China's Digital Currency is a Threat to Dollar Dominance

Beijing’s ambitions could spur acceptance of renminbi as the main rival to the US currency, according to Dr. Michael Hasenstab, CIO of Templeton Global Macro. This commentary was first published in the Financial Times’ Opinion Markets Insights column on April 13, 2021.

Markets have been gripped by cryptocurrency fever. The price of bitcoin has attained new record highs while debate has raged over the emergence of cryptocurrency technology.

But these may be a sideshow for a big emerging trend—the rapid digitalisation of the renminbi.

This shift, combined with other macroeconomic and political factors, could be the key that accelerates the decline of the dollar’s dominance as the world’s leading reserve currency. It could also hasten the acceptance of the renminbi as the main rival to the US currency.

Central banks around the world have been grappling in recent years with the concept of digital currency technology. Few nations, though, are as aggressive as China in their approach to developing a so-called central bank digital currency (CBDC).

Such a currency would be overseen by a central governmental authority, removing the element of anonymity that is fundamental to the decentralised, blockchain-ledger of popularised cryptocurrencies like bitcoin or ethereum. The theoretical benefits of government oversight of these new digital assets are numerous.

CBDCs allow for greater fraud or crime prevention, enable instantaneous international transactions, reduce transaction costs, permit greater financial inclusion and aid the provision of direct fiscal stimulus to individual citizens.

For China, adoption of a CBDC both within and beyond its borders would allow its financial system to reduce reliance on the dollar and limit the role and oversight of foreign financial institutions and regulators. While many countries have started discussing the potential future application of CBDCs, China has pushed ahead with development.

In April 2020, Beijing piloted a digital currency in four cities, allowing commercial banks to run internal tests converting between cash and digital money, account-balance checks, and payments. The pilot programme expanded to 28 major cities in August. Aiming for broad circulation in 2022, China plans to test the digital currency in additional major cities, including Beijing and Shanghai, this year.

This pioneering approach should accelerate the elevation of the renminbi on the world stage. Some users outside China, particularly in the US, might be reluctant to use a digital currency controlled by China. However, early adoption in parts of Asia, Latin America and Africa is likely to proceed significantly faster.

Global reserve currencies’ relative importance historically is explained by the macroeconomist Barry Eichengreen. Currencies are more prized as reserve assets when they satisfy two conditions: first, when they are stable, liquid and widely used in international transactions; and second, when they are backed by a country to which another state has important security links.

China’s development in recent years puts it on a clear path to satisfy these criteria as its government has maintained relative policy stability. The country accounted for 16% of global output in 2019, but the renminbi represented a little over 2% of global reserves as of the second-quarter last year.

Lack of renminbi-denominated assets for foreigners to own has inhibited the rise of the renminbi as a reserve currency. But now the renminbi will be supported by the Chinese authorities opening their US$15 trillion domestic bond market to foreign participants. Greater demand for these bonds will push down yields, lowering borrowing costs.

More important, if China captures the first-mover advantage to meet the world’s demand for use of digital currencies to settle international financial transactions and own digital assets, the appeal of its CBDC could rise sharply.

China has also made great strides in invoicing its trade in renminbi. The security and geopolitical rationale for holding renminbi has become stronger through such measures as China’s Belt and Road Initiative financing of projects in developing countries.

COVID-19 might also be a catalyst for the greater acceptance of the renminbi as a global reserve currency. The economic carnage of the pandemic has sent already large fiscal deficits ballooning and driven even more accommodative monetary policy in the US.

This historically unique combination of impending massive fiscal and vaccine-led growth, where short-term interest rates are anchored at zero, will expand an already large current account deficit, putting further pressure on the value of the dollar.

The digitalisation of the renminbi will add to these economic and geopolitical factors. This will have a durable, transformative impact on the international economy.

What Are the Risks?

All investments involve risks, including possible loss of principal. The value of investments can go down as well as up, and investors may not get back the full amount invested. Special risks are associated with foreign investing, including currency fluctuations, economic instability and political developments. Investments in emerging markets involve heightened risks related to the same factors, in addition to those associated with these markets’ smaller size, lesser liquidity and lack of established legal, political, business and social frameworks to support securities markets. Bond prices generally move in the opposite direction of interest rates. Thus, as prices of bonds in an investment portfolio adjust to a rise in interest rates, the value of the portfolio may decline. To the extent a strategy focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a strategy that invests in a wider variety of countries, regions, industries, sectors or investments. China may be subject to considerable degrees of economic, political and social instability. Investments in securities of Chinese issuers involve risks that are specific to China, including certain legal, regulatory, political and economic risks.

Buying and using blockchain-enabled digital currency carries risks, including the loss of principal. Speculative trading in bitcoins and other forms of cryptocurrencies, many of which have exhibited extreme price volatility, carries significant risk. Among other risks, interactions with companies claiming to offer cryptocurrency payment platforms or other cryptocurrency-related products and services may expose users to fraud. Blockchain technology is a new and relatively untested technology and may never be implemented to a scale that provides identifiable benefits. Investing in cryptocurrencies and ICOs is highly speculative and an investor can lose the entire amount of their investment. If a cryptocurrency is deemed a security, it may be deemed to violate federal securities laws. There may be a limited or no secondary market for cryptocurrencies.

IMPORTANT LEGAL INFORMATION

This material is intended to be of general interest only and should not be construed as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy. It does not constitute legal or tax advice.

The views expressed are those of the investment manager and the comments, opinions and analyses are rendered as at publication date and may change without notice. The information provided in this material is not intended as a complete analysis of every material fact regarding any country, region or market. All investments involve risks, including possible loss of principal.

Data from third party sources may have been used in the preparation of this material and Franklin Templeton ("FT") has not independently verified, validated or audited such data. FT accepts no liability whatsoever for any loss arising from use of this information and reliance upon the comments opinions and analyses in the material is at the sole discretion of the user.

Products, services and information may not be available in all jurisdictions and are offered outside the U.S. by other FT affiliates and/or their distributors as local laws and regulation permits. Please consult your own financial professional or Franklin Templeton institutional contact for further information on availability of products and services in your jurisdiction.

Issued in the U.S. by Franklin Templeton Distributors, Inc., One Franklin Parkway, San Mateo, California 94403-1906, (800) DIAL BEN/342-5236, franklintempleton.com - Franklin Templeton Distributors, Inc. is the principal distributor of Franklin Templeton U.S. registered products, which are not FDIC insured; may lose value; and are not bank guaranteed and are available only in jurisdictions where an offer or solicitation of such products is permitted under applicable laws and regulation.

You need Adobe Acrobat Reader to view and print PDF documents. Download a free version from Adobe's website.

Franklin Templeton Distributors, Inc.

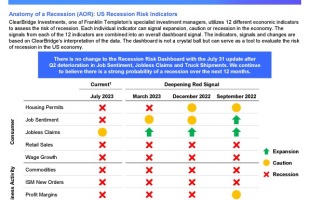

Anatomy of a Recession Update: Cracks in the Foundation

Get perspective on the most recent US economic data, the investor’s view, and how reviewing previous recessionary periods may help us today, in this conversation with Jeff Schulze, Head of Economic and Market Research at ClearBridge Investments.

AOR Update: When to expect a recession?

ClearBridge Investments: Despite improving economic sentiment now leaning the consensus view toward a soft landing, we continue to believe a recession is on the horizon.

Anatomy of a Recession: Economic and Market Outlook 3Q 2023 | August 1st

ClearBridge Investments, one of Franklin Templeton’s specialist investment managers, utilizes 12 different economic indicators to assess the risk of recession.