Investment Perspective: A Narrowed Path

OUTLOOK

Extraordinary volatility continues in financial markets as investors grapple with the outlook for inflation, monetary policy and the eventual economic impact. We experienced some welcome upside volatility in both stocks and bonds recently as consumer price inflation (CPI) finally delivered a positive surprise. Headline CPI fell from 8.2% in September to 7.7% in October – better than the 7.9% expectation. While this “beat” seems small, the 0.4% month-on-month change was nicely below the 0.6% expectation. While this improvement is certainly welcome, we caution that it is a single month of data. The drop was aided by declining energy and goods inflation, while services inflation levelled off.

The slowing global economy has aided recent inflation trends, as shown by a global composite of purchasing manager indexes – which are now in recession territory. Global short-rates have been increased dramatically this year, and they have a lagged impact on growth. Recognizing the (intended) negative impact on growth, Federal Reserve Chair Powell has acknowledged the U.S. economy has a “narrowed path” to achieve a soft landing. Meanwhile, other leading central banks including Australia and Canada have moderated their outlooks, and we now think the European Central Bank is likely to raise rates less than market expectations. This highlights our base case of Central Bank Divergence, where a relatively hawkish Fed continues to pressure currency markets globally. Sustainable improvement in the inflation outlook should, however, allow the Fed to pause once it gets the Fed funds rate to near the 5.0% market expectations – but we believe a pivot toward lower rates remains a long way off. As that transition starts to become more clear, investor focus will increasingly turn to the economic and earnings impact. This earnings season delivered the first negative revisions in some time, and our current forecast calls for modest U.S. earnings growth in 2023, with no earnings growth in emerging markets and modestly declining European earnings.

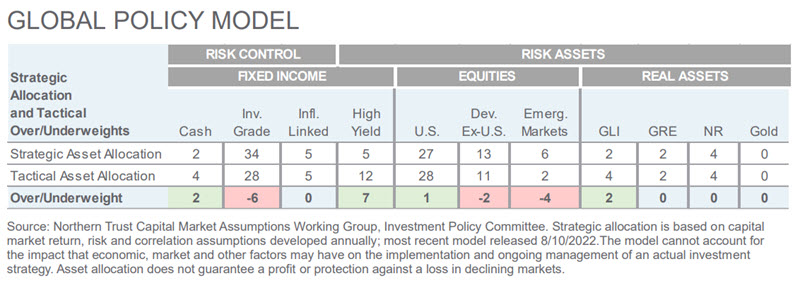

We made no changes in our global policy model (GPM) this month. While U.S. midterm election results are not finalized, divided government is the likely outcome, muting Washington’s impact on financial markets in 2023. Financial market volatility should remain high as global growth disappoints and monetary policy remains tight. In this environment, the GPM is underweight equities and investment grade bonds, while being overweight high yield bonds and modestly overweight cash.

With my pending retirement in February 2023, I am handing off responsibilities for Investment Perspectives to Chris Shipley – Chief Investment Strategist – North America, and Wouter Sturkenboom – Chief Investment Strategist – EMEA & APAC. I am confident that I am leaving the investment strategy effort in strong hands!

INTEREST RATES

-

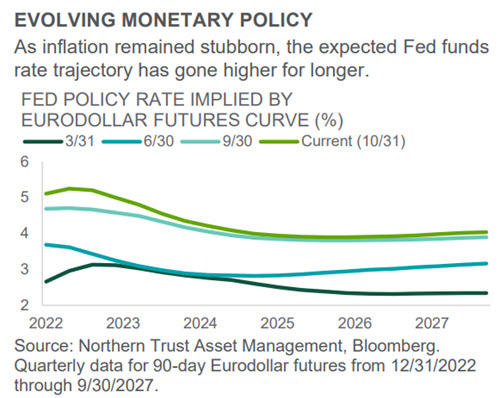

Market expectations for the Fed’s rate hike trajectory have moved higher throughout 2022.

-

The Fed will likely need a few months of softer inflation readings to signal mission accomplished.

-

We remain underweight term (interest rate) risk as we await more clarity on Fed intentions.

Investors can look to the Eurodollar futures curve for insight as to what is priced into the financial markets regarding future U.S. monetary policy. Throughout 2022, markets have marched policy rate expectations higher (see chart) as inflation has proved stickier than expected. Most of the variability has been in the near maturities, however expectations for the terminal policy rate level have moved much higher than both initially expected and experienced in the last fourteen years. The expectation that the Federal Reserve will hike rates, then pause and then be forced to cut has been a broadly consistent theme throughout this year. But the peak level and timing have been in dispute.

The Fed has begun talking about slowing the pace of hikes, which is only natural after 375 basis points of tightening in six months. Economic effects of the policy moves lag by an unknown amount of time, meaning policy-makers will likely need several months of convincing data before sounding the all-clear alarm. The fall from 8% to 5% year-over-year inflation should be much easier than the decline from 5% to the stated goal of 2%. We remain underweight investment grade fixed income as rate volatility may remain high while the Fed fights inflation.

CREDIT MARKETS

-

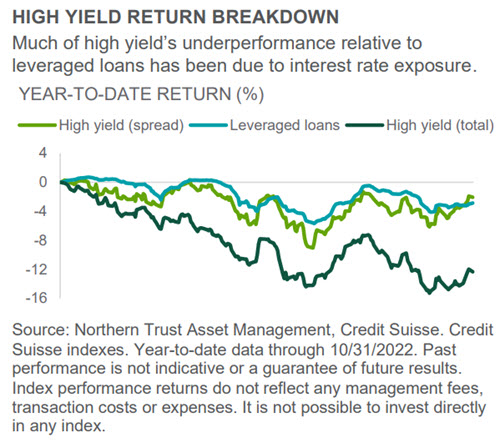

High yield has outperformed investment grade fixed income but underperformed leveraged loans.

-

The floating rate nature of leveraged loans has helped so far this year, but may start to pressure credit quality.

-

We continue to like high yield more than leveraged loans – as well as all other asset classes.

High interest rate volatility alongside elevated monetary policy uncertainty has been a major drag on high yield performance. To help mitigate concerns on rising rates, investors have turned to leveraged loans. To compare the performance of these floating-rate instruments and high yield, we look solely at the spread component of high yield returns. When removing duration impacts, high yield has outperformed leveraged loans year-to-date (see chart).

Moving forward, leveraged loans may be at a disadvantage relative to high yield if the Fed continues to tighten and credit quality concerns rise. High yield quality, which has risen significantly over the past decade, bests the quality of the leveraged loan universe (50% BB-rated versus 23% BB-rated or higher for leveraged loans). Moreover, while high yield bonds are fixed rate, leveraged loan issuers may be at risk of further pressure on financing costs depending on whether they hedged the floating rate aspect of loans. Additionally, the average price on the leveraged loan index is $93 versus an average price of $85 for high yield. This means investors should be able to move up in credit quality by swapping out of higher-priced leveraged loans and into lower-priced high yield. High yield remains the largest overweight in our global policy model.

EQUITIES

-

U.S. stocks have been pressured by tech weakness but helped by a strong dollar relative to other regions.

-

Valuations have been reset and central bank tightening is now closer to the end than the beginning.

-

Regional performance from here will be more driven by the relative severity of regional economic slowdowns.

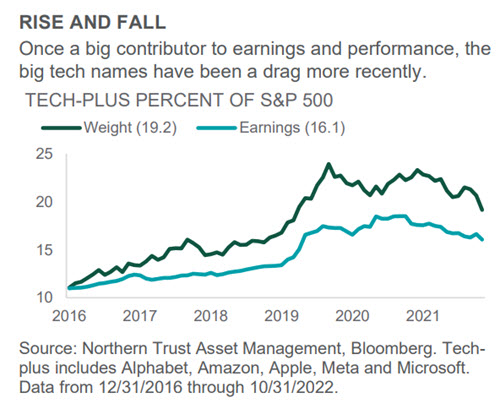

Global equities rose over the past month, shaking off a bumpy earnings season. Developed ex-U.S. equities led, followed by the U.S. and emerging markets. The former benefitted as key non-U.S. central banks considered a pivot away from tightening. Meanwhile, the Fed maintained its hawkish rhetoric. This divergence weighed on U.S. equities alongside more material negative earnings revisions – particularly in tech and tech-adjacent industries. Pandemic-induced growth in tech was assumed to represent a secular uplift in its growth trajectory; however, this proved optimistic and earnings estimates are now being reset toward more sustainable levels of growth.

As shown in the chart, the weight and earnings contribution of the five largest tech-related names (“tech-plus”) in the S&P 500 have adjusted lower, representing a headwind to U.S. stocks given the size and importance of these names. For now, positive investor attention may stay with cyclical sectors (e.g., energy), but a reset in earnings and valuation in U.S. growth stocks should eventually help the market find its footing. We remain underweight global equities with a preference for the U.S. Earnings expectations have fallen to better align with our own in the U.S., while economic conditions outside the U.S. continue to look challenging.

REAL ASSETS

-

Rumors that China will soon exit its zero-Covid policy gave natural resources a strong boost.

-

Falling interest rates gave global listed infrastructure and global real estate a strong boost.

-

Of the three real assets, we believe global listed infrastructure is currently most attractive.

Since the 10-year U.S. Treasury yield hit its recent peak of 4.24% (October 24), real assets have all outperformed the already-strong returns of global equities more broadly. Compared to the global equity return of 7.7% over this period, global listed infrastructure (GLI) and global real estate (GRE) returned 9.7% and 11.7%, respectively. We have written on these pages often about the sensitivity of these cash flow assets to moving interest rates and recent performance exemplifies the boost falling interest rates can provide. It is reasonable to expect both GLI and GRE to outperform global equities in a falling rate environment; but economic growth should dictate absolute returns. We currently prefer GLI over GRE given its lower economic sensitivity in a still-uncertain economic environment.

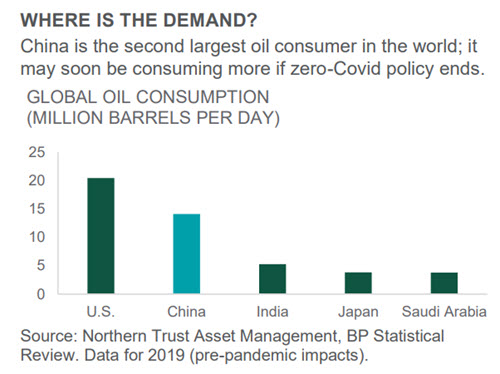

Natural resources (NR) also outperformed global equities, primarily due to rumors of China exiting its zero-Covid policy. The chart shows the top five oil consumers in the world (using 2019 data to remove pandemic influence). China’s reopening would have a big impact on global oil demand (and other commodities) – up to an extra two million barrels demanded per day. We remain cautious on China’s ability to quickly reopen – but NR may soon be a way to offset our emerging market equity underweight.

- Jim McDonald, Chief Investment Strategist

© 2022 Northern Trust Corporation.

The information contained herein is intended for use with current or prospective clients of Northern Trust Investments, Inc. The information is not intended for distribution or use by any person in any jurisdiction where such distribution would be contrary to local law or regulation. This information is obtained from sources believed to be reliable, and its accuracy and completeness are not guaranteed. Information does not constitute a recommendation of any investment strategy, is not intended as investment advice and does not take into account all the circumstances of each investor. Forward-looking statements and assumptions are Northern Trust's current estimates or expectations of future events or future results based upon proprietary research and should not be construed as an estimate or promise of results that a portfolio may achieve. Actual results could differ materially from the results indicated by this information. Investments can go down as well as up.

Northern Trust Asset Management is composed of Northern Trust Investments, Inc., Northern Trust Global Investments Limited, Northern Trust Fund Managers (Ireland) Limited, Northern Trust Global Investments Japan, K.K., NT Global Advisors, Inc., 50 South Capital Advisors, LLC, Belvedere Advisors LLC and investment personnel of The Northern Trust Company of Hong Kong Limited and The Northern Trust Company.

Issued in the United Kingdom by Northern Trust Global Investments Limited.

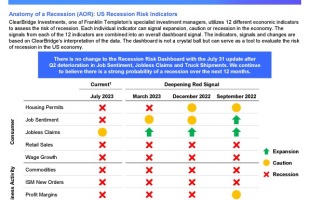

Anatomy of a Recession Update: Cracks in the Foundation

Get perspective on the most recent US economic data, the investor’s view, and how reviewing previous recessionary periods may help us today, in this conversation with Jeff Schulze, Head of Economic and Market Research at ClearBridge Investments.

AOR Update: When to expect a recession?

ClearBridge Investments: Despite improving economic sentiment now leaning the consensus view toward a soft landing, we continue to believe a recession is on the horizon.

Anatomy of a Recession: Economic and Market Outlook 3Q 2023 | August 1st

ClearBridge Investments, one of Franklin Templeton’s specialist investment managers, utilizes 12 different economic indicators to assess the risk of recession.