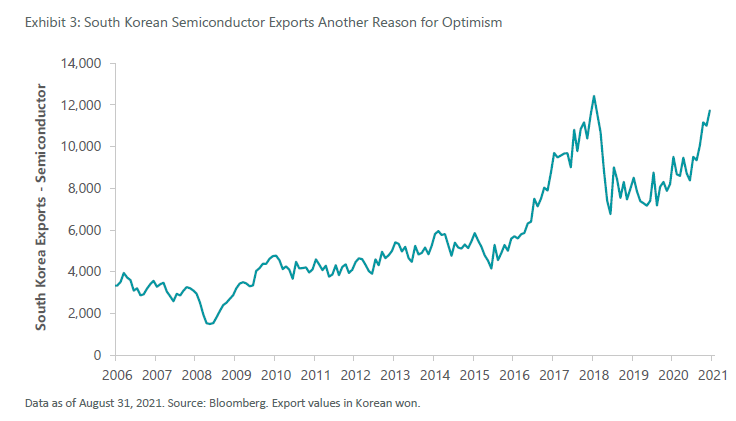

There are additional reasons to be optimistic as we move toward fall. The recent ISM Manufacturing release was very strong, with both the headline and New Orders (a dashboard component) beating expectations and accelerating from the prior month. Moreover, the prices paid subcomponent missed expectations and decelerated, a positive development that suggests inflation should continue to ease in the coming months and into 2022. While supply chain issues continue to persist, a bright spot is South Korean semiconductor exports which are up 40% YoY and 47% compared to August 2019 levels.

Exhibit 3: South Korean Semiconductor Exports Another Reason for Optimism

Furthermore, the backdrop of rising wages, increasing COVID-19 vaccination rates, and the aforementioned UI benefit expiration should support an increasing labor pool into fall despite last week’s jobs report miss. With a record 10 million job openings, labor supply appears to be the primary challenge currently facing the labor market, and the pool should expand as schools reopen given the higher rates of labor force exits among mothers in particular.

The jobs report miss was largely driven by weakness in the leisure and hospitality sector which gained zero jobs after averaging +284,000/month over the prior six months. This sector is particularly sensitive to COVID-19, making the peak in Delta particularly important. In fact, 400,000 additional workers reported they were “unable to work because their employer closed or lost business due to the pandemic” in August (5.6 million) relative to July (5.2 million) per the Bureau of Labor Statistics household survey supplemental data. Case counts appear to be growing at a slower pace and could peak soon – if the U.S. follows a similar trajectory to India and the U.K. – which would support a rebound in hiring.

The rapidly changing landscape in job creation means that the Federal Reserve’s “substantial further progress” barometer for the labor market has not yet been met. This development could push back the effective liftoff date for the upcoming tightening cycle (beginning with the tapering of quantitative easing). In the near term, this sets up the potential for a goldilocks scenario for equity investors with the Fed on hold for a bit longer and a possible economic reacceleration when Delta subsides. Even when the Fed eventually does begin to renormalize monetary policy away from extraordinary crisis measures, their overall stance will still remain quite accommodative, continuing to support the current bull market. The more things change, the more they stay the same.

About the Authors

Jeffrey Schulze, CFA

Director, Investment Strategist

• 16 years of investment industry experience

• Joined ClearBridge Investments in 2014

• BS in Finance from Rutgers University

Josh Jamner, CFA

Vice President, Investment Strategy Analyst

• 12 years of investment industry experience

• Joined ClearBridge Investments in 2017

• BA in Government from Colby College

Definitions

The ClearBridge Recession Risk Dashboard is a group of 12 indicators that examine the health of the U.S. economy and the likelihood of a downturn.

The S&P 500 Index is an unmanaged index of 500 stocks that is generally representative of the performance of larger companies in the U.S.

The Institute for Supply Management (ISM) is an association representing more than 48,000 purchasing and supply management professionals. It conducts regular surveys of purchasing and supply managers to determine industry trends.

IMPORTANT LEGAL INFORMATION

All investments involve risk, including possible loss of principal.

Past performance is no guarantee of future results. Please note that an investor cannot invest directly in an index. Unmanaged index returns do not reflect any fees, expenses or sales charges.

The value of investments and the income from them can go down as well as up and investors may not get back the amounts originally invested, and can be affected by changes in interest rates, in exchange rates, general market conditions, political, social and economic developments and other variable factors. Investment involves risks including but not limited to, possible delays in payments and loss of income or capital. Neither Franklin Resources, Inc. nor any of its affiliates guarantees any rate of return or the return of capital invested.

Equity securities are subject to price fluctuation and possible loss of principal. Fixed-income securities involve interest rate, credit, inflation and reinvestment risks; and possible loss of principal. As interest rates rise, the value of fixed income securities falls. International investments are subject to special risks including currency fluctuations, social, economic and political uncertainties, which could increase volatility. These risks are magnified in emerging markets.

Commodities and currencies contain heightened risk that include market, political, regulatory, and natural conditions and may not be suitable for all investors.

U.S. Treasuries are direct debt obligations issued and backed by the “full faith and credit” of the U.S. government. The U.S. government guarantees the principal and interest payments on U.S. Treasuries when the securities are held to maturity. Unlike U.S. Treasuries, debt securities issued by the federal agencies and instrumentalities and related investments may or may not be backed by the full faith and credit of the U.S. government. Even when the U.S. government guarantees principal and interest payments on securities, this guarantee does not apply to losses resulting from declines in the market value of these securities.

The opinions and views expressed herein are not intended to be relied upon as a prediction or forecast of actual future events or performance, guarantee of future results, recommendations or advice. Statements made in this material are not intended as buy or sell recommendations of any securities. Forward-looking statements are subject to uncertainties that could cause actual developments and results to differ materially from the expectations expressed. This information has been prepared from sources believed reliable but the accuracy and completeness of the information cannot be guaranteed. Information and opinions expressed by either Franklin Resources, Inc. or its affiliates are current as at the date indicated, are subject to change without notice, and do not take into account the particular investment objectives, financial situation or needs of individual investors.

The information in this material is confidential and proprietary and may not be used other than by the intended user. Neither Franklin Resources, Inc. or its affiliates or any of their officer or employee of Franklin Resources, Inc. accepts any liability whatsoever for any loss arising from any use of this material or its contents. This material may not be reproduced, distributed or published without prior written permission from Franklin Resources, Inc. Distribution of this material may be restricted in certain jurisdictions. Any persons coming into possession of this material should seek advice for details of, and observe such restrictions (if any).

This material may have been prepared by an advisor or entity affiliated with an entity mentioned below through common control and ownership by Franklin Resources, Inc. Unless otherwise noted the “$” (dollar sign) represents U.S. Dollars.

This material is approved for distribution in those countries and to those recipients listed below. Note: this material may not be available in all regions listed.

All investors and eligible counterparties in Europe, the UK, Switzerland:

In Europe (excluding UK and Switzerland), this financial promotion is issued by Legg Mason Investments (Ireland) Limited, registered office 6th Floor, Building Three, Number One Ballsbridge, 126 Pembroke Road, Ballsbridge, Dublin 4, D04 EP27. Registered in Ireland, Company No. 271887. Authorised and regulated by the Central Bank of Ireland.

All Qualified Investors in Switzerland: In Switzerland, this financial promotion is issued by Legg Mason Investments (Switzerland) GmbH. Investors in Switzerland: The representative in Switzerland is FIRST INDEPENDENT FUND SERVICES LTD., Klausstrasse 33, 8008 Zurich, Switzerland and the paying agent in Switzerland is NPB Neue Privat Bank AG, Limmatquai 1, 8024 Zurich, Switzerland. Copies of the Articles of Association, the Prospectus, the Key Investor Information documents and the annual and semi-annual reports of the Company may be obtained free of charge from the representative in Switzerland.

All investors in the UK: In the UK this financial promotion is issued by Legg Mason Investments (Europe) Limited, registered office 201 Bishopsgate, London EC2M 3AB. Registered in England and Wales, Company No. 1732037. Authorized and regulated by the Financial Conduct Authority. Client Services +44 (0)207 070 7444

All Investors in Hong Kong and Singapore:

This material is provided by Legg Mason Asset Management Hong Kong Limited in Hong Kong and Legg Mason Asset Management Singapore Pte. Limited (Registration Number (UEN): 200007942R) in Singapore.

This material has not been reviewed by any regulatory authority in Hong Kong or Singapore.

All Investors in the People's Republic of China ("PRC"):

This material is provided by Legg Mason Asset Management Hong Kong Limited to intended recipients in the PRC. The content of this document is only for Press or the PRC investors investing in the QDII Product offered by PRC's commercial bank in accordance with the regulation of China Banking Regulatory Commission. Investors should read the offering document prior to any subscription. Please seek advice from PRC's commercial banks and/or other professional advisors, if necessary. Please note that Legg Mason and its affiliates are the Managers of the offshore funds invested by QDII Products only. Legg Mason and its affiliates are not authorized by any regulatory authority to conduct business or investment activities in China.

This material has not been reviewed by any regulatory authority in the PRC.

Distributors and existing investors in Korea and Distributors in Taiwan:

This material is provided by Legg Mason Asset Management Hong Kong Limited to eligible recipients in Korea and by Legg Mason Investments (Taiwan) Limited (Registration Number: (109) Jin Guan Tou Gu Xin Zi Di 035; Address: Suite E, 55F, Taipei 101 Tower, 7, Xin Yi Road, Section 5, Taipei 110, Taiwan, R.O.C.; Tel: (886) 2-8722 1666) in Taiwan. Legg Mason Investments (Taiwan) Limited operates and manages its business independently.

This material has not been reviewed by any regulatory authority in Korea or Taiwan.

All Investors in the Americas:

This material is provided by Legg Mason Investor Services LLC, a U.S. registered Broker-Dealer, which includes Legg Mason Americas International. Legg Mason Investor Services, LLC, Member FINRA/SIPC.

All Investors in Australia and New Zealand:

This document is issued by Legg Mason Asset Management Australia Limited (ABN 76 004 835 839, AFSL 204827). The information in this document is of a general nature only and is not intended to be, and is not, a complete or definitive statement of matters described in it. It has not been prepared to take into account the investment objectives, financial objectives or particular needs of any particular person.

Forecasts are inherently limited and should not be relied upon as indicators of actual or future performance.

The aforementioned Legg Mason entities are wholly owned subsidiaries of Franklin Resources, Inc.

Copyright © 2021, Franklin Resources, Inc.

Weekly Investment Commentary: Earnings season: investment ideas

First-quarter earnings season has kicked off with the utilities and communication services sectors projected to deliver the strongest year-over-year EPS growth, while estimates for materials and energy are expected to decline the most.

Global Weekly Commentary: Earnings growth not just about tech

Solid U.S. economic and corporate earnings growth have supported risk appetite, driving stocks to all-time highs – even as bond yields have jumped. We think earnings will need to deliver on high expectations, especially after last week’s data showing sticky inflation spooked investors.

Global Markets Weekly Update: April 12, 2024

Review the performance of global stock and bond markets over the past week, along with relevant insights from T. Rowe Price economists and investment professionals.