Equity Outlook: Bracing for an Economic Slowdown

Spiking inflation, rising interest rates and growing fears of a US recession dominated global equity markets in the second quarter. While the outlook is very cloudy, it’s important to evaluate what types of strategies can help investors in an economic downturn.

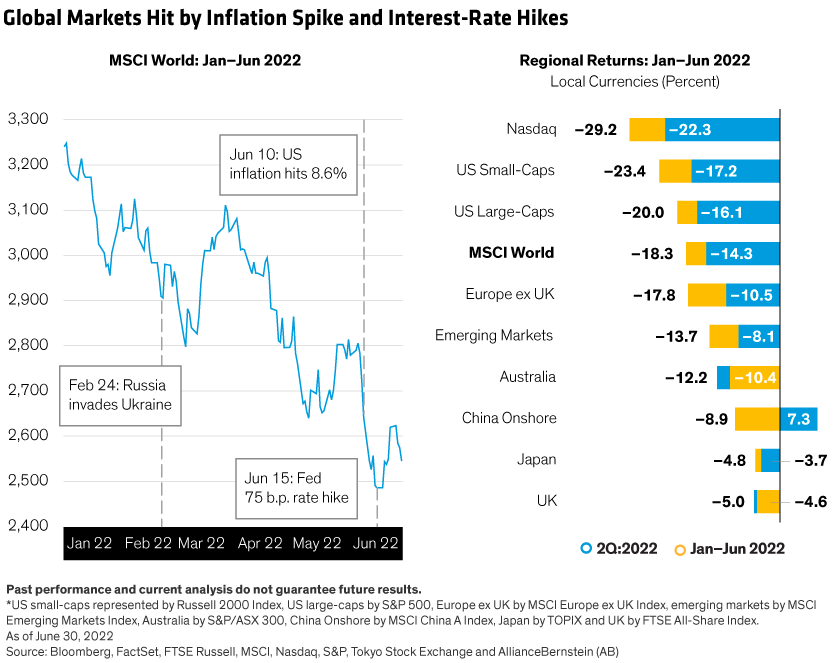

Equity investors have suffered a painful six months. Global equities fell sharply in the second quarter as US markets slid into bear market territory. The MSCI World Index fell by 14.3%, in local-currency terms, in the quarter and was down 18.3% in the first half of 2022 (Display). US large-cap stocks tumbled by 16.1% in the quarter and lost 20.0% in the first half. Regional returns were diverse, with relatively modest declines in the UK and Japan. Emerging market losses were offset by gains in Chinese stocks. Individual outcomes were affected by a strengthening US dollar, reducing losses for non-US investors in American equity portfolios.

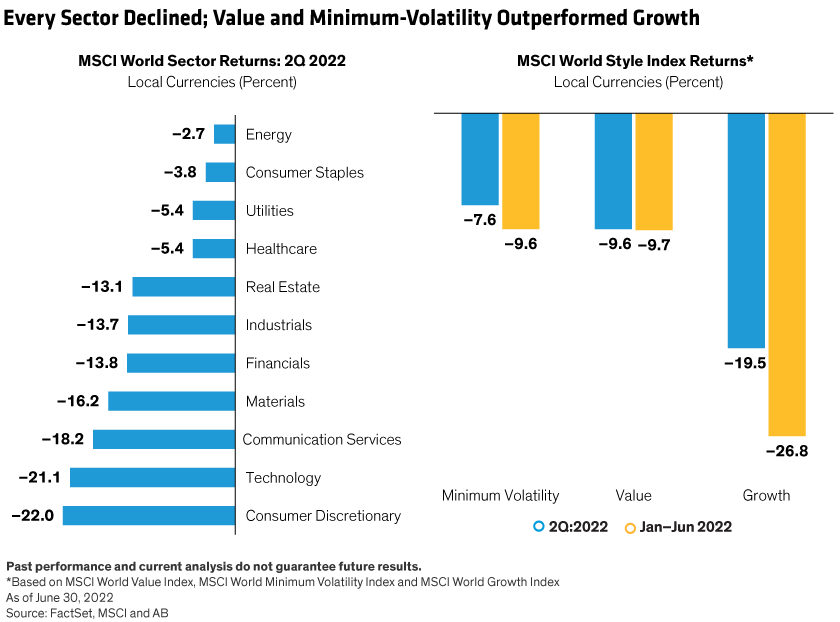

Consumer-discretionary and technology stocks were hit hardest (Display). Energy stocks outperformed but ended the quarter down on fears of falling demand. Defensive sectors, such as consumer staples and utilities, were relatively resilient. Minimum-volatility and value stocks outperformed growth stocks. Meanwhile, cryptocurrency values crashed, as heightened risk aversion led investors to abandon speculative assets.

The market shock reflects runaway inflation in several regions, which has fostered uncertainty and policy differences around the world. The European Central Bank is preparing for its first interest-rate hike in more than a decade. In the UK, stagflation—a toxic combination of inflation and slowing growth—is taking root. In contrast, inflation remains low in Japan, which is sticking with loose monetary policy. China is asynchronous to developed economies, as it eases policy to help achieve the government’s GDP growth target of 5.5%, while enforcing a zero-COVID agenda that has stifled economic activity. And with no end in sight to the Russia-Ukraine war, geopolitical instability continues to weigh on the global outlook.

US Economic Drama Takes Center Stage

But the drama unfolding in the US economy took center stage in the quarter. Concerns about the impact of rapidly rising US interest rates on equity valuations evolved into recession worries. Investors are now asking whether company earnings will moderate as both demand and margins come under pressure.

Escalating inflation is at the heart of the problem. On June 10, the consumer price index for May showed US inflation jumping to a 40-year high of 8.6%. Five days later, the Federal Reserve raised interest rates by 75 basis points, its biggest hike since 1994, lifting the fed funds rate target to between 1.5% and 1.75%. Fed Chair Jerome Powell made clear that the top priority is to cool inflation, widely seen as a sign that the Fed was willing to risk tipping the US economy into a slowdown or recession. With US stocks ending the quarter more than 20% below their January peak—the standard definition of a bear market—recession fears eclipsed hopes of a soft landing for the US economy.

So how likely is a US recession? On the one hand, US bear markets have signaled recessions in all but one case since 1970. Consumer and business confidence indicators are deteriorating, while falling stock prices have eroded personal wealth, which may lead to a reduction in spending. Many supply-side imbalances, from oil prices to supply chain disruptions, are simply out of the Fed’s control.

Yet there are some mitigating forces. Wholesale inventories are back to normal levels in many industries. US household and bank balance sheets are healthy. While a slowing economy will erode consumer strength, if energy prices ease and inflation expectations fall, monetary policy pressure could be reduced.

What Are Equity Prices Implying?

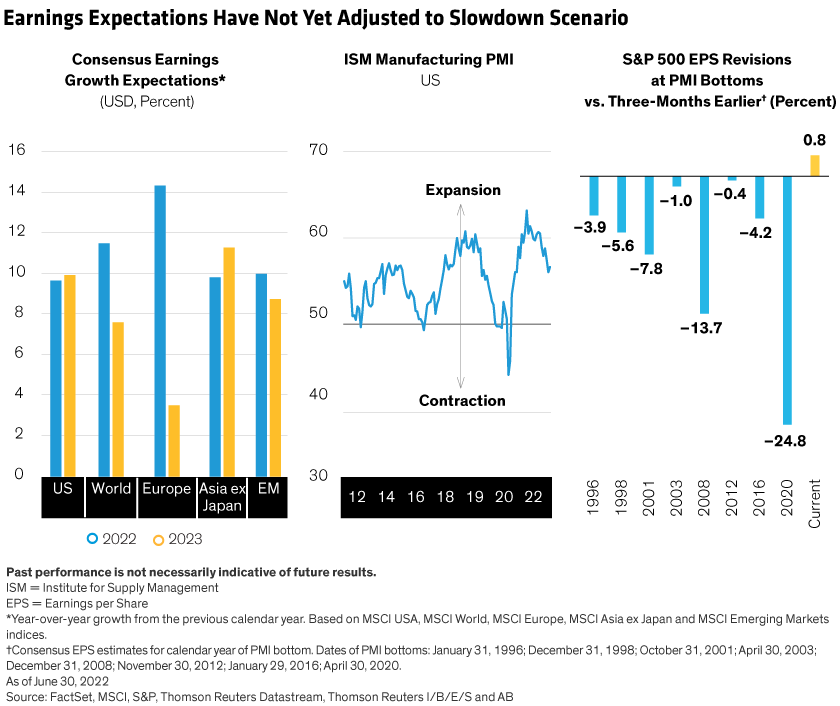

Every economic slowdown has unique features. As the third quarter begins, it’s clear that US interest rates are going up and the Purchasing Managers’ Index (PMI), an important signal of economic expansions and contractions, is pointing downward. In previous economic slowdowns, corporate earnings revisions came down significantly as the PMI bottomed.

That hasn’t happened yet. Stock market declines this year were driven mainly by multiple compression. In other words, share prices fell while forward-earnings forecasts generally did not—in the US and other markets (Display); in some cases, particularly Europe, earnings forecast revisions are still positive. This implies that earnings forecasts are likely to fall, and equities may see further declines.

Connecting the dots between recessions and market bottoms is tricky. Economic data are lagging, while markets are forward looking. So often, by the time the data tell us the economy has contracted, we’re already entering a new phase of recovery. Our research of 14 US recessions since 1937 suggests that the market bottom occurs on average 211 days after a recession began (Display). But every downturn is different; in 2020, the market bottomed just 23 days after the start of the brief recession as governments and central banks responded with unprecedented fiscal and monetary easing. Today, with the Fed committed to bringing inflation under control, we shouldn’t count on policy support to drive such a rapid rebound.

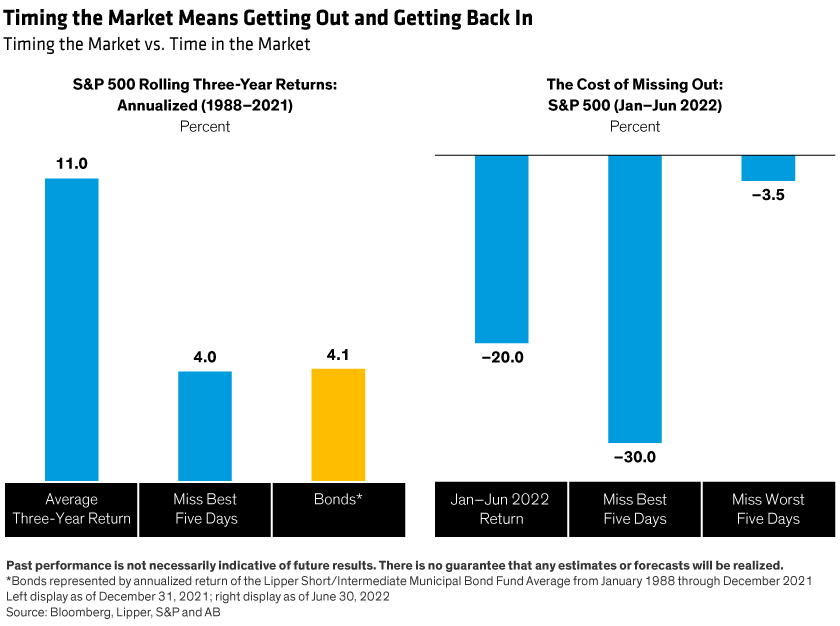

One thing is certain: it is extremely difficult to time market inflection points and investors who try to do so often end up hurting themselves. Missing the five best days of US market gains since 1988 would reduce annualized three-year returns to just 4%, compared with 11% for those who stayed in the market (Display). Similarly, in the first half of 2022, missing the five best market days meant much steeper losses.

Why stay in equities in this turbulent environment? Because equities remain a vital source of long-term returns even in economically challenging periods with heightened market volatility. Following recent declines, current valuations point to improved forward long-term return potential. What’s more, equities are an important hedge against inflation risk, and with correlations between stocks and bonds turning positive this year, the traditional diversification benefits of fixed income are muted.

Playing Defense with Quality

That said, equity allocations deserve scrutiny. In our view, equity portfolios of all types should emphasize quality companies with business resilience for a downturn and rebound potential for a recovery. Although quality stocks underperformed this year, as inflation comes down from extreme highs and economic activity moderates, we expect quality to come back into vogue.

Cash flows are an essential indicator of quality. Companies with high free cash flow have historically performed better through economic slowdowns and recessions. Pricing power, another important quality feature, can help companies maintain margins in inflationary times. Healthy balance sheets and low debt levels offer some protection from rising interest rates. Competitive advantages, innovative cultures and strong management teams bolster business quality for tougher times.

Balancing Defensive Strategies with Future Recovery Potential

Strategies that explicitly aim to reduce risk can help investors stay in the market through tougher times. Lower-volatility portfolios focused on high-quality businesses with stable stocks trading at attractive prices can help alleviate volatility in a downturn.

Still, we caution against being overly defensive, which could limit return potential in a recovery. To that end, diversifying style and regional exposures is important. Investors who have been heavily weighted toward growth stocks might consider shifting toward value equity portfolios that should do well in an inflationary environment. Many investors are under-allocated to emerging markets, where valuations are attractive, particularly in China, which may be poised for recovery given its loosening monetary policy and fiscal stimulus.

Companies will be affected in different ways in a weaker economy. Fundamental research is the key to identifying stocks that can make it to the other side in better shape than peers. And shares of select companies are trading at extremely depressed valuations that exaggerate the potential impact of a recession on their businesses.

While we adjust our expectations for this evolving environment, investors should also remember that downturns aren’t forever. Taking a long-term view on business dynamics and earnings potential, while being mindful of near-term risks, will help position portfolios for an uncertain future—and beyond.

Chris Hogbin is Head of Equities at AllianceBernstein (AB).

The views expressed herein do not constitute research, investment advice or trade recommendations and do not necessarily represent the views of all AB portfolio-management teams and are subject to revision over time.

MSCI makes no express or implied warranties or representations, and shall have no liability whatsoever with respect to any MSCI data contained herein.

The MSCI data may not be further redistributed or used as a basis for other indices or any securities or financial products. This report is not approved, reviewed or produced by MSCI.

Peeling back the onion: A concentric approach to investment decision making

Portfolio Managers Greg Wilensky and Jeremiah Buckley offer a framework for interpreting economic news for investment decision making.

What is ESG and why do we care?

Michelle Dunstan, Janus Henderson’s Chief Responsibility Officer, explores ESG considerations and highlights how ESG integration helps Janus Henderson deliver on client goals and aspirations.

Hiding in plain sight: The investment case for healthcare

Though healthcare may have flown under the market’s radar this year, the sector’s attractive valuations and new growth opportunities are not to be overlooked, say Portfolio Managers Andy Acker and Dan Lyons.