Economic and Commercial Real Estate Outlook: Bracing for Uncertain Times

Open and Download the Full Article Here: Open Full Article

Executive Summary

- The global economy faces material headwinds heading into the second half of 2022 from ongoing conflict in Ukraine, stubbornly disrupted supply chains, and central banks tightening monetary policy swiftly to try control very high inflation levels. This central bank pivot comes at a dangerous time for growth, as consumer sentiment wanes, brewing a potentially dangerous cocktail.

- The U.S. economy has been on the forefront of these headwinds, but weak growth and conflict in Ukraine has more directly impacted the European Union in recent months. Both major economies could enter recession in the next 12 months.

- Though not all recessions have an indelible impact on commercial real estate markets, investors should anticipate some decline in capital values.

- Under a slower growth/recessionary scenario, investment performance will vary widely across property sectors. We view sectors that have better long-term structural drivers as more durable during a downturn, while more cyclical sectors (office, retail and hotel) will likely see broader declines in fundamentals potentially allowing price discovery and opening investment opportunities that have been generally scarce.

Global economic outlook now fraught with risks

The global economy is rapidly approaching a crossroad as it confronts fast growing consumer prices, weaker fiscal support and the ongoing impact of geopolitical conflict that is disrupting global trade already challenged by dislocated supply chains. In the U.S., the Federal Reserve has pivoted hard to remove record level monetary accommodation and tighten financial conditions.

The European Central Bank is mulling tighter monetary policy though it faces the more immediate challenge of record-high energy prices which may make it harder to increase interest rates.

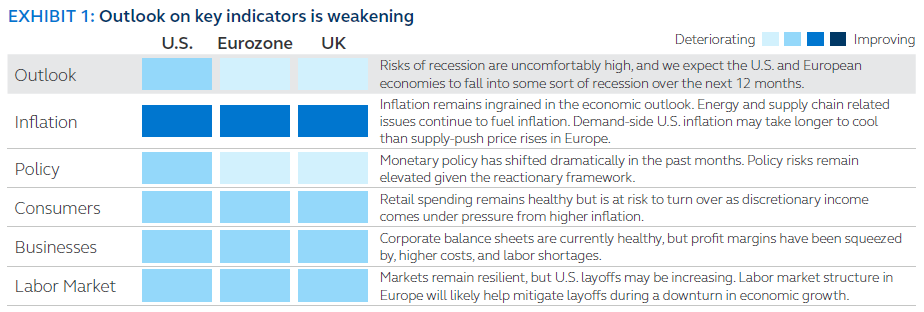

Both economies are poised to see a deterioration in key indicators (exhibit 1) which has sent a chill air to traditional risk assets that have suffered their worst year-to-date performance in decades.

Commercial real estate has not escaped the deterioration in sentiment with public quadrants experiencing double-digit decline in performance (-20%, -10% for REITs and CMBS A 2.0 respectively) year-to-date. Private real estate index values have yet to see a draw-down in capital values given the scarcity of transactions. That said, we are starting to see signs of weakness and repricing in transaction markets as inflation, interest rates and uncertainty filter through to the private real estate sales market.

In this paper we discuss changes to our baseline outlook given persistently high inflation and a more hawkish central bank policy regime which have greatly increased the probability of recession and the likely impact on property sectors in both Europe and the U.S.

Baseline: Talking ourselves into a recession

United States

Although GDP growth has weakened considerably during the first half of 2022, it has been largely attributable to the effects of a widening trade deficit, inventories, and a reduction in government consumption. Payrolls continue to grow at a solid pace; job openings are outstripping unemployed individuals by nearly two to one; the financial system is well capitalized; and corporate balance sheets are in good shape. These are hardly signs of an economy on the

verge of recession.

Yet, rising policy rates, high-levels of inflation—particularly gasoline prices, which have proved a catalyst for every U.S. recession since the 1970s, are beginning to weigh on both consumer balance sheets and sentiment. Higher policy and treasury yields are also starting to weigh on housing affordability. Taken together, these factors have elevated the risk of recession to uncomfortable levels.

Our internal view has evolved in recent weeks such that we feel a recession is more likely than not over the next 12 months. Consumer spending is generally healthy but showing signs of strain under higher prices and increased uncertainty—in real terms retail spending growth is negative. Corporations have seen their profit margins come under pressure and there are nascent reports of layoffs in the technology, retail, and banking industries.

We expect the ensuing recession to be moderate, imagining a retracing of the unemployment rate from its current full-employment level of 3.5% to roughly 5%. This would imply a peak to trough drawdown in payroll employment of between two to three million— significant enough to have reverberations across the economy. Energy markets already in the early stages of a correction would see price pressures ease. Interest rates would remain higher than what we have been accustomed to over the past decade, but inflation, in the absence of a material recession, would likely decline at a slow pace towards the Fed’s target rate of 2% owing to continued supply chain issues. The Fed would have little option but to start cutting its policy rate once it believes it has achieved a reasonable trade-off between inflation and growth, which remains a wild card in terms

of timing.

Europe

The ECB faces a difficult task in reversing decade-long easy monetary policy without tipping the economy into recession. The endeavor is made more challenging by two additional risks, namely a possible debt and energy crises.

Due to the imperfect nature of the monetary union, rising interest rates may reverberate with different intensity across the member states, widening the borrowing cost spreads for those countries with higher debt levels. To contain unwarranted divergence, the ECB is devising a new anti-fragmentation tool, details of which will be announced by the end of July. Any assessment of the feasibility and efficacy of this tool must wait until then.

The second risk refers to the geographical proximity to the conflict in Ukraine and to the dependency on energy imports from Russia. Gas prices in the eurozone reached an all-time high in June amid Russia’s unilateral decision to reduce supplies. This contributed to driving annual inflation to double-digit levels in nearly half of the states comprising the monetary union. The combination of soaring prices and tightening monetary policy has led to a squeeze in real household disposable income and a sharp drop in consumer confidence across the continent. So far, consumer spending has held on, buffered by savings accumulated during the pandemic, strong labor market and governments™ temporary relief measures. However, the first signs of weakening demand have started to emerge, as retail sales stagnated in the European Union in May versus the previous month and declined outright in the UK.

Assuming the relationships with Russia will remain tense, the energy deficit is only set to increase, especially during the winter months when demand reaches its peak. Since the Ukraine invasion last February, Europe has reduced Russian gas supplies from 40% to 20% of total imports. However, the International Energy Agency has warned the continent to prepare for the likelihood of a complete cut-off, which may tip Europe into a more severe recession compared to the U.S. Under this scenario, the ECB estimated the Euro area’s economy will shrink by

-1.7% in 2023.

Economic impact on commercial real estate

The impact of our slower growth/recessionary scenario will differ across property types. Elevated valuations remain well supported by property fundamentals in both the U.S. and Europe with the notable exception of office (in the U.S.) where utilization rates remain depressed. Retail too will encounter weakness, particularly in the larger shopping center (regional mall) format. A downturn in economic activity at this stage in the cycle would likely result in both a retracing of cap rates and declines in asset values. Some declines in value would be offset by income returns, but only for those property types which we view as most resilient from a both cyclical and structural perspective.

The impact of the moderate recession, which is now our baseline scenario, will also vary by geography. As we have already stated, we feel that the impact of a global slowdown in growth is likely to impact Europe disproportionately due to its exposure to Russian commodities. As a result, private equity property values could face a correction of between 10% to 15% in the next 12 to 18 months in Europe. In the U.S. while energy prices are less threatening, the surge in interest rates is a much bigger problem than Europe. Thus, in the base case of a moderate recession, we will not be surprised to see the NCREIF NPI index witness capital depreciation in the neighborhood of 5% to 15%, over a similar timeframe of 12 to 18 months. Sector specific impacts will also vary widely depending on each property type’s sensitivity to cyclical shifts as well as underlying demand and capital market positioning.

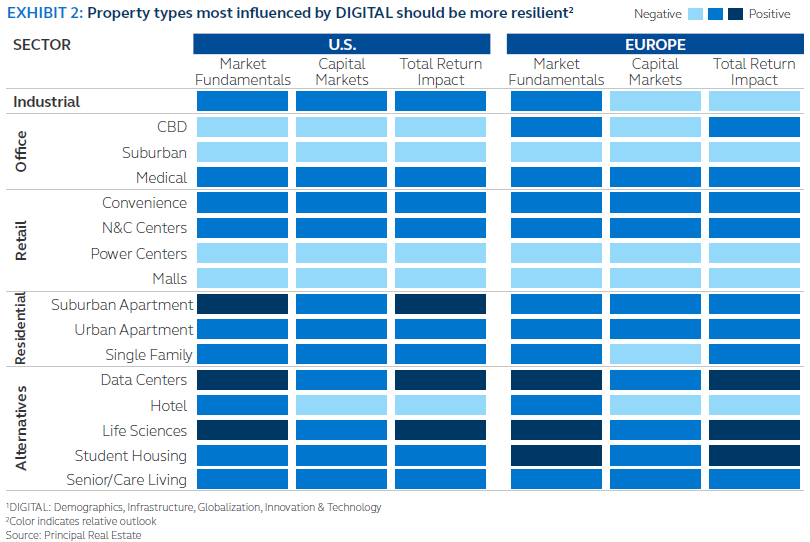

We believe that property types that adhere to our DIGITAL1 drivers are better positioned at least on a relative basis. Exhibit 2 below outlines the magnitude of both the fundamental and capital market impact of a moderate recession on each sector. The residential sector in both the U.S. and Europe is likely the most resilient, especially given its non-discretionary nature. In the U.S. there is an acute shortage of housing across much of the income spectrum, particularly single-family units to middle- and lower-income housing, because of the lack of development for much of the decade following the global financial crisis. Though the problem is less acute in most European markets, supply remains tight and should help mitigate both demand fallout and NOI declines that would drive values lower.

Shorter residential lease terms will allow for tenants to regain a modicum of pricing power should the recession prove more persistent than our current base case imagines. Though industrial has continued to outperform all other sectors, the nature of the downturn and a turnover in e-commerce spending relative to brick and mortar sales (in the U.S. in particular), have highlighted its vulnerability. Amazon, which had been a catalyst for outsized net absorption of space since 2019, has also announced it will be releasing space to the sublet market, indicating that it had overestimated its space needs.

Though it is unlikely to signal a broader drawdown given the demand for space along supply-chains, it could signal a level-shift in demand, which would be exacerbated by recession. A retracing of consumer spending would of course create problems for warehouse landlords and impact overall sector performance in both the U.S. and Europe—particularly as it relates to e-commerce. Our base case for recession, however, is far from the experience following

the housing collapse in 2008, which saw consumer demand decline so far that the U.S. experienced a brief period

of deflation for the first time since the 1950s. Record low vacancy rates in both regions will also provide support to industrial landlords, although weakness in core values will not be unexpected if tenant demand softens.

Among the remaining primary core real estate sectors, we feel there will be more room for adjustment, particularly in weaker subsectors. The secular decline in office demand in the U.S. has been well documented over the past 24 months. And, while occupancy and utilization trends in European office markets have outperformed their U.S. peers, a drawdown in services employment would likely create a darker scenario for landlords and investors in which vacancy rates linger higher than their equilibrium levels. We would expect some outperformance within the sector, however, from the traditional offices in core locations and, with ESG designations, medical and the life sciences sectors, which to date have outperformed. These sectors will remain in demand from a structural perspective and likely continue to outperform the broader office property indices over the next 12 to 24 months.

Retailers would also fall in the unfavored category, though it remains a highly bifurcated sector and investment performance will vary significantly. Brick and mortar sales growth has been impressive since 2021—partially fueled by fiscal stimulus and pent-up consumer demand—and store openings have outpaced closings over the past 18 months. The retail recovery has largely focused on convenience-based retail formats such as grocers, value-oriented retailers in community centers, as well as retail warehouses.

Over the next 12 months, these sectors should hold up well on a relative basis though rising cap rates should imply at least moderate value declines. The most impacted sector under our new base case will be larger mall and shopping center formats and those with a focus on discretionary spending and higher price points such as regional and super regional malls in the U.S., and High Street retailers (particularly focused on CBD locations) in both Europe and the U.S. The dislocation in the cyclical property types will challenge landlords and open up the pathway to price discovery, thereby also creating investment opportunities that have been hitherto absent from the transaction market.

Among the alternative sectors not already addressed, data centers should hold up both on an absolute and relative basis. Supply and demand fundamentals remain in balance and despite capital market disruptions strong rent and NOI growth will provide a bond-like coupon for investors.

It is imaginable that demand for data centers continues to improve through the recession due to both structural and cyclical drivers. Cost cutting among major corporates for example could shift demand further from pricey CBD offices toward work from home arrangements, which could potentially increase demand for data services.

Investment strategy implications

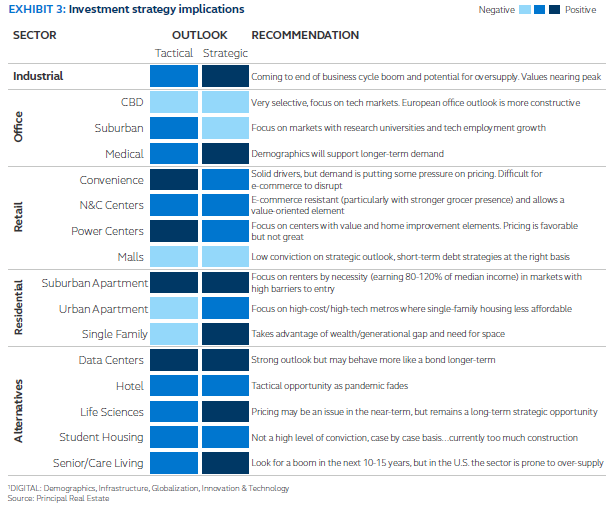

In this challenging environment where should investors look to preserve capital and seek relative value? At a base level, we expect cost of capital to increase and financial conditions to tighten. For real estate, we would expect capitalization rates to push up more as investors seek higher risk premia in an environment of slow growth/recession. As such, we prefer debt over core equity given the potential write down in equity values and the possible preservation to cash flows provided by subordination.

From a sector selection perspective, we are biased towards segments that are non-discretionary—food (grocery anchored centers, discounters, retail warehouses), shelter, and structurally driven property types (data centers, medical offices, senior/care living). For markets, we continue to tilt towards our DIGITAL1 markets which have key structural elements that should weather a recession, though asset selection is going to become even more paramount. In the past 12 months, transaction activity has been mostly focused around the most favored property types (mostly structurally resilient). We expect the transaction market to broaden out as debt markets become less forgiving and force more assets towards price discovery. We are therefore also going to be on the look out for interesting dislocation opportunities once price discovery becomes more widespread, particularly within the more cyclical property types.

Important Information

This material covers general information only and does not take account of any investor’s investment objectives or financial situation and should not be Investing involves risk, including possible loss of principal. Past performance is no guarantee of future results.

Potential investors should be aware of the risks inherent to owning and investing in real estate, including value fluctuations, capital market pricing volatility, liquidity risks, leverage, credit risk, occupancy risk and legal risk. All these risks can lead to a decline in the value of the real estate, a decline in the income produced by the real estate and declines in the value or total loss in value of securities derived from investments in real estate. International and global investing involves greater risks such as currency fluctuations, political/social instability, and differing accounting standards. Direct investments in real estate are highly illiquid and subject to industry or economic cycles resulting in downturns in demand. Accordingly, there can be no assurance that investments in real estate will be able to be sold in a timely manner and/or on favorable terms.

This material covers general information only and does not take account of any investor’s investment objectives or financial situation and should not be construed as specific investment advice, a recommendation, or be relied on in any way as a guarantee, promise, forecast or prediction of future events regarding an investment or the markets in general. The opinions and predictions expressed are subject to change without prior notice. The information presented has been derived from sources believed to be accurate; however, we do not independently verify or guarantee its accuracy or validity. Any reference to a specific investment or security does not constitute a recommendation to buy, sell, or hold such investment or security, nor an indication that the investment manager or its affiliates has recommended a specific security for any client account. Subject to any contrary provisions of applicable law, the investment manager and its affiliates, and their officers, directors, employees, agents, disclaim any express or implied warranty of reliability or accuracy and any responsibility arising in any way (including by reason of negligence) for errors or omissions in the information or data provided.

This material may contain ‘forward looking’ information that is not purely historical in nature. Such information may include, among other things, projections, and forecasts. There is no guarantee that any forecasts made will come to pass. Reliance upon information in this material is at the sole discretion of the reader.

Indices are unmanaged and do not take into account fees, expenses, and transaction costs and it is not possible to invest in an index.

This material is not intended for distribution to or use by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation.

This document is intended for use in:

• The United States by Principal Global Investors, LLC, which is regulated by the U.S. Securities and Exchange Commission.

• Europe by Principal Global Investors (EU) Limited, Sobo Works, Windmill Lane, Dublin D02 K156, Ireland. Principal Global Investors (EU) Limited

is regulated by the Central Bank of Ireland. In Europe, this document is directed exclusively at Professional Clients and Eligible Counterparties and should not be relied upon by Retail Clients (all as defined by the MiFID). The contents of the document have been approved by the relevant entity. Clients that do not directly contract with Principal Global Investors (Europe) Limited (“PGIE”) or Principal Global Investors (EU) Limited (“PGI EU”) will not benefit from the protections offered by the rules and regulations of the Financial Conduct Authority or the Central Bank of Ireland, including those enacted under MiFID II. Further, where clients do contract with PGIE or PGI EU, PGIE or PGI EU may delegate management authority to affiliates that are not authorized and regulated within Europe and in any such case, the client may not benefit from all protections offered by the rules and regulations of the Financial Conduct Authority, or the Central Bank of Ireland.

• United Kingdom by Principal Global Investors (Europe) Limited, Level 1, 1 Wood Street, London, EC2V 7 JB, registered in England, No. 03819986, which is authorised and regulated by the Financial Conduct Authority (“FCA”).

• This document is marketing material and is issued in Switzerland by Principal Global Investors (Switzerland) GmbH.

• United Arab Emirates by Principal Global Investors LLC, a branch registered in the Dubai International Financial Centre and authorized by the Dubai Financial Services Authority as a representative office and is delivered on an individual basis to the recipient and should not be passed on or otherwise distributed by the recipient to any other person or organisation.

• Singapore by Principal Global Investors (Singapore)Limited (ACRA Reg.No.199603735H), which is regulated by the Monetary Authority of Singapore and is directed exclusively at institutional investors as defined by the Securities and Futures Act 2001. This advertisement or publication has not been reviewed by the Monetary Authority of Singapore.

• Australia by Principal Global Investors (Australia) Limited (ABN 45 102 488 068, AFS Licence No. 225385), which is regulated by the Australian Securities and Investments Commission. This document is intended for sophisticated institutional investors only.

• Hong Kong SAR (China) by Principal Global Investors (Hong Kong) Limited, which is regulated by the Securities and Futures Commission and is directed exclusively at professional investors as defined by the Securities and Futures Ordinance.

• Other APAC Countries, this material is issued for institutional investors only (or professional/sophisticated/qualified investors, as such term may apply in local jurisdictions) and is delivered on an individual basis to the recipient and should not be passed on, used by any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation

© 2022 Principal Financial Services, Inc. Principal®, Principal Financial Group®, and Principal and the logomark design are registered trademarks of Principal Financial Services, Inc., a Principal Financial Group company, in the United States and are trademarks and services marks of Principal Financial Services, Inc., in various countries around the world. Principal Global Investors leads global asset management at Principal®. Principal Real Estate Investors is a dedicated real estate investment management group within Principal Global Investors.

MM13005 | 08/2022 | 2303516-122023

Weekly Investment Commentary: Earnings season: investment ideas

First-quarter earnings season has kicked off with the utilities and communication services sectors projected to deliver the strongest year-over-year EPS growth, while estimates for materials and energy are expected to decline the most.

Global Weekly Commentary: Earnings growth not just about tech

Solid U.S. economic and corporate earnings growth have supported risk appetite, driving stocks to all-time highs – even as bond yields have jumped. We think earnings will need to deliver on high expectations, especially after last week’s data showing sticky inflation spooked investors.

Global Markets Weekly Update: April 12, 2024

Review the performance of global stock and bond markets over the past week, along with relevant insights from T. Rowe Price economists and investment professionals.