FAQ: What Does Russia’s Invasion of Ukraine Mean for the Market?

Key takeaways

- We continue to monitor events and their impact on asset classes closely. As our conditions and our views evolve, we will provide our financial advisors with updated commentary.

- Our advice, as contrary as it may sound, is to stay the course. This is subtly different to doing nothing—it means you should review your goals, affirm your risk tolerance, and make sure they align with your portfolio.

- Our focus remains on fundamentals. In a crisis of this magnitude, the chance that not just prices but also fundamentals are in flux is a very real possibility. As a result, our team is focusing on fundamental shifts that impact earnings, dividends, and valuations.

Mounting tensions between Russia and Ukraine resulted in a Russian invasion into Ukraine sovereign territory in February. Below we offer our perspective on the market’s response. We continue to monitor events and their impact on asset classes closely. As our conditions and our views evolve, we will provide our financial advisors with updated commentary.

How has the market responded to the armed conflict?

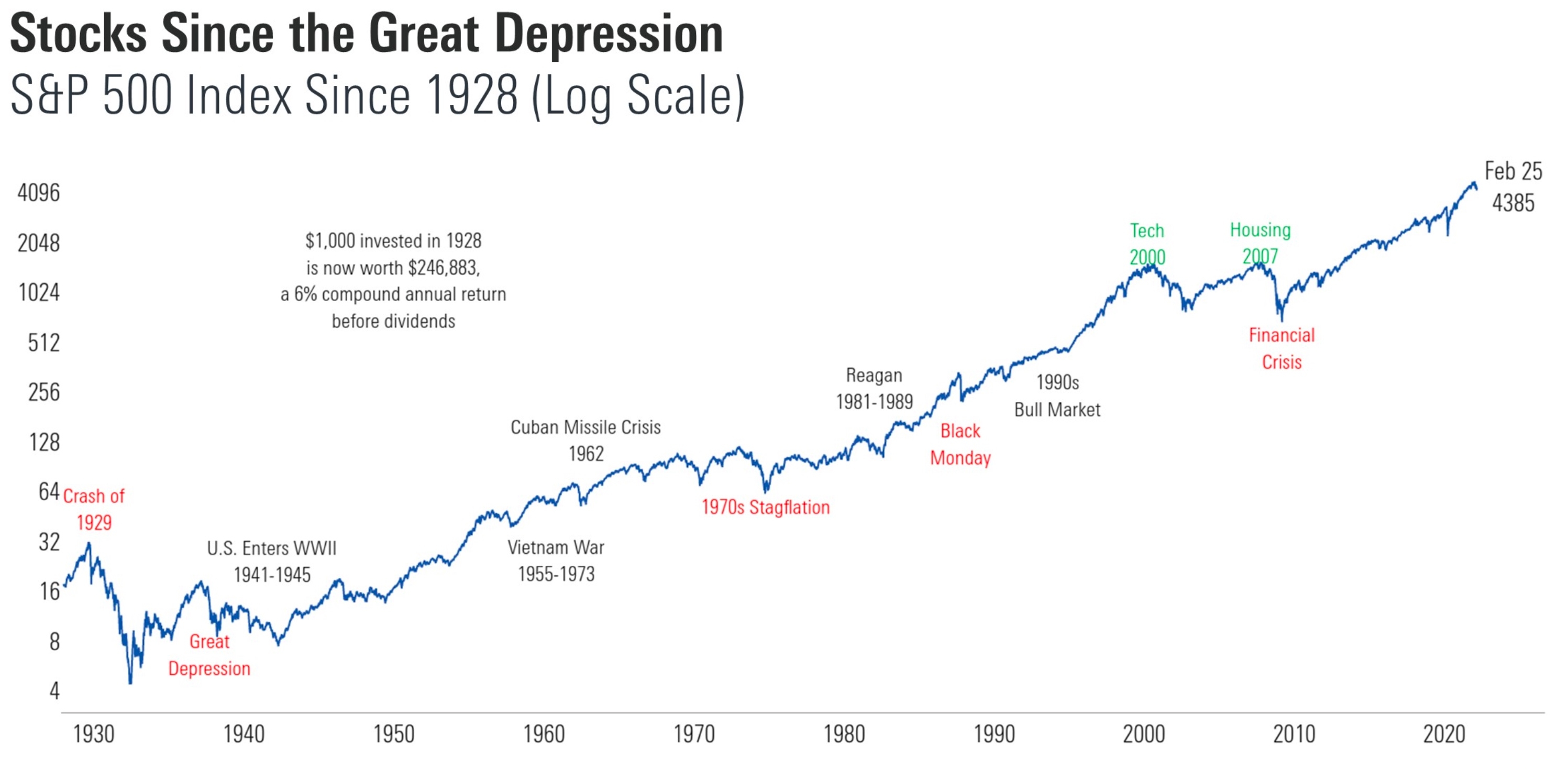

Markets ended the year arguably priced to perfection, with the Morningstar US Market Index up 25.8%; in fact, 2021 marked the eighth year of double-digit gains in the past decade. But uncertainty around how long inflation would remain at high levels and the growing possibility of a shift to a less accommodative policy by the Federal Reserve became a source of volatility during the first month of the year; in January, the Morningstar US Market Index was down 5.9%.

Adding to the worries in February was the growing tension between Russia and Ukraine. As Russia became increasingly aggressive, investors grew nervous. On Feb. 22, when Russia established a military presence in the region already held by Moscow-backed separatists, the Morningstar US Market Index was down 1.1%, and the Morningstar Global Markets ex-US was down 0.7%. Within a little more than a day, with a full-scale invasion underway, fear and uncertainty roiled global markets and led to a wide array of results. On Feb. 24, the Morningstar Emerging Markets Index ended down 4.3%, the Morningstar Europe Index was down 5.6%, Intermediate Treasuries finished up 0.1%, and the Morningstar US Market Index closed up 1.8% despite rocky performance early in the day.

Markets continued to tumble by varying degrees in the week that followed, as the scale of human suffering skyrocketed and the response of Western nations isolated Russia from much of its typical economic and financial activity. From the Feb. 24 start of the invasion through March 7, the Morningstar US Market Index lost 0.7% and the Morningstar Global Markets ex US fell 7.7%, with heavily impacted markets such as Germany dropping 15.8%, as measured by the Morningstar Germany Index.

Advisors and their clients potentially have the hardest job of all. Our advice, as contrary as it may sound, is to stay the course. This is subtly different to doing nothing—it means you should review your goals, affirm your risk tolerance, and make sure they align with your portfolio. This turns a nearly impossible task (when the headlines are screaming, and we are living through history) into an actionable and positive plan. It is also worth remembering that despite a myriad of horrific wars, inflation, and other tragedies, in the long run the markets have managed to climb higher.

Source: Clearnomics, Standard & Poor’s1

And if clients are in portfolios that are well calibrated to their financial goals, then adjusting as markets are selling off is less a form of risk control and more a recipe for loss. That is because not only is it hard to predict whether losses will continue, it’s also hard to predict when markets will suddenly recover. In fact, studies show that market timing is especially difficult because investors need to make two—not one—decisions: when to get out and when to get back in. Getting both decisions right has proven elusive to most investors. It’s just too complex a world.

Will we continue to see market losses?

We’ve always been of the view that anticipating price moves over the next few days, weeks, or even months is a fool’s errand. Daily price moves happen at random, and we have no advantage in predicting geopolitical outcomes. We aren’t alone in that: very few, if anyone, do. That said, history tells us investors hate uncertainty, and uncertainty remains high. So, volatility remains our default expectation; indeed, there is a wide range of potential outcomes to the current conflict and its resulting impact on related financial markets.

How is the Morningstar Investment Management team responding to the conflict and the price moves?

Our focus remains on fundamentals and the degree to which price movements become unmoored from those underpinnings. Of course, in a crisis of this magnitude, the chance that not just prices but also fundamentals are in flux is a very real possibility. As a result, our team is focusing on fundamental shifts that impact earnings, dividends, and valuations. We won’t likely know the lasting impact immediately, so in the meantime, we are watching the price behavior of asset classes that are unrelated to the conflict. Should those areas sell off in sympathy, we are more likely to consider the price gap an opportunity to add at better price points. Top of mind for us are areas such as Germany and European financials, which have suffered far more than other regions. In the case of Germany, we are considering the potential for supply-chain disruptions, given the country’s significant international trade. For European financials, and banks in particular, we are considering direct exposure to Russia and the impact potential write-downs could have on our assessment of company value. We’re also testing various macroeconomic scenarios, including a recessionary environment, given banks’ economic sensitivity.

Morningstar Investment Management is a big believer in behavioral finance. How does that impact your decision-making at this juncture?

Being big believers in behavioral finance is another way of saying we are aware of our weaknesses. As humans with all the usual mental shortcomings, we are tempted to develop attractive narratives and overweight those narratives when thinking about the outcome. Trying to think through the political and economic impact is more likely to harm than help returns.

Like everyone else, we are also prone to recency bias, meaning we let our most recent experience dictate our overall perspective. Our most recent experience of market volatility was a sharp bounce; that outcome may or may not be the case this time.

Rather than equating recent market movement with today’s environment, we take a longer look back through history and consider the wider range of outcomes that could occur. Then, at the risk of sounding like a broken record, we return to the lasting impact on the fundamentals, which in the long run drive asset-class returns.

What can we expect from Morningstar Investment Management going forward?

Know that we are laser-focused on managing the portfolios we offer you and are leveraging our global team to develop a fundamental view that we believe will ultimately drive returns over the appropriate time horizon. We’ve put enormous effort into calibrating each portfolio so that it is taking the appropriate amount of risk for its objective, and we will adjust those portfolios in real time to take advantage of opportunities as we think we see them. This means, unfortunately, that we won’t avoid all daily losses. We do believe, however, that our efforts will put investors in the best position possible to help achieve their individual financial goals over the longer term.

As always, we appreciate the opportunity to work with you and will continue to communicate our latest views as conditions evolve.

1For illustrative purposes only. Index is unmanaged and is not available for direct investment. Past performance is not a guarantee of future results.

Opinions expressed are as of the current date; such opinions are subject to change without notice. Morningstar Investment Management shall not be responsible for any trading decisions, damages, or other losses resulting from, or related to, the information, data, analyses or opinions or their use. This commentary is for informational purposes only. The information, data, analyses, and opinions presented herein do not constitute investment advice, are provided solely for informational purposes and therefore are not an offer to buy or sell a security. Please note that references to specific securities or other investment options within this piece should not be considered an offer (as defined by the Securities and Exchange Act) to purchase or sell that specific investment. Performance data shown represents past performance. Past performance does not guarantee future results. All investments involve risk, including the loss of principal. There can be no assurance that any financial strategy will be successful. Morningstar Investment Management does not guarantee that the results of their advice, recommendations or objectives of a strategy will be achieved. This commentary contains certain forward-looking statements. We use words such as “expects”, “anticipates”, “believes”, “estimates”, “forecasts”, and similar expressions to identify forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results to differ materially and/or substantially from any future results, performance or achievements expressed or implied by those projected in the forward-looking statements for any reason. Past performance does not guarantee future results. Morningstar® Managed PortfoliosSM are offered by the entities within Morningstar’s Investment Management group, which includes subsidiaries of Morningstar, Inc. that are authorized in the appropriate jurisdiction to provide consulting or advisory services in North America, Europe, Asia, Australia, and Africa. In the United States, Morningstar Managed Portfolios are offered by Morningstar Investment Services LLC or Morningstar Investment Management LLC, both registered investment advisers, as part of various advisory services offered on a discretionary or non-discretionary basis. Portfolio construction and on-going monitoring and maintenance of the portfolios within the program is provided on Morningstar Investment Services behalf by Morningstar Investment Management LLC. Morningstar Managed Portfolios offered by Morningstar Investment Services LLC or Morningstar Investment Management LLC are intended for citizens or legal residents of the United States or its territories and can only be offered by a registered investment adviser or investment adviser representative. Investing in international securities involve additional risks. These risks include, but are not limited to, currency risk, political risk, and risk associated with varying accounting standards. Investing in emerging markets may increase these risks. Emerging markets are countries with relatively young stock and bond markets. Typically, emerging-markets investments have the potential for losses and gains larger than those of developed-market investments. A debt security refers to money borrowed that must be repaid that has a fixed amount, a maturity date(s), and usually a specific rate of interest. Some debt securities are discounted in the original purchase price. Examples of debt securities are treasury bills, bonds and commercial paper. The borrower pays interest for the use of the money and pays the principal amount on a specified date. The indexes noted are unmanaged and cannot be directly invested in. Individual index performance is provided as a reference only. Since indexes and/or composition levels may change over time, actual return and risk characteristics may be higher or lower than those presented. Although index performance data is gathered from reliable sources, Morningstar Investment Management cannot guarantee its accuracy, completeness or reliability. The Morningstar US Market Index measures the performance of US securities and targets 97% market capitalization coverage of the investable universe. It is a diversified broad market index. This Index does not incorporate Environmental, Social, or Governance (ESG) criteria. The Morningstar Global Markets ex-US Index measures the performance of the stocks located in the developed and emerging countries across the world (excluding the United States) as defined by Morningstar. Stocks in the index are weighted by their float capital, which removes corporate cross ownership, government holdings and other locked-in shares. This Index does not incorporate Environmental, Social, or Governance (ESG) criteria. The Morningstar Emerging Markets Index measures the performance of emerging markets targeting the top 97% of stocks by market capitalization. This Index does not incorporate Environmental, Social, or Governance (ESG) criteria. The Morningstar Europe Index measures the performance of Europe's broad regional markets targeting the top 97% of stocks by market capitalization. This Index does not incorporate Environmental, Social, or Governance (ESG) criteria.

Weekly Investment Commentary: Earnings season: investment ideas

First-quarter earnings season has kicked off with the utilities and communication services sectors projected to deliver the strongest year-over-year EPS growth, while estimates for materials and energy are expected to decline the most.

Global Weekly Commentary: Earnings growth not just about tech

Solid U.S. economic and corporate earnings growth have supported risk appetite, driving stocks to all-time highs – even as bond yields have jumped. We think earnings will need to deliver on high expectations, especially after last week’s data showing sticky inflation spooked investors.

Global Markets Weekly Update: April 12, 2024

Review the performance of global stock and bond markets over the past week, along with relevant insights from T. Rowe Price economists and investment professionals.