MONEYBALL INVESTING: THE REAL REASON SWINGING FOR THE FENCES IS BAD FOR YOUR PORTFOLIO

One of the more iconic scenes in the movie, Moneyball, involves the baseball scouts discussing various players’ abilities. They note a player’s “classy” swing and then move on to his girlfriend’s looks for an assessment of his in-game proficiency. It’s both darkly humorous and a sly indictment of the flawed mechanics by which scouts judge players.

Now imagine those same people were picking stocks for your portfolio. It’s a scary thought. Because this is what you’d get:

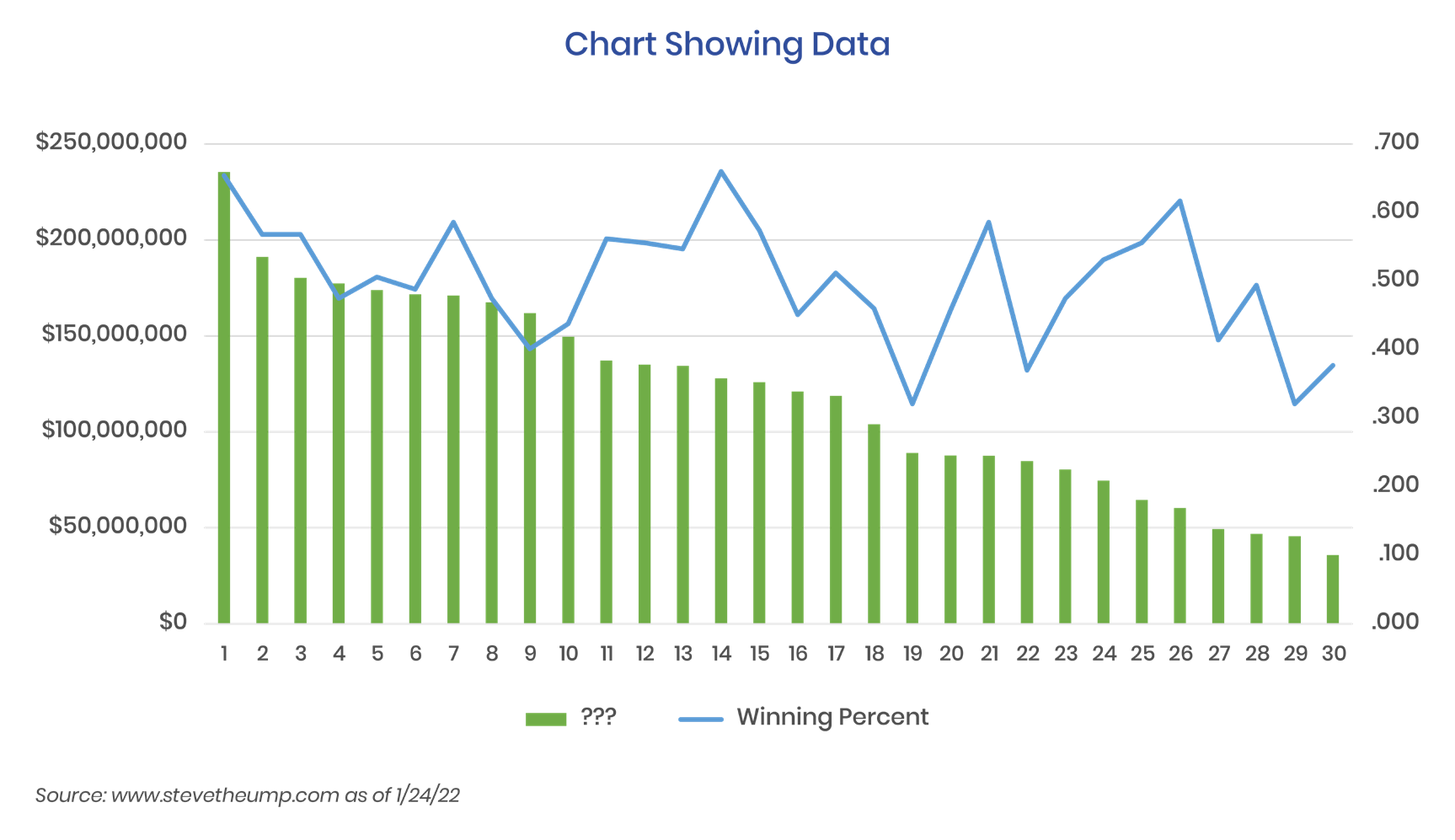

You’ll be forgiven if you thought this chart wasn’t terribly informative. Yet the dollar figures on the left axis attest to the sheer amount of money at risk. You see, the green bars represent the payrolls of the 30 Major League Baseball teams at the start of the 2021 season. Meanwhile, the blue line represents the respective clubs’ records. Most would agree that the correlation isn’t perfect, to say the least. (And if you’d prefer to quibble, please refer to the Note at the end for further discussion.)

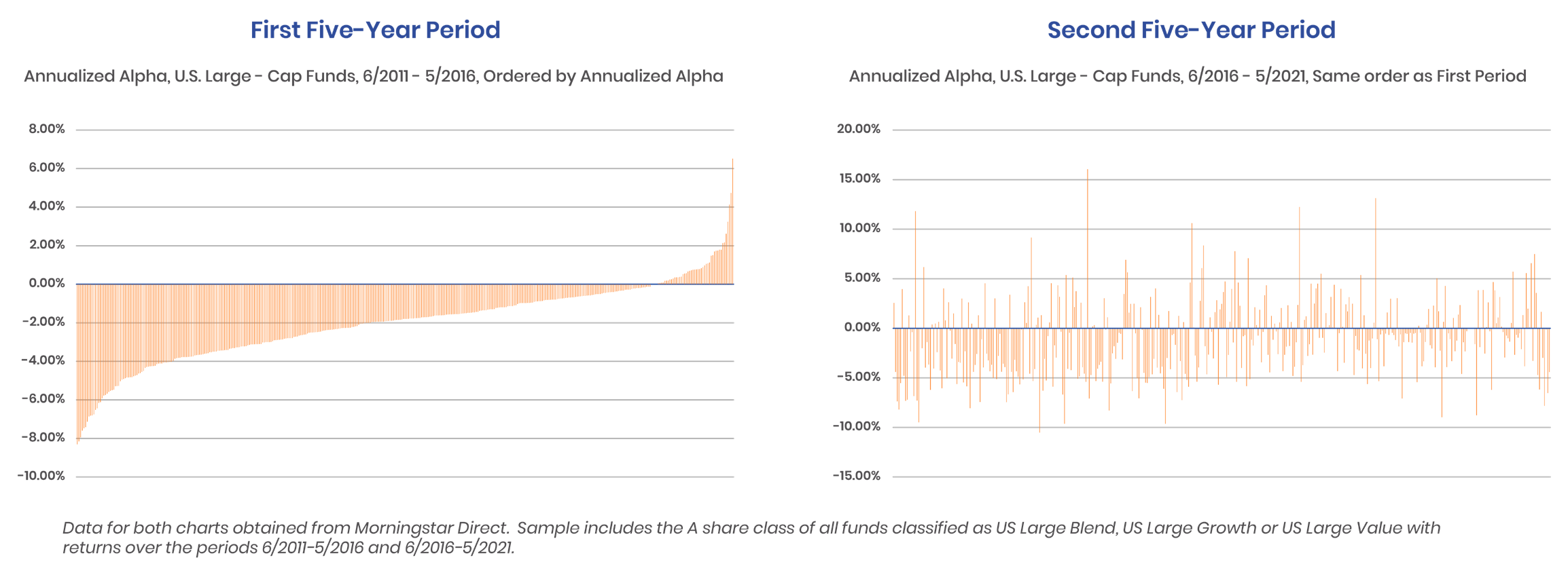

With this in mind, please review these two charts below:

The charts compare the total collection of U.S. Large Cap funds, ranked by annualized return, over one five-year period (6/2011-5/2016) vs. the ensuing five-year period (6/2016-5/2021). The chaos in the second chart is nearly as random as the lack of correlation between the MLB’s team payroll and winning percentage.

It’s as if those same scouts who picked players based on their girlfriend’s looks are the same portfolio managers picking investment funds based on previous fund performance. No longer a mere ‘scary thought,’ the similarity takes on frightening reality. Perhaps each should stop trying to pick winners altogether?

Picking Winners is a Loser’s Game

The truth is the people who run ball clubs are a lot like the people who run investment portfolios. They always think in terms of buying the big names in order to put together a winning team. And as you can see, this often leads to failure. We believe this is due to the failure of active stock selection and an imperfect understanding of where alpha comes from.

Billy Beane knew this. The Oakland A’s were struggling but their scouts were using traditional, outdated and ineffective methods to identify talent; it was the only way they knew how to evaluate talent. With a tiny payroll and a burning desire to win, he knew he needed to approach the problem differently. He decided to focus strictly on the data. Rather than attempting to predict the future of a player or buying superstars, he took human judgment out of the equation. Specifically, he focused on a player’s On-base Percentage. The result was revolutionary and the randomness of outcomes was reduced.

In investing, just like in baseball, we believe it’s all about getting things down to a number. Once you have that, you can reduce the vague and ambiguous information—you can avoid investment strikeouts and find value in stocks that many fail to see. The Oakland A’s exploited the On-base Percentage. At New Age Alpha we exploit The Human Factor.

Know the Number

The Human Factor measures the probability a company will fail to deliver the growth implied by the stock price. It’s New Age Alpha’s proprietary methodology designed to systematically measure the amount of vague and ambiguous information impounded into a stock’s price. By putting a number to this risk of human behavior—the Human-Factor—we believe we can measure it and avoid it. In this way, we believe we can produce a differentiated source of outperformance in any investment universe.

Just like baseball’s outdated scouting methods, active stock pickers have always attempted to guess market winners by forecasting the future. Such an approach is archaic, unsystematic, and unpredictable. We believe human behavior is the source from which all traditional risk metrics are born. Beta or PE Ratio do little; they are merely proxies for certain types of risk. If an investor hopes to avoid risk en totale, he or she must look at risk in an entirely new way. Put simply, rather than trying to pick winners, investors should aim to avoid the losers.

Note: Some may contend that there is a generalized successful trend among the top 10 or so teams. As an average, this is true: the top third teams by payroll averaged a W-L percentage of 0.516%, the middle averaged 0.510% and the bottom averaged 0.474%. But this general trend had little predictive power on the best teams overall. The Giants, with the most wins (107), ranked almost exactly in the middle with the 14th highest payroll. Meanwhile, the Dodgers managed the second-most wins (106) with the highest payroll, while the Rays attained the third-most wins (100) with the 26th overall payroll. And an amusing sidenote? The eventual World Series winner, the Braves, were right beside the Giants with the 13th highest payroll.

Yet this doesn’t even address the wild disparities between the Dodger’s highest payroll at $235 million and the lowest amount, $35 million, spent by the Pirates. Viewed relative to dollars invested, picking winners becomes even more perilous as one moves up the salary chain. If you applied the old techniques and used team salary as a guide for success, your top-third 0.516% winning percentage would’ve cost an average of $178 million. Meanwhile, the middle third’s 0.510% would’ve cost $118 and the bottom third’s 0.474% would’ve cost $63 million.

About Us

New Age Alpha is ushering in a new age of asset management by applying an actuarial-based approach to investment portfolios. Utilizing these principles built by the insurance industry, we construct portfolio solutions, indexes, and tools that aim to identify and avoid a mispricing risk caused by investor behavior. Embedding well-established principles of probability theory in our investment methodology, we construct solutions that aim to avoid overpriced stocks in a portfolio—losers. We combine the alpha potential of active management with the advantages of rules-based investing to build differentiated equity, fixed income and ESG-themed portfolios that drive long-term outperformance.

Disclosures

New Age Alpha refers to the New Age Alpha separate but affiliated entities, generally, rather than to one particular entity. These entities are New Age Alpha LLC and New Age Alpha Advisors, LLC (“New Age Alpha Advisors”). Investment advice is offered through New Age Alpha Advisors, LLC a wholly-owned subsidiary of New Age Alpha LLC. New Age Alpha Advisors is an investment advisor registered with the U.S. Securities and Exchange Commission. New Age Alpha Advisors, located in the State of New York, only transacts business in those states in which it is properly registered or qualifies for an applicable exemption or exclusion from such state’s registration requirements.

This material should not be construed as an offer to sell or the solicitation of an offer to buy any security. It is not possible to invest directly in an index. We are not soliciting any action based on this material. It is for general information purposes only. To the extent that it includes references to securities, these references do not constitute a recommendation to buy, sell or hold such security, the information may not be current, and it should not be read to suggest that it is an endorsement of New Age Alpha or its products or strategies. There is no intention for New Age Alpha to include any securities referenced herein, if any, in its portfolios unless they become part of the established universe of eligible securities that are part of each specific investment strategy.

Past performance is not indicative of future results. Current and future results may be lower or higher than those shown. Therefore, no current or prospective client should assume that the future performance of any specific investment, investment strategy (including the investments and/or investment strategies recommended and/or purchased by New Age Alpha), or an Index, product, or a referenced strategy, either directly or indirectly, in this material, will be profitable or equal to corresponding indicated performance levels.

Information contained herein and used in the analysis provided by New Age Alpha has been obtained from sources believed to be reliable, but not guaranteed. It has been prepared solely for informational purposes on an “as is” basis and New Age Alpha does not make any warranty or representation regarding the information. Investors should be aware of the risks associated with data sources and quantitative processes used in our investment management process. Errors may exist in data acquired from third-party vendors.

This overview is limited to providing general information about New Age Alpha and its investment advisory services. New Age Alpha’s specific advice is given only within the context of its contractual agreements with each client. Investment advice may only be rendered after the delivery of Form ADV Part 2 (an investment advisor’s disclosure document) and the execution of an investment agreement by the client and New Age Alpha. New Age Alpha’s Form ADV Part 2 and accompanying descriptions are available upon request.

Beware 'greenwashing'

Increasingly, managers are integrating environmental, social and governance (ESG) factors into their investment process and beginning to actively engage with companies.

Is your wholesaler your BESTIE?

Have you ever called your wholesaler when you realized late in the game of planning a client event that you need additional funding?

The six key components for choosing an index asset manager

Are all index asset managers the same? Learn what separates the best managers from the rest of the industry.