Global Weekly Commentary: Energy shock spurs Europe's recession

Energy shock

We think the energy crisis will spur a recession in Europe. The ECB is trying to fight inflation without recognizing the costs. We prefer credit over equities.

Market backdrop

The ECB raised rates by a record 0.75%. We think the ECB will keep raising rates through year-end until the economic effects of the energy crunch are clear.

Week ahead

All eyes are on U.S. CPI inflation for signs of further easing, especially core inflation. We expect inflation to cool but still settle above pre-Covid levels.

The energy crunch will drive a recession in Europe, as we’ve argued since March. The crisis has worsened since then as Russia has halted gas supplies. Plus, the European Central Bank (ECB) isn’t acknowledging how it will crush activity further by trying to fight high inflation, in our view. We think the ECB will wake up to this reality sooner than markets expect – but not before it inevitably faces a severe recession. We remain underweight equities and prefer high-quality credit.

Europe’s energy squeeze

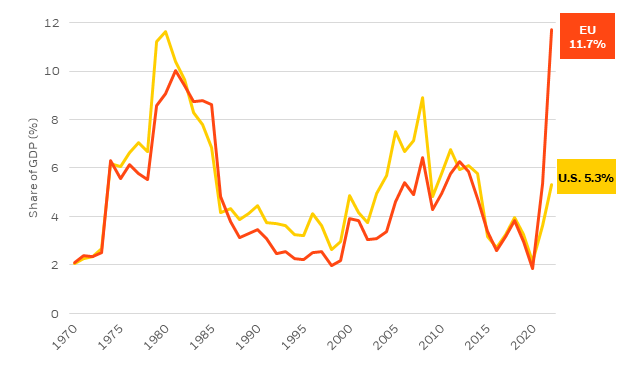

Energy burden as a share of GDP, 1970-2022

Sources: BlackRock Investment Institute and BP Statistical Review of World Energy 2021, with data from Haver Analytics. September 2022. Notes: The chart shows the cost of oil, gas and coal consumption in the European Union and U.S. as a share of GDP. We use regional energy prices and divide by GDP in U.S. dollars. Data for 2022 are based on IMF’s latest GDP forecasts and the year-to-date average of daily commodities prices.

Europe’s efforts to wean itself off Russian energy have triggered a price surge that’s been amplified as Russia cuts gas supplies. The European Union is now spending nearly 12% of its GDP on energy, making the crisis worse than the 1970s oil shocks. See orange line in the chart. That’s not the case for the U.S, a net energy exporter (yellow line). It’s hard to see any relief for Europe in the next couple of years, with rationing on the horizon, in our view. Winter may cause demand to surge, slashing stockpiles. Countries are rushing to cushion pressure, especially on households. Germany plans to collect excess profits from energy providers and cap prices. EU energy ministers have called for similar policies. The UK has a sizable plan to pay energy suppliers the difference between a new capped price and the price they would have been able to charge.

The euro area policies are much smaller than those in the UK or for Covid-19. That reinforces why the energy shock will drive a protracted recession lasting several quarters in Europe, in our view. The ECB is set to make things worse: Like the Federal Reserve, the ECB hasn’t acknowledged the damage it must do to growth to fight this inflation, even after it hiked a record 0.75% last week. The ECB is instead responding to the politics of energy-driven headline inflation, we think. Its new forecast for modest growth next year is already stale by not accounting for recent events like Russia cutting off gas supply. We see the ECB’s downside scenario of a -0.9% contraction as more likely. The euro sliding to 20-year lows against the U.S. dollar reflects deteriorating growth and terms of trade from higher energy prices, in our view.

European Central Bank view

The ECB will also have to contend with fragmentation risks – and perhaps put into practice its anti-fragmentation tool for peripheral debt spreads. Italy’s economic fundamentals have worsened in this shock, with the shift to a current account deficit amid its heavy debt burden. That’s more likely to feed volatility for Italian bonds, even if the coming election likely results in a center-right government that won’t be very antagonistic to the EU.

We think the ECB will keep up its aggressive rate hikes through the end of 2022 but then stop once it sees the economy taking a major hit. Year-end rates will likely stand somewhat short of current market rate expectations, in our view.

Bank of England view

Unlike others, the Bank of England (BoE) has been clear that bringing inflation down to target would require a deep recession. The UK’s fiscal plans wouldn’t change that, in our view. The measures are just another example of governments responding to the politics of high inflation. The subsidies may slow headline inflation and cushion the recession blow in the near term. But they can’t solve the imbalance of low supply relative to demand – and in fact block the fall in demand required to reduce inflation. Limiting the hit to real household incomes reduces the growth drag the BoE would have expected. That implies the BoE will keep hiking rates to get demand back in line with supply but not as much as markets expect, in our view.

Our bottom line

European stocks aren’t priced for the deep recession we expect. Excluding commodities, European earnings growth estimates are too optimistic, we think. We stay underweight European and most developed market stocks. We prefer investment grade credit as yields better compensate for default risk. We’re neutral European government bonds and have a modest overweight to UK gilts with a preference for short-dated bonds due to markets pricing in an overly hawkish rate path.

Market backdrop

Volatility persists across markets – underscoring the new regime of heightened macro volatility. The ECB hiked rates a record 0.75% and cut its growth forecasts last week. Yet the ECB’s new growth forecasts still don’t reflect the deep recession we expect from the energy shock and higher rates. We see the ECB jacking up rates through year-end but then stopping as the economic toll from the energy shock and rate hikes becomes clear.

The focus this week is on whether U.S. core inflation is slowing further or staying at elevated levels. The consensus sees the core CPI holding fairly steady, up by shelter costs, even if headline inflation likely cools on lower gasoline prices. The Bank of England policy meeting previously set for Sept. 15 has been rescheduled after Queen Elizabeth’s death.

Week ahead

Sept. 12

UK GDP data

Sept. 13

U.S. CPI data

Sept. 14

UK CPI data

Sept. 16

China retail sales; U.S. University of Michigan survey

Source

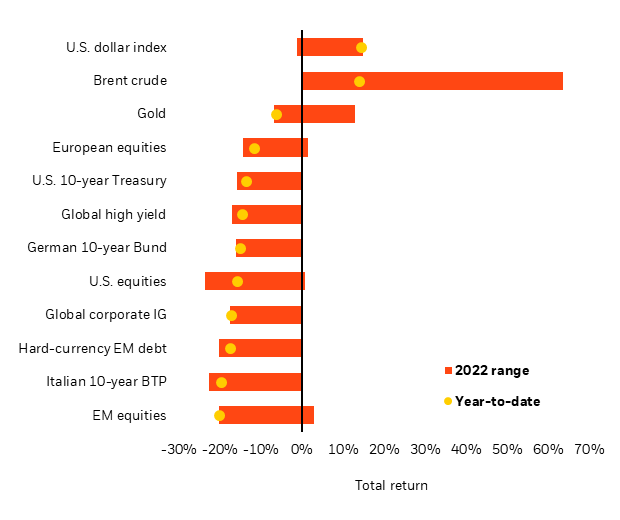

Past performance is not a reliable indicator of current or future results. Indexes are unmanaged and do not account for fees. It is not possible to invest directly in an index. Sources: BlackRock Investment Institute, with data from Refinitiv Datastream as of Sept. 8, 2022. Notes: The two ends of the bars show the lowest and highest returns at any point this year-to-date, and the dots represent current year-to-date returns. Emerging market (EM), high yield and global corporate investment grade (IG) returns are denominated in U.S. dollars, and the rest in local currencies. Indexes or prices used are: spot Brent crude, ICE U.S. Dollar Index (DXY), spot gold, MSCI Emerging Markets Index, MSCI Europe Index, Refinitiv Datastream 10-year benchmark government bond index (U.S., Germany and Italy), Bank of America Merrill Lynch Global High Yield Index, J.P. Morgan EMBI Index, Bank of America Merrill Lynch Global Broad Corporate Index and MSCI USA Index.

© 2022 BlackRock, Inc. All rights reserved.

General disclosure: This material is intended for information purposes only, and does not constitute investment advice, a recommendation or an offer or solicitation to purchase or sell any securities to any person in any jurisdiction in which an offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The opinions expressed are as of Sept. 12, 2022 , and are subject to change without notice. Reliance upon information in this material is at the sole discretion of the reader. Investing involves risks.

In the U.S. and Canada, this material is intended for public distribution. In the European Economic Area (EEA): this is Issued by BlackRock (Netherlands) B.V. is authorised and regulated by the Netherlands Authority for the Financial Markets. Registered office Amstelplein 1, 1096 HA, Amsterdam, Tel: 020 – 549 5200, Tel: 31-20-549-5200. Trade Register No. 17068311 For your protection telephone calls are usually recorded. In the UK and Non-European Economic Area (EEA) countries: this is Issued by BlackRock Advisors (UK) Limited, which is authorised and regulated by the Financial Conduct Authority. Registered office: 12 Throgmorton Avenue, London, EC2N 2DL, Tel: +44 (0)20 7743 3000. Registered in England and Wales No. 00796793. For your protection, calls are usually recorded. Please refer to the Financial Conduct Authority website for a list of authorised activities conducted by BlackRock. In Switzerland, This document is marketing material. Until 31 December 2021, this document shall be exclusively made available to, and directed at, qualified investors as defined in the Swiss Collective Investment Schemes Act of 23 June 2006 (“CISA”), as amended. From 1 January 2022, this document shall be exclusively made available to, and directed at, qualified investors as defined in Article 10 (3) of the CISA of 23 June 2006, as amended, at the exclusion of qualified investors with an opting-out pursuant to Art. 5 (1) of the Swiss Federal Act on Financial Services ("FinSA"). For information on art. 8 / 9 Financial Services Act (FinSA) and on your client segmentation under art. 4 FinSA, please see the following website: www.blackrock.com/finsa For investors in Israel: BlackRock Investment Management (UK) Limited is not licensed under Israel’s Regulation of Investment Advice, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”), nor does it carry insurance thereunder. In South Africa, please be advised that BlackRock Investment Management (UK) Limited is an authorized financial services provider with the South African Financial Services Board, FSP No. 43288. In the DIFC this material can be distributed in and from the Dubai International Financial Centre (DIFC) by BlackRock Advisors (UK) Limited — Dubai Branch which is regulated by the Dubai Financial Services Authority (DFSA). This material is only directed at 'Professional Clients’ and no other person should rely upon the information contained within it. Blackrock Advisors (UK) Limited - Dubai Branch is a DIFC Foreign Recognised Company registered with the DIFC Registrar of Companies (DIFC Registered Number 546), with its office at Unit 06/07, Level 1, Al Fattan Currency House, DIFC, PO Box 506661, Dubai, UAE, and is regulated by the DFSA to engage in the regulated activities of ‘Advising on Financial Products’ and ‘Arranging Deals in Investments’ in or from the DIFC, both of which are limited to units in a collective investment fund (DFSA Reference Number F000738) In the Kingdom of Saudi Arabia, issued in the Kingdom of Saudi Arabia (KSA) by BlackRock Saudi Arabia (BSA), authorised and regulated by the Capital Market Authority (CMA), License No. 18-192-30. Registered under the laws of KSA. Registered office: 29th floor, Olaya Towers – Tower B, 3074 Prince Mohammed bin Abdulaziz St., Olaya District, Riyadh 12213 – 8022, KSA, Tel: +966 11 838 3600. The information contained within is intended strictly for Sophisticated Investors as defined in the CMA Implementing Regulations. Neither the CMA or any other authority or regulator located in KSA has approved this information. The information contained within, does not constitute and should not be construed as an offer of, invitation or proposal to make an offer for, recommendation to apply for or an opinion or guidance on a financial product, service and/or strategy. Any distribution, by whatever means, of the information within and related material to persons other than those referred to above is strictly prohibited. In the United Arab Emirates is only intended for - natural Qualified Investor as defined by the Securities and Commodities Authority (SCA) Chairman Decision No. 3/R.M. of 2017 concerning Promoting and Introducing Regulations. Neither the DFSA or any other authority or regulator located in the GCC or MENA region has approved this information. In the State of Kuwait, those who meet the description of a Professional Client as defined under the Kuwait Capital Markets Law and its Executive Bylaws. In the Sultanate of Oman, to sophisticated institutions who have experience in investing in local and international securities, are financially solvent and have knowledge of the risks associated with investing in securities. In Qatar, for distribution with pre-selected institutional investors or high net worth investors. In the Kingdom of Bahrain, to Central Bank of Bahrain (CBB) Category 1 or Category 2 licensed investment firms, CBB licensed banks or those who would meet the description of an Expert Investor or Accredited Investors as defined in the CBB Rulebook. The information contained in this document, does not constitute and should not be construed as an offer of, invitation, inducement or proposal to make an offer for, recommendation to apply for or an opinion or guidance on a financial product, service and/or strategy. In Singapore, this is issued by BlackRock (Singapore) Limited (Co. registration no. 200010143N). This advertisement or publication has not been reviewed by the Monetary Authority of Singapore. In Hong Kong, this material is issued by BlackRock Asset Management North Asia Limited and has not been reviewed by the Securities and Futures Commission of Hong Kong. In South Korea, this material is for distribution to the Qualified Professional Investors (as defined in the Financial Investment Services and Capital Market Act and its sub-regulations). In Taiwan, independently operated by BlackRock Investment Management (Taiwan) Limited. Address: 28F., No. 100, Songren Rd., Xinyi Dist., Taipei City 110, Taiwan. Tel: (02)23261600. In Japan, this is issued by BlackRock Japan. Co., Ltd. (Financial Instruments Business Operator: The Kanto Regional Financial Bureau. License No375, Association Memberships: Japan Investment Advisers Association, the Investment Trusts Association, Japan, Japan Securities Dealers Association, Type II Financial Instruments Firms Association.) For Professional Investors only (Professional Investor is defined in Financial Instruments and Exchange Act). In Australia, issued by BlackRock Investment Management (Australia) Limited ABN 13 006 165 975 AFSL 230 523 (BIMAL). The material provides general information only and does not take into account your individual objectives, financial situation, needs or circumstances. In China, this material may not be distributed to individuals resident in the People’s Republic of China (“PRC”, for such purposes, excluding Hong Kong, Macau and Taiwan) or entities registered in the PRC unless such parties have received all the required PRC government approvals to participate in any investment or receive any investment advisory or investment management services. For Other APAC Countries, this material is issued for Institutional Investors only (or professional/sophisticated /qualified investors, as such term may apply in local jurisdictions). In Latin America, no securities regulator within Latin America has confirmed the accuracy of any information contained herein. The provision of investment management and investment advisory services is a regulated activity in Mexico thus is subject to strict rules. For more information on the Investment Advisory Services offered by BlackRock Mexico please refer to the Investment Services Guide available at www.blackrock.com/mx

Not FDIC Insured | May Lose Value | No Bank Guarantee

© 2022 BlackRock, Inc. All Rights Reserved. BLACKROCK, iSHARES and ALADDIN are trademarks of BlackRock, Inc. or its subsidiaries in the United States and elsewhere. All other trademarks are those of their respective owners.

BIIM0922U/M-2418840

Weekly Investment Commentary: Earnings season: investment ideas

First-quarter earnings season has kicked off with the utilities and communication services sectors projected to deliver the strongest year-over-year EPS growth, while estimates for materials and energy are expected to decline the most.

Global Weekly Commentary: Earnings growth not just about tech

Solid U.S. economic and corporate earnings growth have supported risk appetite, driving stocks to all-time highs – even as bond yields have jumped. We think earnings will need to deliver on high expectations, especially after last week’s data showing sticky inflation spooked investors.

Global Markets Weekly Update: April 12, 2024

Review the performance of global stock and bond markets over the past week, along with relevant insights from T. Rowe Price economists and investment professionals.